Growing up in an asian family, I have come to understand the immense value of saving money as an essential aspect of financial management. From an early age, I was taught that savings serve as a safety net during times of uncertainty, a foundation for major life events, a source of security during retirement and a pathway to achieving long-term financial stability.

Throughout my savings journey, I felt that having a high-yield savings account can significantly alleviate the burden of reaching my financial goals. Hence, in this article, I would like to share my personal choice of savings account and options that may be beneficial for fellow students that are interested in optimizing their savings!

What savings account are you currently using? Comment down below!

#1: GXS Bank (Saving Pockets)

What is GXS Bank?

GXS Bank is a digital bank backed by Singtel (40%) and Grab Holdings Inc (60%), they are on a mission to make banking better for Singapore’s everyday consumers and businesses. As it was launched in 2022, it gained a full digital banking license from the Monetary Authority of Singapore (MAS).

Why GXS Saving Pockets?

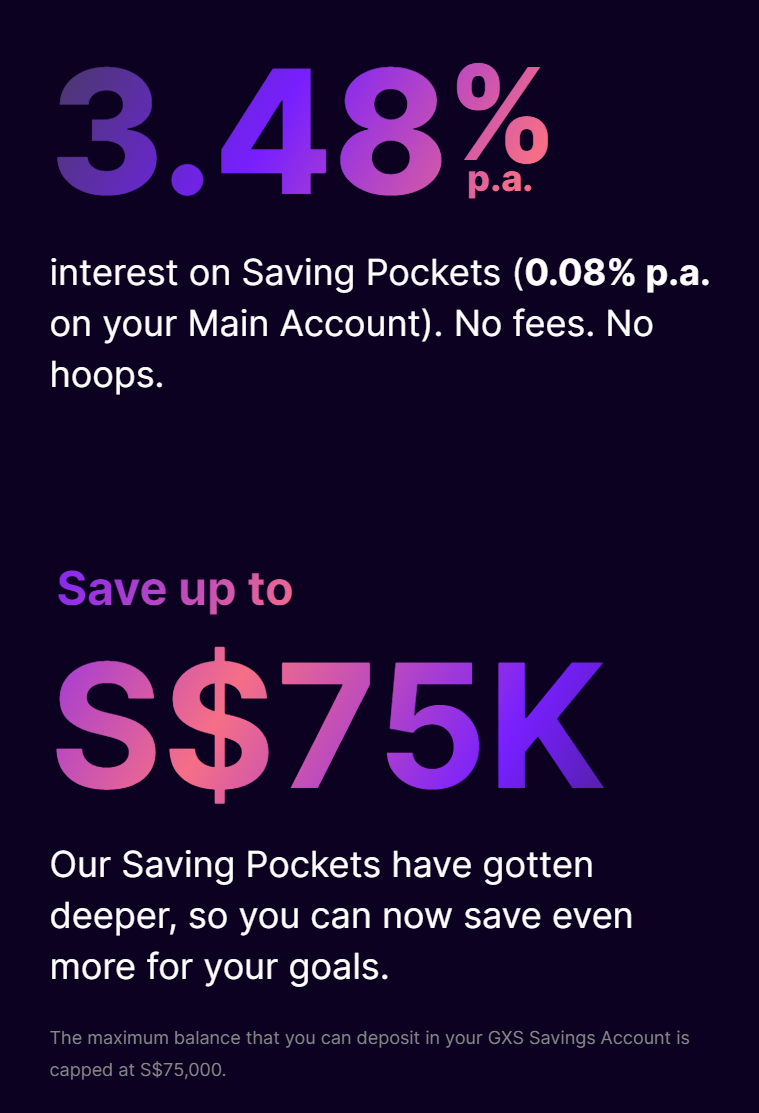

The most attractive feature about GXS Saving Pockets is their 3.48% p.a. interest on Saving Pockets (0.08% p.a. on your main account).

Furthermore:

- NO FEES.

- NO LOCK IN.

- NO PENALTIES.

- NO MINIMUM BALANCE.

- Interest credited daily.

- You can put a maximum balance of up to $75,000 inside these savings pockets!

What is bad about the GXS Saving Pockets?

As of now, there are very limited functions. Thus, there is no debit/credit card issued by GXS Bank. Hence, you will not be able to spend/deposit/withdraw cash any money directly from GXS. However, there are plans for GXS to offer its own debit card in the coming months.

#2: CIMB Fastsaver Account*

* For a limited time only (from now till 31 July 2023), earn 3.50%** p.a. From the first dollar, with a minimum deposit of S$1,000 for savings accounts. Maintain or increase your month-end balance to enjoy the promotion. Promotion ends on 31 December 2023)

What is CIMB?

