Over the past few months, Data Centre REITs in Singapore has all taken a beating in terms of stock prices. For example, Keppel DC REIT share prices has fallen by ~20% from a year ago. However, with strong demand for cloud and rising data business, the demand for Data centres are still expected to remain strong. Hence, companies Keppel DC REIT and Digital Core REIT are expected to benefit from it.

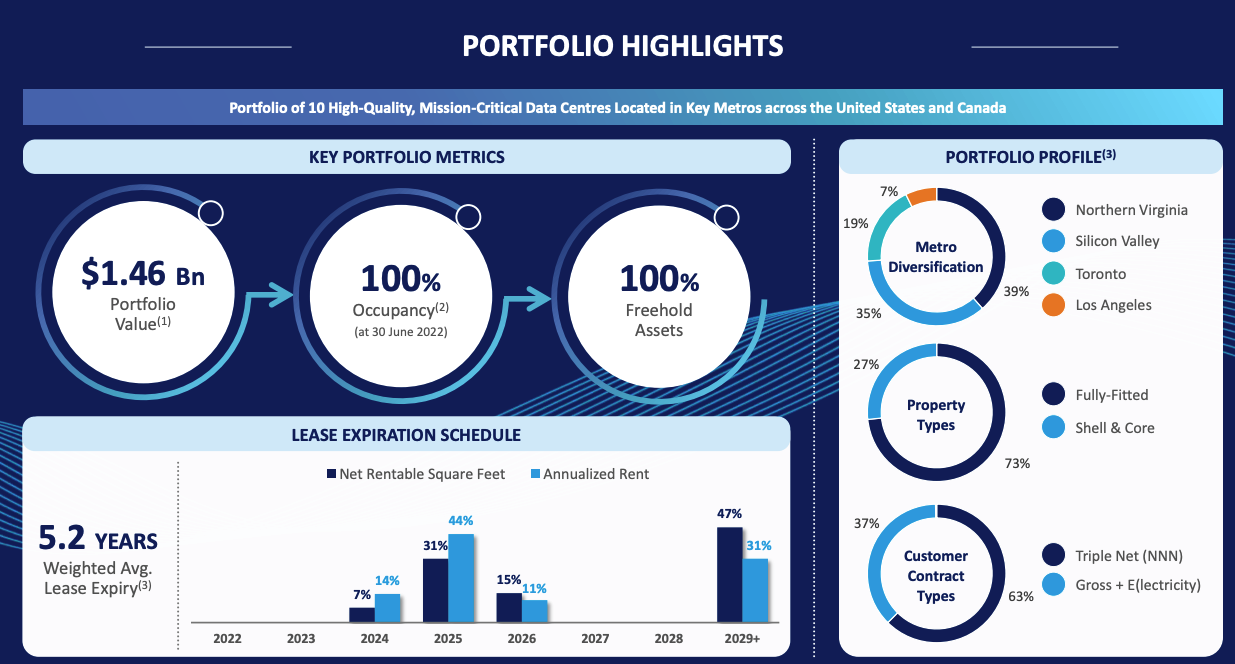

It is a pure-play data center REIT that was listed in Singapore in December 2021. It is currently sponsored by one of the best-in-class data operators, Digital Realty. The Data centers under its portfolio are primarily located in the United States and Canada. As at July 2022, Digital Core REIT’s total portfolio size stands at 10 properties totalling approximately S$1.46 billion.

Overview of Business

Key highlights for the current Portfolio:

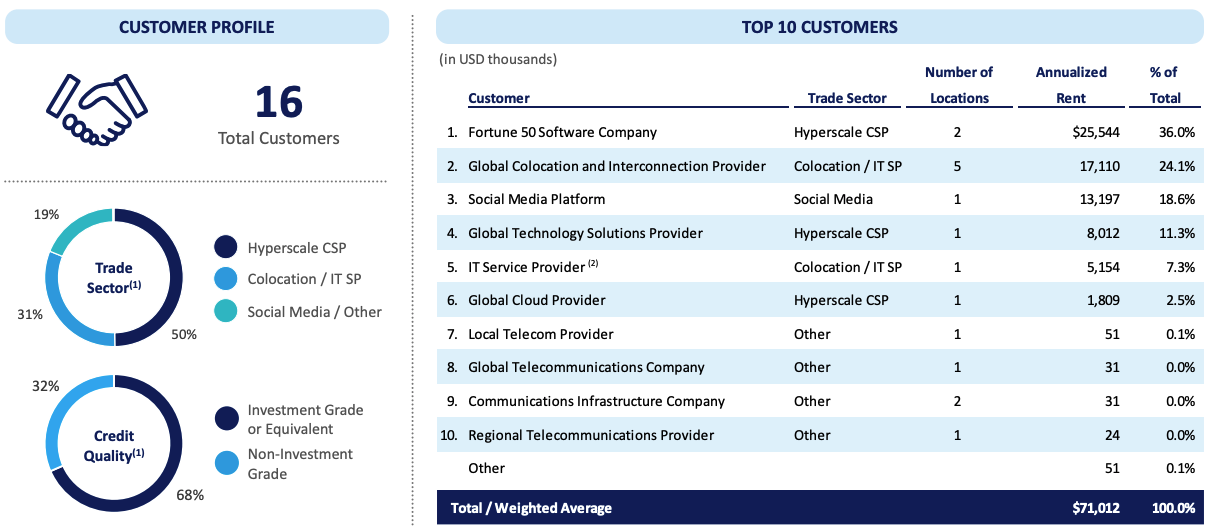

- 10 Properties and 16 tenants

- Geographic breakdown:

- 9 (USA) and 1 (Canada)

- Portfolio Size: S$1.46 billion

- 5.2 Weighted Years Average Lease To Expiry (by Gross Revenue)

Key Figures for Digital Core REIT

Currently there are no historical figures to compare with because the company just went public in 2021.

Digital Core REIT Portfolio has a total of 16 tenants with the Top 5 customers accounting 97% of annual portfolio gross revenue. Its portfolio weighted average lease expiry (WALE) stands at 5.2 years. The small tenant size is a customer concentration risk, and if one of the Top 5 tenants do leave, this may severely impact their revenue.

Growth Prospects for Digital Core REIT

Digital Core REIT’s growth goal is to grow its portfolio into key markets like Frankfurt, Chicago and Dallas.

Dividend Yield

Digital Core REIT shares now stand at US$0.87 per share. Based on its projected FY2022 DPU payout of 4.28 US cents, this would means a dividend yield of 4.91%

Our Stand

Digital Realty has been one of the best performing REITs since its inception in the early 2000s. However, for the REIT holdings, it only has about 10 properties under its belt. Hence,it will still take some time for the REIT to prove that it is capable of delivering results like its sponsor.

At current valuation, it seems a little overvalued with a current dividend yield of 4.91%. Before investing, I would prefer a bigger margin of safety and a yield of about ~7% yield.

If you are keen to read about our analysis on other stocks in Singapore, you can check out our latest article on OCBC and Ascendas REIT.