2022 is a year that will go down in history. Every month, the Consumer Price Index (CPI) increases tremendously, with the latest June report increasing 9.1% over the past year. On top of that, the Federal Reserve has delivered the biggest rate increase since 1994, a 0.75 basis point increase, to tackle the ever hotter U.S. inflation.

In times like this, companies in the consumer staples industry usually thrive. This is because companies in the consumer staples industry are seen as recession-resistant. Moreover, payment technology companies, such as Visa and Mastercard, are businesses that are highly reliant on consumer spending activities.

Recent market corrections have somewhat deflated the bubbles in many growth stocks, bringing their valuations to much more reasonable levels. PayPal Holdings and Visa are two representatives. Paypal has declined over 70%, while Visa has declined to a lesser degree, by about 20% off its peak.

Thus, we would like to discover and unpack more about Visa on whether this could be a good opportunity to buy this stock. So, let’s take a closer look at Visa’s main business and financials in order to better assess Visa’s overall performance.

An Overview of Visa’s Business

Visa was introduced by Bank of America (BofA) as the BankAmericard credit card program in September 1958. In 1966, in response to competitor Master Charge (now ), Bank of America began licensing the BankAmericard service to other banking institutions. By 1970, BofA relinquished direct control of the BankAmericard program, creating a partnership with other BankAmericard issuer banks to oversee it. In 1976, it was renamed Visa.

Based on the yearly amount of card payments processed and the number of issued cards, Visa is the world’s second-largest card payment organization (debit and credit cards combined), having been eclipsed by China UnionPay in 2015. As UnionPay’s size is essentially determined by the size of its native market in China, Visa remains the largest bankcard firm in the rest of the globe, where it controls a 50% market share of total card payments.

