Payment companies like Mastercard are highly reliant on consumer spending and business activities. Concerns over rising interest rates raises the possibility of a recession or stagflation. In either case, consumer and business spending would be affected which may hamper Mastercard business. In 2022 alone, Mastercard has dropped by about ~10%.

The recent increase in interest rates by the Fed have definitely increased recession fears globally. In 2022, the S&P 500 and multiple companies’ valuation plummeted to year low. Growth and technology stocks have been one of the worst-hit sectors after the recent tightening policy. Consumer-staples companies are often viewed as recession resistant due to their necessity in all situations. Is the current market condition a concern or could this be a good opportunity for us to consider the stock?

So let’s take a closer look at its main business and financial outcomes in order to better assess Mastercard’s overall performance.

Overview of Mastercard’s Business

Mastercard, formerly Interbank and Master Charge in the 1960s, was created to compete with BankAmericard issued by Bank of America. They were formed by an alliance of regional bank associations and banks to aggregate their customer and merchant networks. Over the years, Mastercard also made several strategic acquisitions like Europay, DataCash and Provus. Today, Mastercard enables the use of debit, prepaid and credit cards in more than 150 currencies in over 210 countries globally. Mastercard processed over 112.1 billion transactions in 2021, with $7.7 trillion in gross volume processed.

How does Mastercard work?

