OCBC provides a variety of commercial banking, insurance and financial services, mostly in Asia-Pacific. Consumer/Private Banking, Wholesale Banking, Treasury & Markets, Insurance and others are among the company’s key business segments.

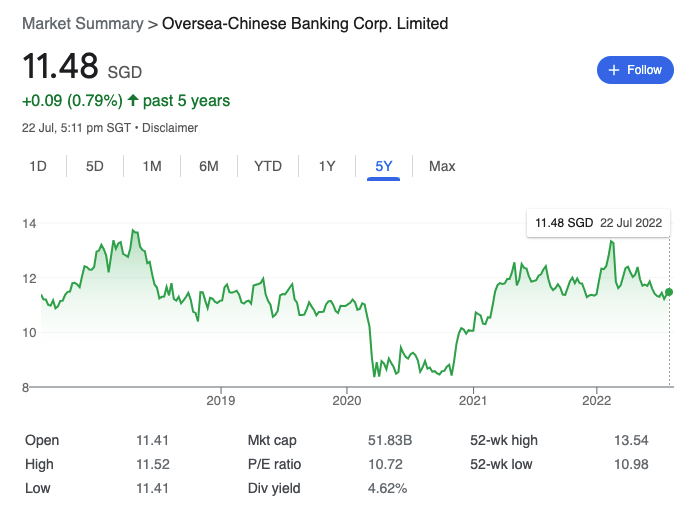

With OCBC down 20% from this year’s peak in February this year till today due to market uncertainty. Now may be a good time to discover more about OCBC and determine if this could be a good opportunity. Let’s now take a look at what the company has to offer.

Back in 2020, MAS requested for OCBC to lower dividends to buffer capital during the start of COVID-19. When the news was announced, it deterred investors and the stock price plummeted.

OCBC Bank is a popular bank among Singaporeans and also awarded the ASEAN SME bank for 11th consecutive years. More often than not, it is usually the second bank account that Singaporeans may open after a DBS Bank account. Its biggest shareholders are Citibank and DBS Nominees which stands at ~16% and ~11% respectively.

An Overview of OCBC’s Business

1. Key Product & Services under OCBC

The 4 main operating segments are as follows:

Qualitative Factors affecting OCBC

Let’s now take a deeper look into the qualitative aspects that affect the business.