CIMB is an indigenous ASEAN investment bank. CIMB has a wide retail branch network with 1,080 branches across the region. The group operates under several entities, which include CIMB Investment Bank, CIMB Bank, CIMB Islamic, CIMB Securities International and CIMB Thai.

Why CIMB Fastsaver Account?

The most attractive feature about CIMB FastSaver Account is their 3.50% p.a. interest in their savings account. (0.02% base cashback). There is no limit of how much savings you can put in the savings account.

What is bad about the CIMB Fastsaver Account?

Must Open the account online before 31st July 2023. Minimum $1,000 in fresh funds (for savings account) or $5,000 in fresh funds (current account). Maintain or Increase each month-end balance against the previous month-end balance. Interest credited monthly. For the extensive terms and conditions of CIMB Fastsaver Account, you can find it here.

#3: Standard Chartered JumpStart Account

What is Standard Chartered?

Standard Chartered is a British multinational bank with operations in consumer, corporate and institutional banking, and treasury services. Despite being headquartered in the UK, it does not conduct retail banking in the UK and around 90% of its profits come from Asia, Africa and the Middle East. Standard Chartered has a primary listing on the London Stock Exchange and is a constituent of the FTSE 100 Index.

Why Standard Chartered JumpStart Account?

The most attractive feature about Standard Chartered JumpStart Account is their unique value proposition curating an account for the young adults between 18 to 26 years old. JumpStart Account has many benefits, such as 2.00% p.a. interest in their savings account (up to S$50,000).

Furthermore:

- 1% cashback on eligible debit card spends.

- No lock-in.

- No minimum spends.

- No requirement for salary-crediting.

- No service or annual fees.

- There is no limit of how much savings you can put in the savings account.

- You can continue to maintain the JumpStart Account after you turn 26 years old.

What is bad about the Standard Chartered JumpStart Account?

You have to invest with SC to get the additional 0.5% p.a. Interest. You have to be between 18 to 26 years to sign up for the account.

#4: Trust Bank

What is Trust Bank?

Trust Bank is a digital bank, backed by Standard Chartered Bank and FairPrice Group. I believe this will revolutionize the way banking was previously conducted. Trust does not have any physical branches and they operate 24/7 allowing them to deliver a banking service that is easier and faster to use.

Why Trust Bank Savings Account (Debit Card)?

The most attractive feature about Standard Chartered JumpStart Account is the fusion of a multinational bank and social enterprise coming together to form a digital bank. Trust Bank Savings Account has many benefits, such as 1.50% p.a. base interest in their savings account (up to S$75,000).

Furthermore:

- 0.22% base cashback (unlimited) on eligible debit card spends.

- No lock-in.

- No Monthly Fee.

- No Minimum Balance.

- No Account Closure Fee.

- No Foreign Transaction Fee.

- No Card Replacement Fee.

- Decent amount of partner merchants.

What is bad about the Trust Bank Savings Account (Debit Card)?

A lot of the numbers shown on Trust Bank Savings Account have many prerequisites – “Up To”. Hence, a lot of the cost savings revolve around FairPrice Group. Need to make at least 5 eligible purchases (to get bonus interest of 0.5% to 1.0% p.a.) – is not hard, but requires more effort.

Our Stand

Indeed, in the realm of personal finance, there is no one-size fits all approach and the same holds true of selecting the ideal high-yield savings account. Each savings account comes with its unique sets of goods and bads. Finding the ideal high-yield savings account is like trying to solve a jigsaw; only by putting all the pieces together will you be able to solve this challenging task.

Moving forward, we are starting to embrace the era of digital banking, where traditional banks providing low interest rates, such as 0.05%, are becoming a thing of the past. Digital banks are disrupting financial institutions by providing more competitive interest rates and user-friendly interfaces that cater to the liking of the new generation of millennials and Gen-Zs.

In conclusion, the key in finding the best-high yield savings account lies in conducting thorough research, understanding our financial needs, and aligning the offers of various banks. Hence, let us start embarking on our journey with curiosity, diligence and a quest for your financial success. Remember, your financial puzzle is waiting to be assembled, and each piece chosen will shape the picture of your financial success!

In addition, do check out our other latest articles. If you are keen, check out our articles on other analysis: Trust Bank Referral, July Great Credit Card Deals, Investing in Meme stock journey.

Free USD18 with just a simple deposit of $1.

Lastly, looking for some good credit card deals, make sure to check back next week. We’ll be sharing some great offers that you won’t want to miss. In the meantime, if you have any questions about credit cards or how to use them wisely, feel free to leave a comment below and we’ll be happy to help.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before the usage of these products. We do not offer any warranty or assurance regarding the quality of these services or goods.

Best best best..