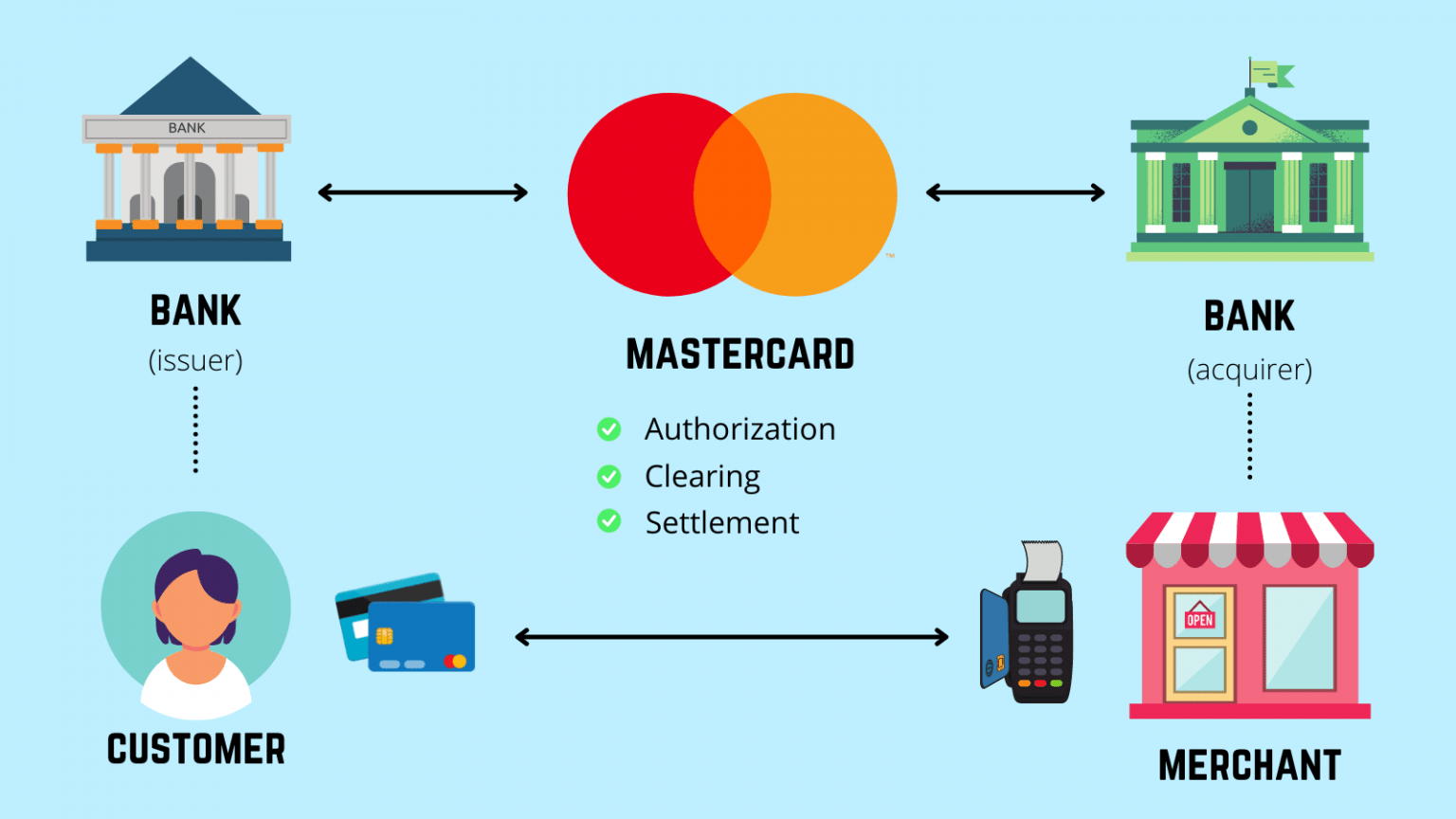

Alongside Visa, Mastercard is part of the duopoly that connects customers and business together to facilitate swift monetary transfer. They provide the infrastructure that allows banks and businesses to communicate with each other.

In a typical Mastercard transaction, it involves 4 different parties: Cardholders, Issuing bank (Cardholder Bank) , Merchant and Acquirer (Merchant Bank). Mastercard acts as the toll operator and is responsible for authorization, clearing and settlement of payments across all parties. As a result, Mastercard is paid transaction and volume fee for facilitating all these payments.

In summary, Mastercard typically charges from 1.35% to 3.25% for each transaction. These charges include assessment, processing, authentication and connectivity fees. This may seem puny but when one considers Mastercard processed over 100 billion transactions in 2021, it becomes substantial.

Qualitative Factors affecting Mastercard

Let’s look at the qualitative aspects in order to get a more accurate assessment of Mastercard’s price and value.

Economic Moat

1. Economics of Scale

Mastercard’s global network stands at 3 billion cardholders, 70 million merchants and over 20,000 institution partners. For Mastercard, the marginal cost of adding more cardholders or merchants is incredibly low as compared to potential disruptors. In addition, the payment processing industry requires strict compliance with regulations across the 210 countries that they operate in. Over multiple years of operation, Mastercard has amassed strong institutional and regulation expertise. This makes it challenging for new card brands to compete and little incentive for merchants to accept other brands.

2. Cutting-Edge Technology

Mastercard has a highly advanced payment network that connects millions of merchants to the different banks all around the world. The company ensures 99.999% availability and can process 432 million transactions per day at 5000 transactions per second. This is comparable to some of the top cryptocurrencies like Solana which processes an average 2700 transactions per second. Furthermore, Mastercard continues to invest in cutting-edge technologies like tokenisation and other features that improve processing speed and security. Its continual pursuit to improve its payment infrastructure will make it difficult for potential challengers to match quickly or cheaply.

Growth Opportunities

1. Multi-Rail strategy

Mastercard’s multi-rail strategy enables instantaneous global transfers between business-to-business (B2B) buyers and sellers for different payment forms. This allows users to choose from open banking, B2B, account-to-account (A2A), cryptocurrencies and more. Looking forward, Mastercard plans to leverage it with disbursements, remittance, POS and B2B transactions. The management sees this as an opportunity surpassing $14 trillion.

2. Services

One of Mastercard’s fastest growing segments is Services. This currently makes up over 35% of its net revenue. Services can be further split into the following: Cyber and Intelligence, Data and Services and others. Mastercard leverages the data collected to build stickiness with their customers. This aims to enhance transactions, deepen customer interaction, and improve customer decision-making. For example, Mastercard introduced a Test and Learn solution to identify and recommend solutions to attract customers. It has since generated over 67% return on investment and racked over 2200 clients. This allows Mastercard to position themselves as a front runner in the growing service innovation.