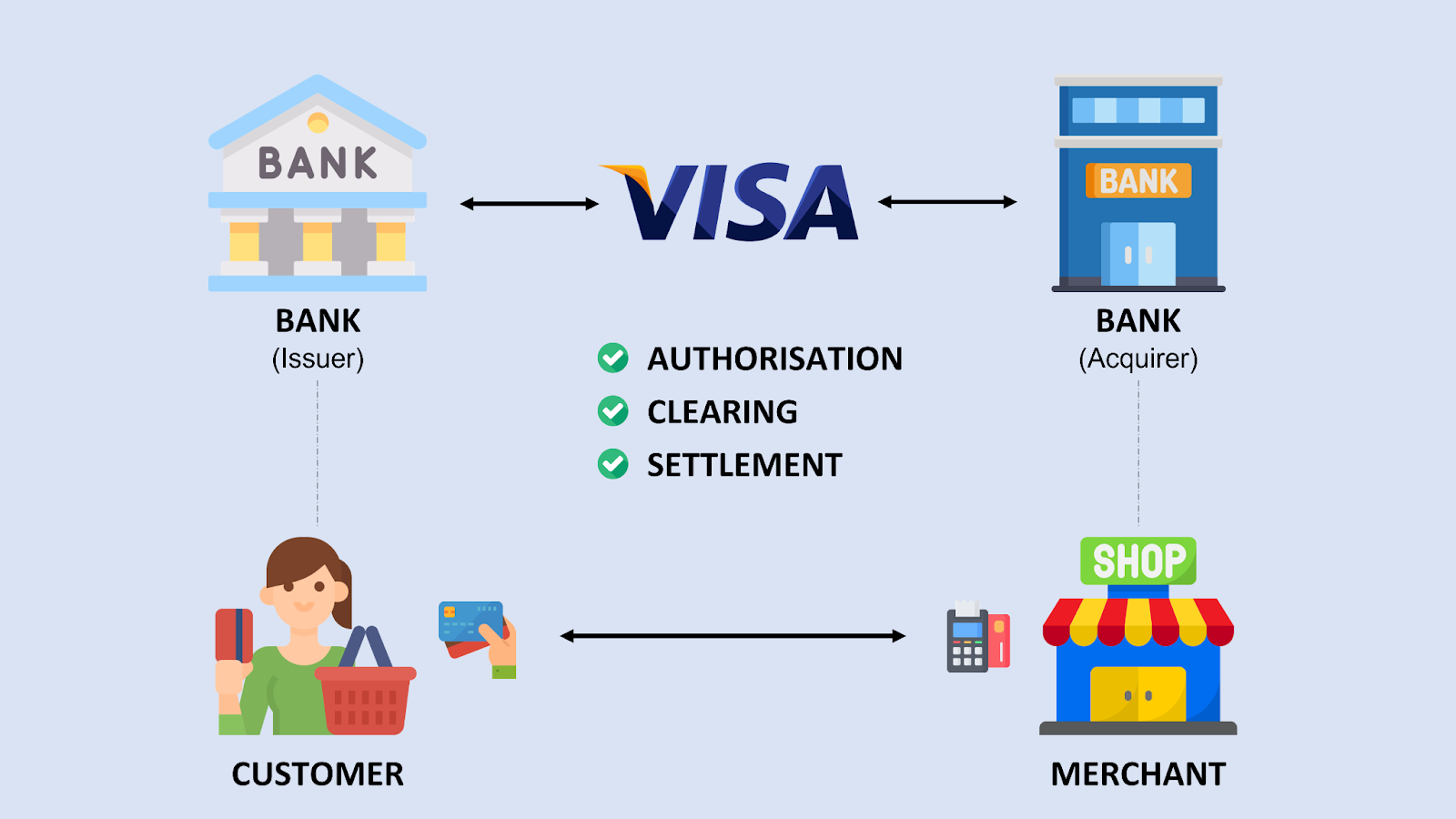

How does Visa work?

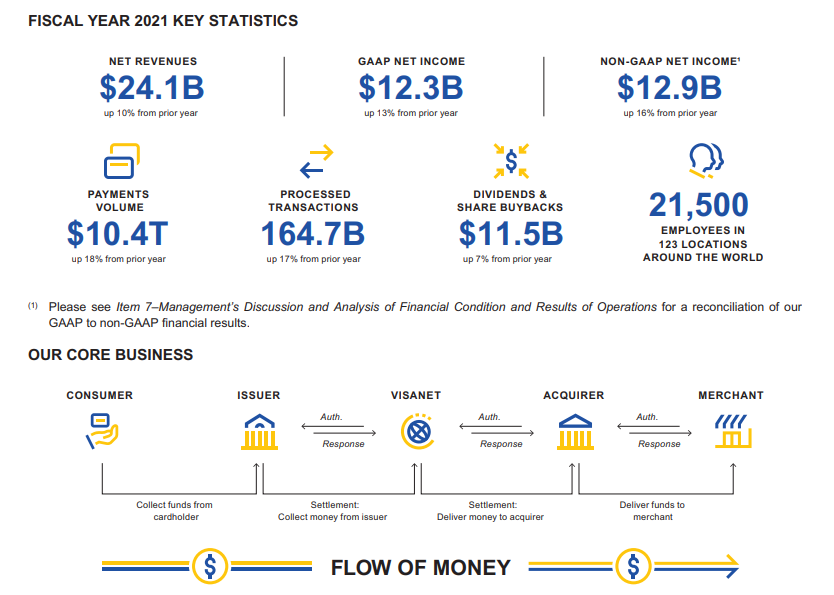

In a typical Visa transaction, it involves 4 different parties: Cardholders, Issuing bank (Cardholder Bank) , Merchant and Acquirer (Merchant Bank). Visa acts as the toll operator and is responsible for authorization, clearing, and settlement of payments across all parties. As a result, Visa is paid transaction and volume fees by the respective banks for facilitating all these payments.