Growth Opportunities

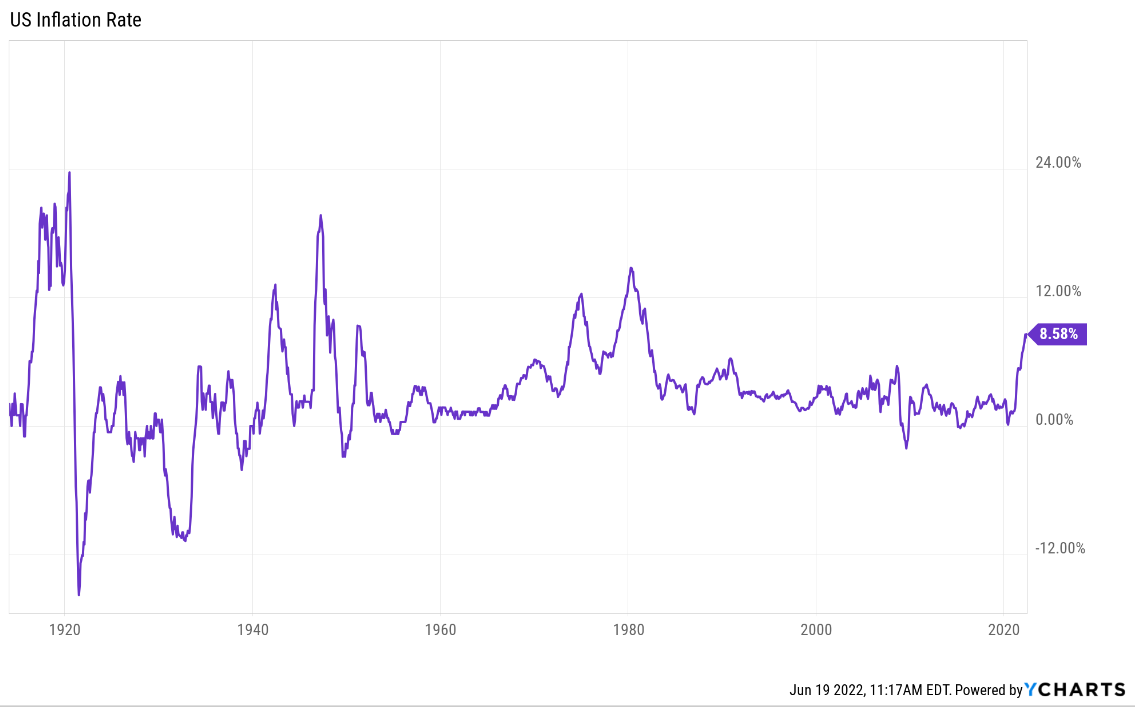

1. Rising Interest Rate Environment

In May 2022, inflation reached 8.58%, its highest level in 20 years. To avoid hyperinflation, the Federal Reserve Board (Fed) must raise interest rates in order to cool an overheated economy and lower inflation. The latest 0.75% (during June) increase in interest rates was the greatest since 1994, when the rate was 1.75% at the time of writing (19th June 2022). It will gain from this climate since increasing interest rates will allow them to charge higher rates on their loan and financing solutions. These are important to banks, like OCBC since they are how they generate net interest revenue for their total income.

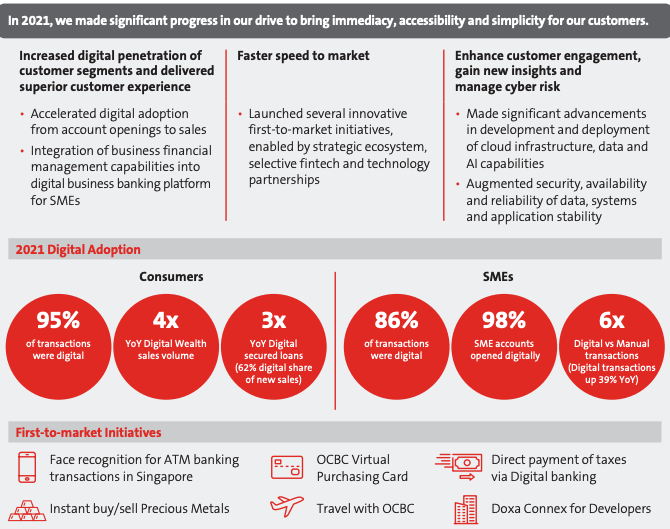

2. Accelerating Digital Transformation

OCBC has been placing greater emphasis on digital transformation. Some of its new endeavours include the new AI Lab@TOV which was launched in 2018. They aim to boost the usage of AI in banking services like wealth management and loan financing. The goal is for targeted and personalised products and services to provide OCBC customers with better value. Thus, in 2021, OCBC witnessed almost a 4-fold increase in their Digital wealth sales as compared to the prior year.

Business Risks for OCBC

1. Fraud Risks

In 2021, OCBC witnessed a sharp rise in SMS phishing scams impersonating the Bank over the past few weeks. Between 8 to 17 December 2021, 26 clients reported losses from scams of around $140,000. Given the circumstances, the Bank has provided full goodwill reimbursements for the affected clients. Hence, OCBC has introduced multiple measures to bolster its security. Some measures include 24-hour cooling off period for account changes, “kill switch” to freeze accounts and dedicated fraud hotline.

Together with Association of Banks in Singapore (ABS) and MAS, OCBC will continue to review and enhance fraud detection and prevention measures.

2. Market Risks

These are risks related to shifting interest rates, currency exchange rates, stock and commodity prices. Due to its trading, customer servicing and balance sheet management activities, OCBC Bank is exposed to several market risks. The current supply and demand changes resulting from the Russia-Ukraine conflict has affected prices for the equity and commodities markets. However, the bank does have measures like Stress Testing and Value-At-Risk calculation in place to quantify market risk exposures.

3. Counter-party Credit Risks

Credit risk remained the most important risk for OCBC in 2021. COVID-19 had a significant influence on several of these customers in the aviation and hospitality industries. Furthermore, the interest rate is expected to rise in the following months in order to combat inflation. As such, some of these clients may find themselves in an over-leverage position. This is because they did not consider the growing interest rate when taking out a loan previously. These clients will need to be identified sooner to mitigate any chances of default.

While OCBC does an excellent job of managing such clients, credit risk is likely to be the most significant and emerging risk among the others.

Quantitative Factors affecting OCBC

Let’s now take a deeper look into the quantitative aspects that affect the business.