3. Micro, Small and Middle business opportunities

Duka Connect, is an app that was developed by Mastercard which turns a mobile phone into a point of sale (POS) tool. This tool is popular with micro businesses in developing countries due to its affordability. Furthermore, it offers advanced technologies like AI and computer vision to identify products without the use of scanning equipment. This completes the entire payment and transaction cycle of a customer. It is estimated that annually $19.8 trillion in payments are made across micro, small and middle retailers globally. However, more than 60% of these businesses are underserved for financial services and Mastercard sees an opportunity for it.

Business Risks

1. Risk Related to Company

One of the biggest risks for Mastercard would be an impending economic recession. In the event of a recession, payment volumes for consumers and business would decrease which would affect Mastercard’s revenue. However, the business is also defensive as the majority of the payments are generated from necessities or non-durable goods. This implies that Mastercard continues to generate consistent revenue during a recession.

2. Risk Related to Foreign Regulations

Mastercard operates internationally and thus their product and service offerings are subject to different regulations and oversights. Hence, the company has to be aware of any regulatory changes that may have an impact on the business.

Quantitative Factors affecting Mastercard

Let’s look at the quantitative aspects in order to get a more accurate assessment of Mastercard’s price and value.

1. Financial Highlights (Revenue Breakdown)

The majority of Mastercard’s revenue in 2021 is contributed from Transaction processing. The other segments like Cross-border and Domestic assessments are also big contributors to their annual revenue. Currently, 32% of their revenue is contributed from the United States and the remaining 68% is from International markets.

2. Key Valuation Ratios for Mastercard

When evaluating the financial state of a growing firm like Mastercard, it is crucial to assess key financial ratios.

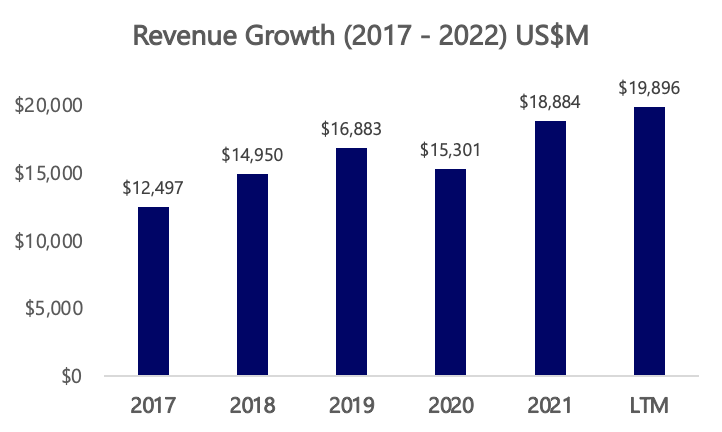

Revenue Growth (5 Year)

Mastercards LTM revenue stands at $19.9B with 23.4% (YoY growth) and 5-Year CAGR stands at 11.9%

Price/Sales (P/S) ratio (1 Year)

The current P/S Mastercard stands at 15.97x while it’s 1-year Avg P/S ratio stands at 19.46x