In summary, Visa typically charges 1.15% + $0.05 to 2.40% + $0.10 for each transaction. These charges include assessment, processing, authentication, and connectivity fees. This may seem puny, but when one considers that Visa processed over 10.4 trillion transactions in 2021, it adds up.

Qualitative Factors affecting Visa

Let’s look at the qualitative aspects in order to get a more accurate assessment of Visa’s price and value.

Economic Moat

1. Economics of scale

Economies of scale arise when a company’s marginal costs decrease as the volume of its activities grows. Visa does benefit from economies of scale since it operates a large network to handle data and transactions. The expense of adding new clients to this network is small in comparison to the company’s earnings.

Visa has attained a gross profit margin of about 97% during the previous ten years. This is because, like other SaaS firms, it has few costs that are directly related to its sales. Visa is likely the most obvious example of scale economies. This is both a plus for Visa since it can attain greater overall margins and a disadvantage for rivals because they will not benefit from this improved profitability till they reach a specific size.

2. Brand Equity

Visa, once again, is in a really unusual branding circumstance since it is a truly worldwide and intersectional brand. Visa markets to whom? Everyone in the world is the answer.

Visa has effectively established a household name, and its brand is synonymous with convenience and dependability. Trusting your money to a corporation is a tough thing to do, which is why firms like Visa and Mastercard have maintained such a firm grip on the market. Visa is an appealing payment option since it is used by practically everyone, implying that it must be reliable.

Furthermore, according to Kantar research, Visa is one of the world’s most well-known brands. Visa was ranked 7th among the top ten most valuable brands in 2022.

Growth Opportunities

1. Secular growth tailwinds in the e-commerce (digital payments)

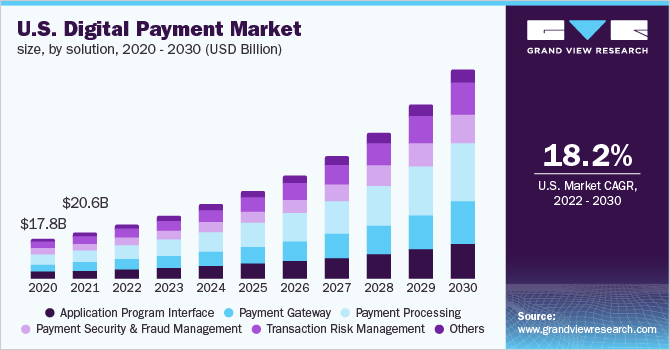

Visa looks well-positioned to benefit from the secular growth trend of payments gradually moving to digital channels. Whether we like it or not, COVID has accelerated the pace of adoption of emerging technologies. In fact, digital payment methods are one of the many ways that have benefited.

The global digital payment market was valued at USD 68.61 billion in 2021 and is expected to expand at a compound annual growth rate (CAGR) of 20.5% from 2022 to 2030. The worldwide increase in customer preference for real-time payments is one of the major factors driving the market’s growth.

Thus, Visa is poised to capitalize on the megatrend of the eCommerce explosion. Ecommerce boomed in 2020 as home-bound consumers sought shopping alternatives and drove the fastest growth rate in five years.