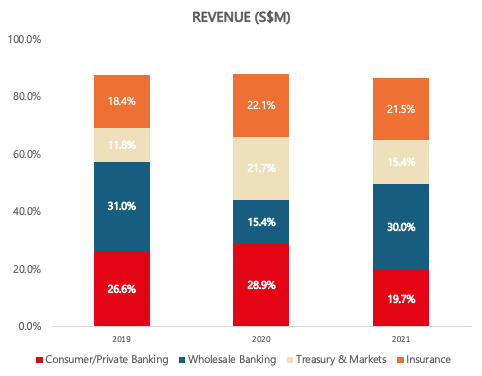

1. Financial Highlights – Total Income (Breakdown)

The majority of OCBC’s revenue in 2021 still predominantly comes from their Consumer and Wholesale Banking, at around 50% over the last 3 years. Throughout the last 3 years, we have seen a shift of income in banks as they tide through the pandemic. Segments like Insurance are increasingly growing as more consumers are taking more precautions in the period since 2020. Thus, revenue from the Insurance segment has increased from 18.4% in 2019 to 21.5% in 2021. Furthermore, as the Covid-19 situation stabilises, there is also a resurgence of Wholesale Banking to ~30% of the total revenue.

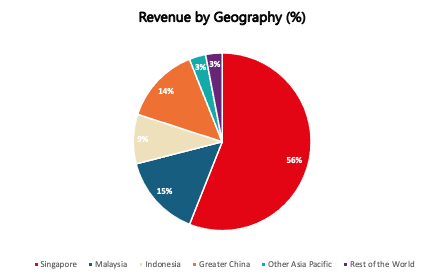

In 2021, Singapore and Malaysia accounted for over 56% and 15% of its revenue respectively. The remaining revenue are contributed from 14% in China, 9% in Indonesia, 3% in other Asia Pacific, and 3% for the Rest of the World. China and other Asia Pacific region revenues were partially impacted due to the Covid-19 and economical conditions.

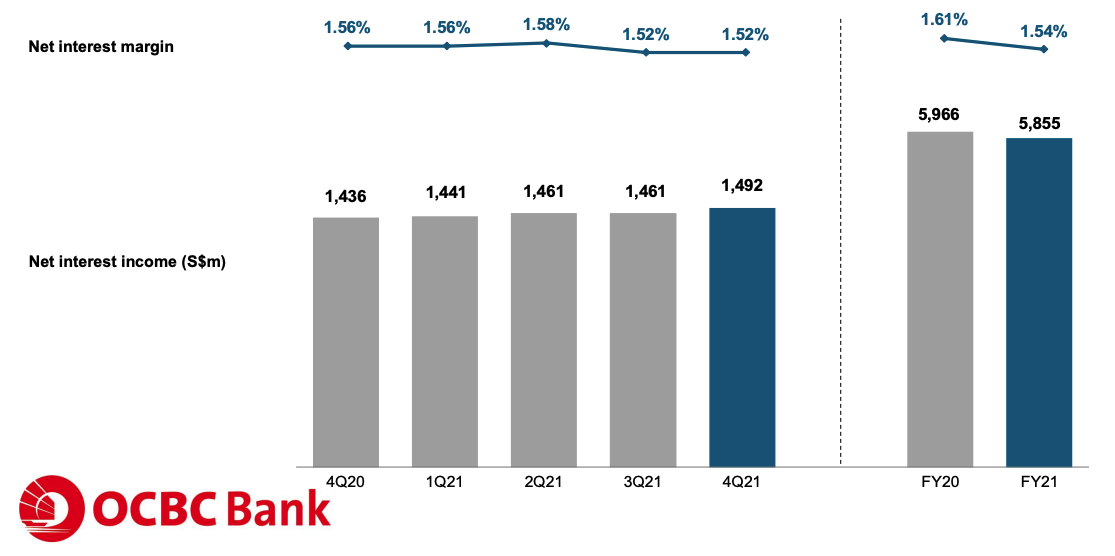

2. Net Interest Income, Net Interest Margin

Net interest income declined 2% to SGD 5.86 billion. Net Interest Margin fell 7 basis points to 1.54%. This is because benchmark interest rates used for pricing loans remained low.