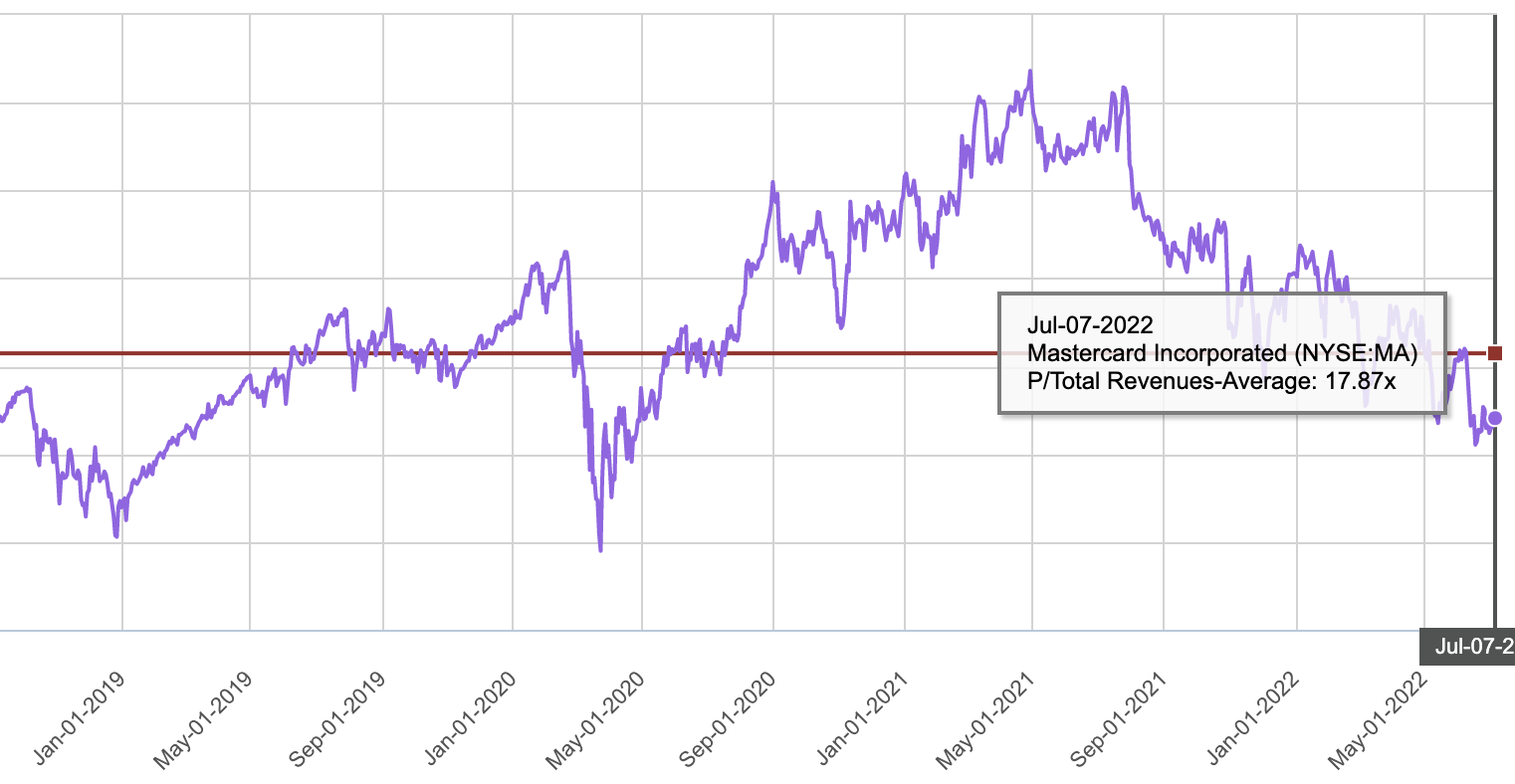

Price/Sales (P/S) ratio (5 Year)

The current P/S Mastercard stands at 15.97x while it’s 5-year Avg P/S ratio stands at 17.87x