2. Change in consumer behavior (away from cash)

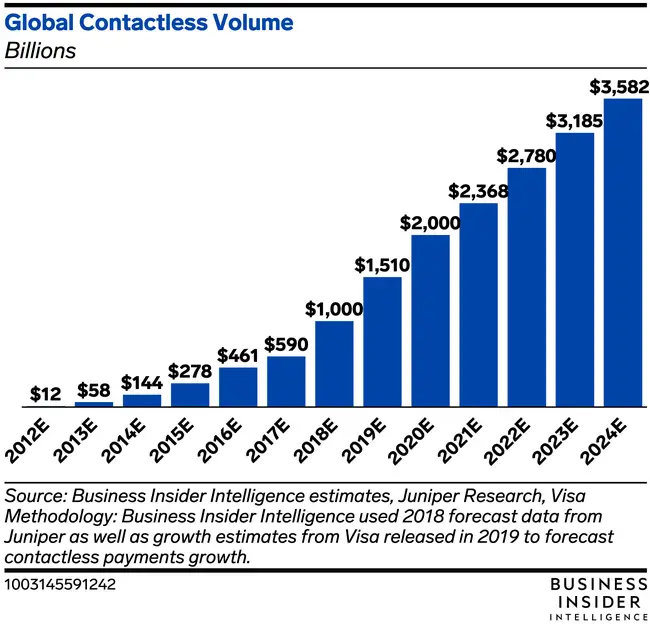

Customers that are younger and more tech-savvy are interested in digital wallet payments. According to a Business Insider article, the expected global contactless volume is growing at an exponential rate. Less conventional alternatives, such as person-to-person transactions and Buy Now, Pay Later payment arrangements, have seen great recent development. Visa is ideally positioned to capitalize on these changes since it provides a payment network with size, security, and reputation.

Visa has worked with a number of companies to provide Apple Pay, Google Pay, and Samsung Pay, as millennials become increasingly interested in mobile and digital wallet payments. Contactless and tap-to-pay have reached 20% penetration in the United States. These services will eventually aid in the acceleration of cash digitization. As a result, merchants are not required to invest in large infrastructure, making these solutions appealing and cost-effective for smaller merchants or merchants in emerging regions.

Business Risks

1. Recession and Exit from Russia

The possibility of a future recession is always present. While Visa will continue to gain from the consumer staples business, transactions and payment volume for discretionary products are expected to fall, resulting in decreased income.

Visa ceased operations in Russia in March. This will almost certainly be detrimental in the long term since it will result in fewer total transactions and payment volume. This will immediately result in less revenue for the firm and poorer fundamentals.

Hence, these 2 possibilities, if they were to happen in the future, would definitely have an impact on Visa.

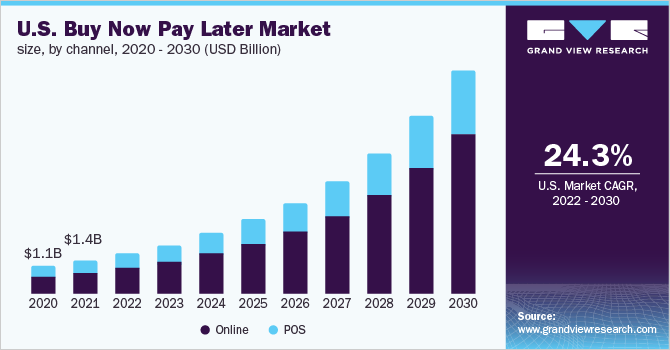

2. Emerging Technologies – Digital Payments, BNPL etc

The physical payment market is dominated by a duopoly of Visa and Mastercard. While Visa and Mastercard continue to dominate the physical payment business, retailers cannot escape utilizing their network, even as competition in in-store payments grows. There are more options for online payments, and the recent emergence of buy now, pay later (BNPL) possibilities is another threat to Visa’s stronghold in the digital payments market.

This occurs because BNPL is sometimes less expensive than charging large purchases to a credit card. Most credit card companies and banks charge very high interest rates that can reach 20% or more, but most BNPL solutions do not charge any interest as long as clients follow the payment schedule. Payments are normally made in three or four installments over a short period of time, usually no more than 3-6 months.

As more people avoid using credit cards for online purchasing, Visa’s position in the payment choices may deteriorate. This might be one of the reasons Amazon has threatened to discontinue Visa cards in the United Kingdom.

Quantitative Factors affecting Visa

Let’s look at the quantitative aspects in order to get a more accurate assessment of Visa’s price and value.