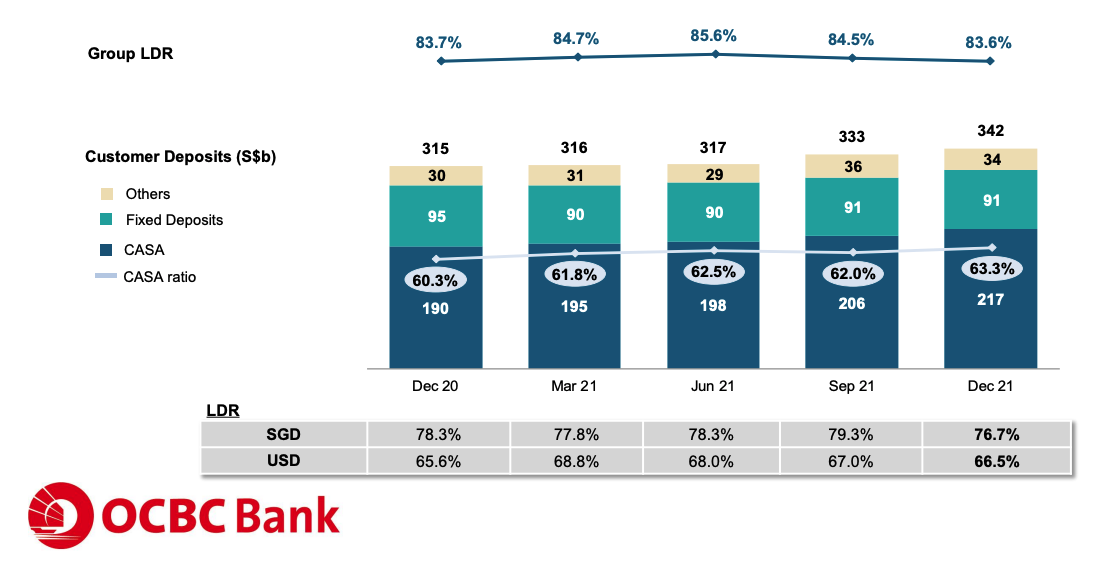

3. CASA deposits (Current Account, Savings Account)

Deposits rose by 8.6% to SGD 342 billion. CASA (Current Account, Savings Account) deposits grew by SGD 27 billion. As a result, the CASA ratio rose from 60.3% to 63.3%.

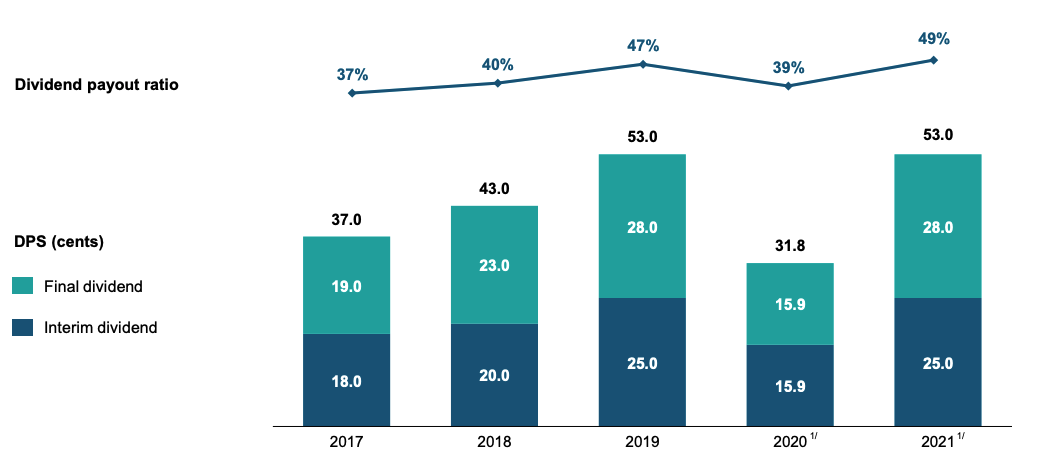

4. OCBC Dividend Payout Ratio & Dividend Per Share

Dividend per share for OCBC has resumed back to pre-covid period at SGD 53.0 cents per share.