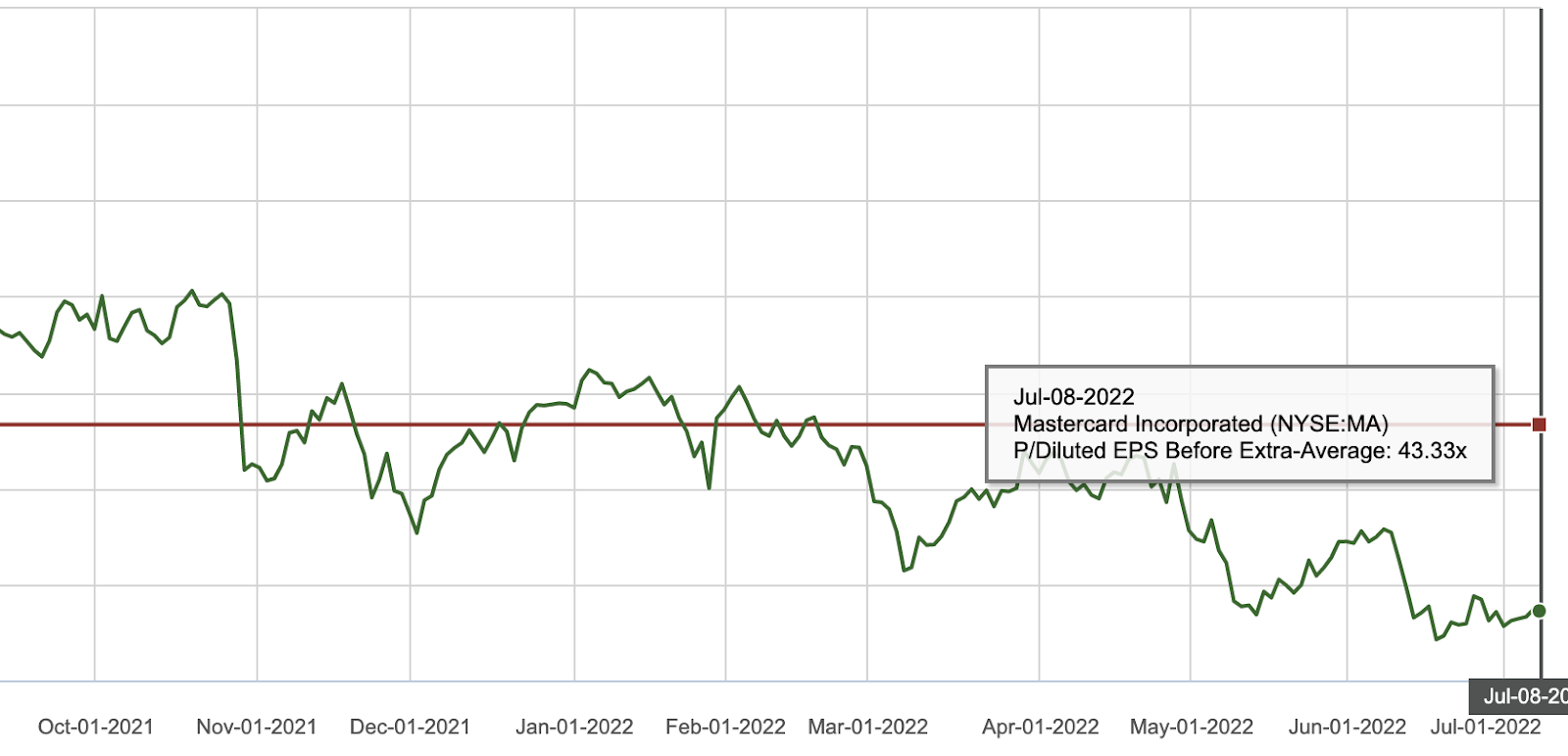

Price/Equity (P/E) ratio (1 Year)

The current P/E Mastercard stands at 33.62x while it’s 1-year Avg P/E ratio stands at 43.33x