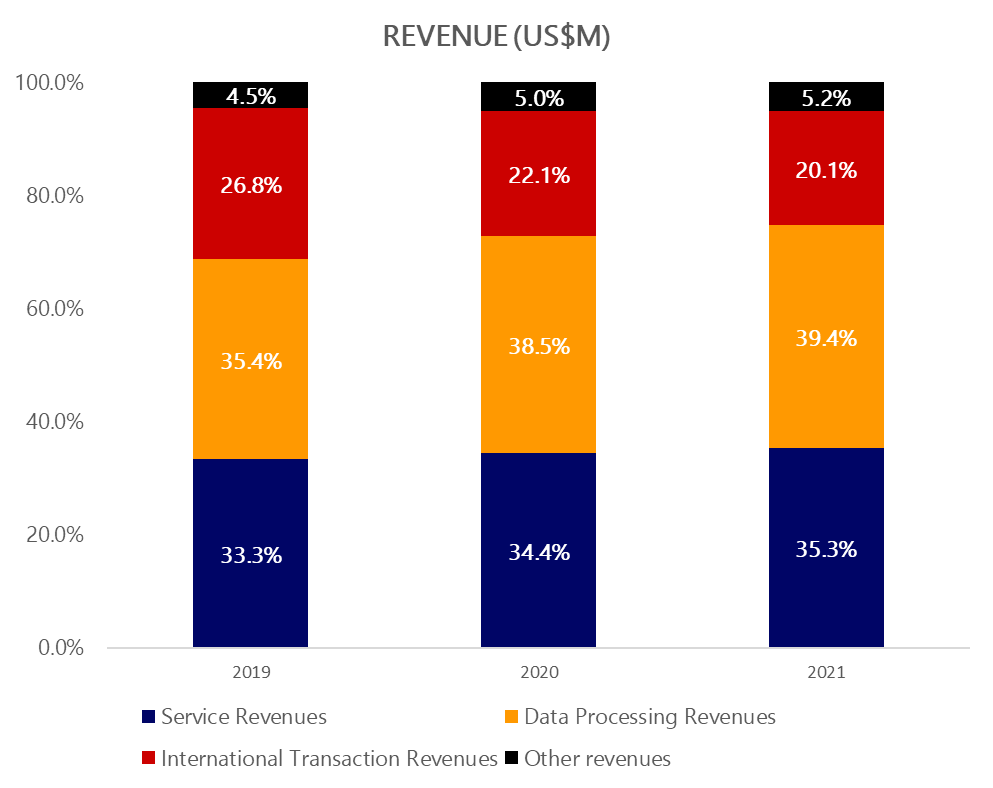

1. Financial Highlights (Revenue Breakdown)

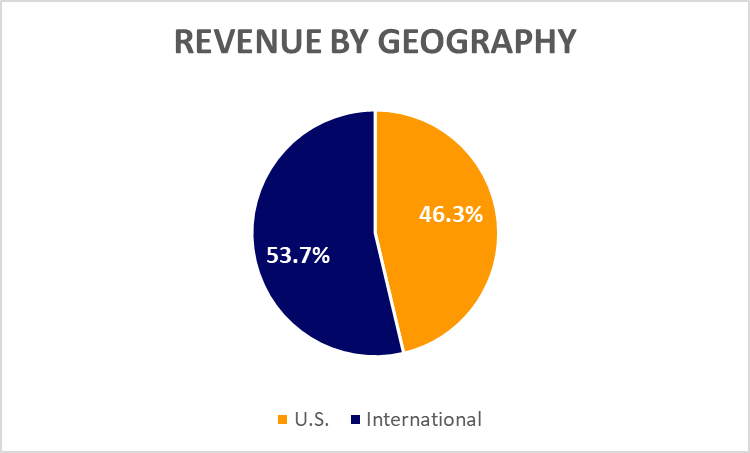

The majority of Visa’s revenue in 2021 is contributed by Data Processing Revenues. The other segments, like Service Revenues and International Transaction Revenues, are also big contributors to their annual revenue. Currently, 46% of their revenue is derived from the United States and the remaining 54% is from international markets.