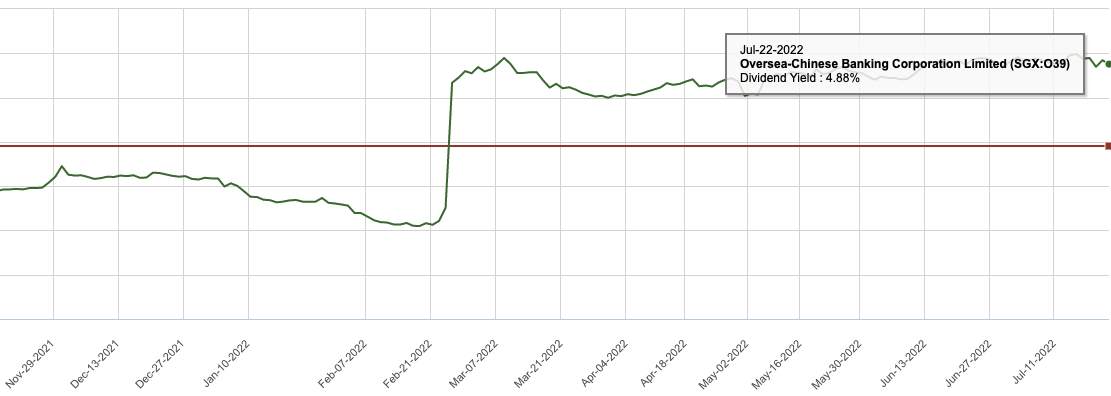

5. Dividend Yield for OCBC

Dividend Yield (1 Year)

The current OCBC dividend yield stands at 4.88%, while its 1-year average dividend yield stands at 3.95%. The sudden spike in dividend yield is due to the 4Q final dividend announcement date. Hence, the big spike.

Dividend Yield (5 Year)

The current OCBC dividend yield stands at 4.88%, while its 5-year average dividend yield stands at 3.97%. The huge decline in dividend yield back in August 2020 was because MAS capped banks’ dividends. Hence, OCBC’S dividend per share was reduced to SGD 31.8 cents per share for 2020.

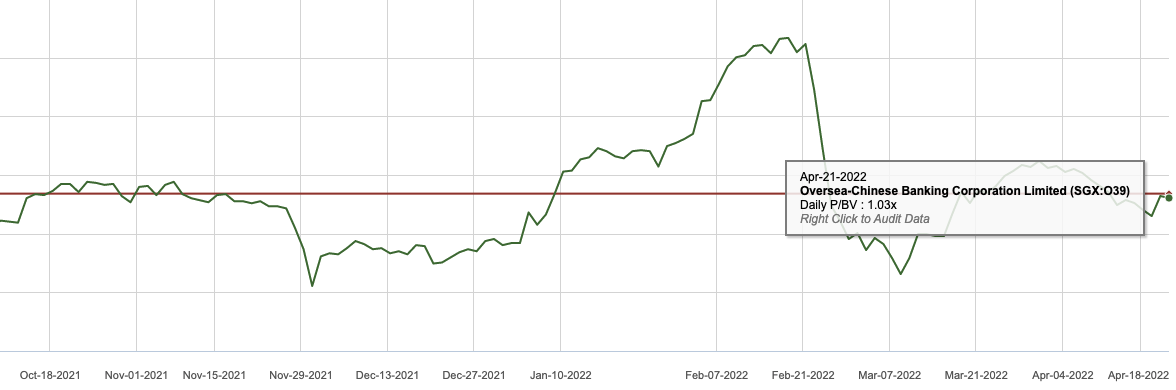

6. P/B for OCBC

Price/Book (P/B) ratio (1 Year)

The current OCBC P/B stands at 1.03x while it’s 1-year Avg P/B ratio stands at 1.03x

Price/Book (P/B) ratio (5 Year)

The current OCBC P/B stands at 1.03x while it’s 5-year Avg P/E ratio stands at 1.10x

Our Stand

OCBC has managed recent challenges very well, including the US-China trade war and the recent pandemic-driven downturn. Furthermore, OCBC management has continued to enable its banking, wealth management and insurance businesses to perform strongly. The outlook for OCBC looks relatively optimistic:

- Interest Rate rising environment

- Focus on Digital Transformation

- Seizing opportunities and unlocking value from Asia’s growth

While OCBC is trading around SGD 11.48 today (24th July 2022), I feel that it may be too expensive for me to pick up some shares. Therefore, I will definitely add this solid blue-chip bank to my watchlist and wait before I nibble up some shares. If you are keen to also read up on our recent analysis on other Singapore stocks: DBS or Ascendas REIT.

Disclosure: No position in OCBC.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.