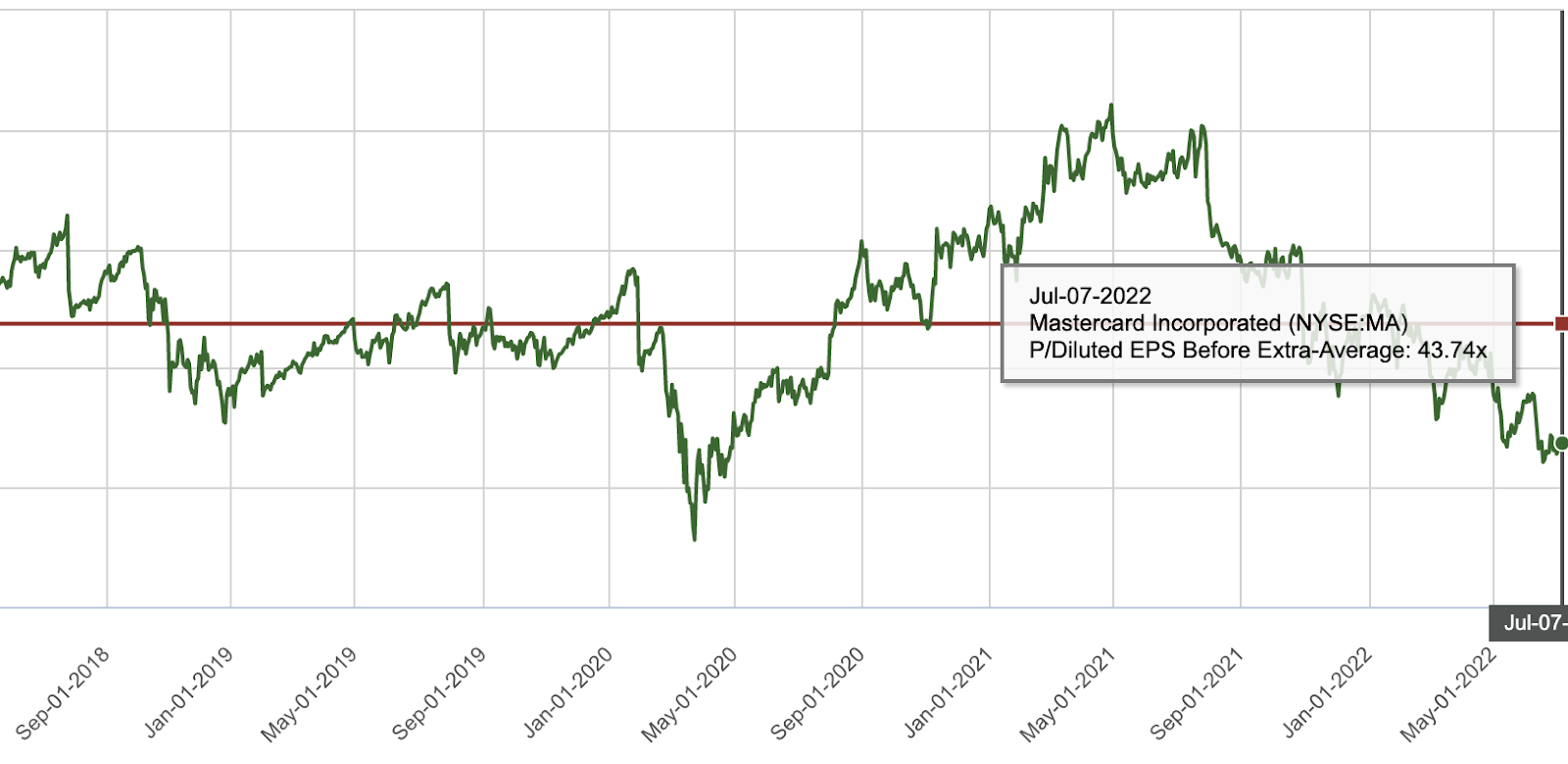

Price/Equity (P/E) ratio (5 Year)

The current P/E Mastercard stands at 33.62x while it’s 5-year Avg P/E ratio stands at 43.74x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs. On the other hand, operating profit margin also considers running expenses such as overhead. Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Mastercard’s financials, its EBITDA margin has been lingering around 50+%. Its operating margin has been sitting around ~50% while its FCF margin is around ~40%. An operating margin of more than 15% is regarded as good in most businesses as a rule of thumb. As a result, this clearly demonstrates that Mastercard has been doing alright financially.

Our Stand for Mastercard

Mastercard has definitely come a long way from a US-based payment processor to over 70 million global merchants. Hence, Mastercard is a great company with one of the strongest moats around with its strong payment network. However, there have been talks about new technologies like blockchain and other types of fintech that may threaten its position. Hence, Mastercard has also been actively investing in the crypto industry to ensure a vital role in the future of digital payments. Some examples include partnering with ConsenSys to increase transactions on Ethereum network and launching the CBDC Sandbox Test platform.

If you are keen to check out our article on other analysis: Nike, Apple and ETF. The current price appears to be fairly attractive with consistently strong margins. As a result, for the time being, this may be a good opportunity to consider Mastercard if you have not invested in it.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.

Thanks for this article. I would like to ask:

How did you get the value for “Mastercard typically charges from 1.35% to 3.25% for each transaction” ?

Hi Larry, we got this information from valuepenguin.com. You can head to this website to find out more: https://www.valuepenguin.com/credit-card-processing/interchange-fees