2. Key Valuation Ratios

When evaluating the financial state of a growing firm like Visa, we must assess key financial ratios such as Revenue Growth, P/S, P/E, Gross Margin%, Operating Margin%, and FCF.

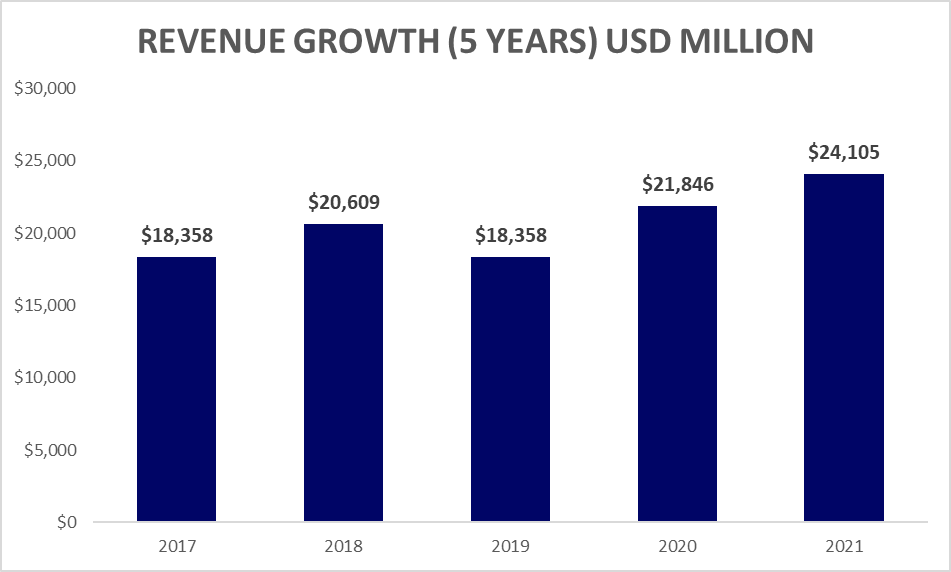

Revenue Growth (5 Years)

Visa’s 2021 revenue stands at $24.1B with 10.0% (YoY growth) and its 5-Year CAGR stands at 5.6%.

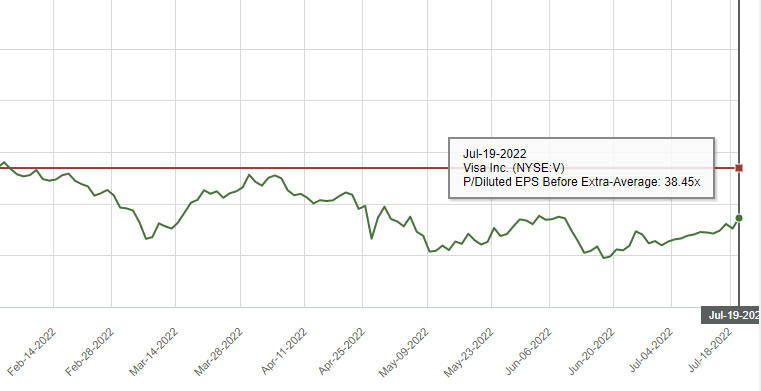

Price/Equity (P/E) ratio (1 Year)

The current Visa P/E stands at 33.61x, while it’s 1-year Avg P/E ratio stands at 38.45x

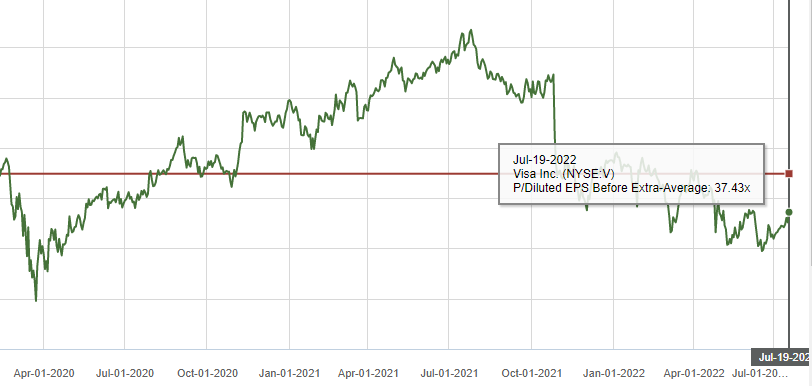

Price/Equity (P/E) ratio (5 Year)

The current Visa P/E stands at 33.61x while it’s 5-year Avg P/E ratio stands at 37.43x

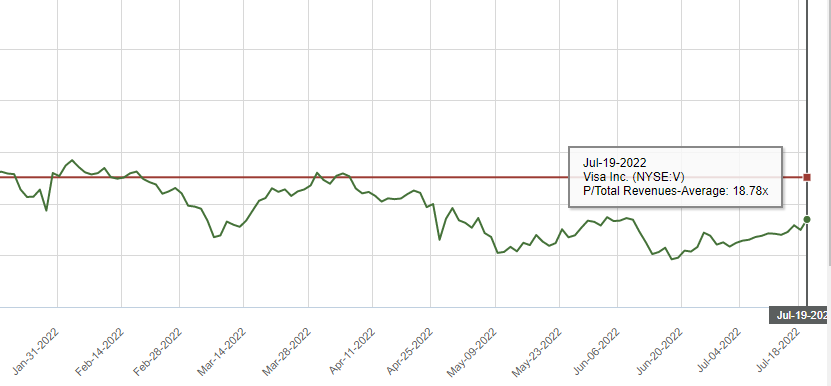

Price/Sales (P/S) ratio (1 Year)

The current Visa P/S stands at 16.74x while it’s 1-year Avg P/S ratio stands at 18.78x

Price/Sales (P/S) ratio (5 Year)

The current Visa P/S stands at 16.74x while it’s 5-year Avg P/S ratio stands at 17.48x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs. On the other hand, operating profit margin also considers running expenses such as overhead. Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Visa’s financials, its EBITDA margin has been lingering around 69+%. Its operating margin has been sitting around ~60% while its FCF margin is around ~55%. An operating margin of more than 15% is regarded as good in most businesses as a rule of thumb. As a result, this clearly demonstrates that Visa has been doing alright financially.

| Other Key Ratios | 2017 | 2018 | 2019 | 2020 | 2021 | LTM |

| EBITDA Margin % | 68.8% | 68.8% | 69.9% | 68.0% | 68.9% | 70.4% |

| Operating Margin % | 50.8% | 62.8% | 55.6% | 47.8% | 63.2% | 59.8% |

| FCF% | 46.9% | 59.3% | 52.3% | 44.4% | 60.2% | 56.7% |

Our Stand

Visa has a robust worldwide network, but its growth is slowing and new entrants are flooding in. With disruptive innovators lurking in the shadows, it may be time to sit back and see how this sector develops. Visa appears to be a potential company to explore in terms of quality, safety, fortress balance sheet, and long-term risk management.

However, Mastercard is a far faster-growing corporation, which might result in exponential returns for Mastercard stockholders, who are anticipated to witness significantly higher growth over the next 10+ years. Although, Visa retains a significant moat due to its far bigger payment volume and ever-increasing number of transactions, Mastercard seems to be a better buy between the 2 payment processing giants.

Click here for our Mastercard Stock Analysis

If you are keen, check out our articles on other analysis: Digital Core REIT Analysis, What happened in the 1st half of 2022, and OCBC Stock Analysis. With all this in mind, Visa still seems a little expensive, but it may be a good opportunity to consider if you have not invested in it.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.