DBS Group is a leading financial services group in Asia with a presence in 18 markets. Headquartered and listed in Singapore, DBS is in the three key Asian axes of growth: Greater China, Southeast Asia, and South Asia. As of 31 December 2022, DBS has total assets of S$743 billion.

Since the lifting of the dividend cap, the stock prices of Singapore banks have continued to rise rapidly. I want to learn how DBS intends to leverage through the rising interest rate environment. Hence, here are 8 things I learned from the 2023 DBS Group AGM.

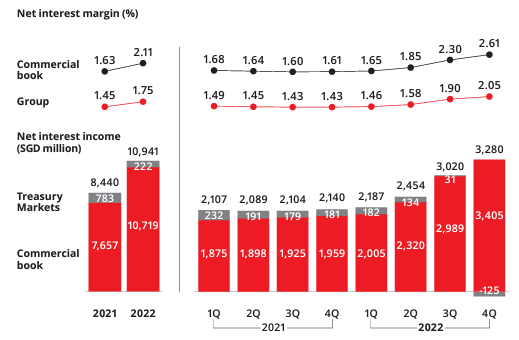

1. Total income increased 16% year-on-year to S$16.5 billion in FY22 from S$14.3 billion in FY21. Net interest income increased 40% to S$10.7 billion. The increase was boosted by a higher net interest margin as interest rates rose, as well as loan growth. Net interest income grew 11% in the first half and 48% in the second half compared to the year-ago period.

Treasury Markets decreased 22% to S$1.2 billion primarily due to lower investment product sales. Investment banking fees were also lower, as capital market activities slowed.

2. Net profit increased 20% year-on-year to a record S$8.2 billion. Earnings were propelled by tailwinds from a rising interest rate environment. Return on equity at 15%, was not just a record, but also significantly higher when compared to previous highs around the 12-13% range. .

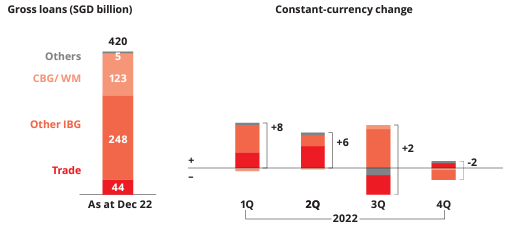

3. Loan growth grew 4% or S$14 billion in constant-currency terms to S$420 billion. CEO Non-trade corporate loans increased 5% or SGD 13 billion from broad-based growth across countries and sectors. Trade loans rose 4% or SGD 2 billion, with an increase in the first half partially offset by a decline in the second half due to unattractive pricing. Housing loans grew 4% or SGD 3 billion, with the majority of the growth occurring in the second half. Other consumer loans fell 7% or SGD 3 billion as wealth management loans declined.

4. CASA (current account, savings account) ratio decreased to 60%. CASA deposits did flow out in the second half as expected. This is because interest rates rose and half of the earlier inflows did stay with DBS. DBS ended 2022 with CASA deposits of S$318 billion. The expanded CASA enabled DBS to enjoy higher leverage to rising rates than in prior years. Hence, this contributed to the strong total income growth.

5. DBS declared a full year dividend at $2.00 per share, 4Q dividend up to 42 cents per share with a special dividend of 50 cents per share. This is in line with DBS policy of paying sustainable dividends that grow progressively with earnings. Barring unforeseen circumstances, annualised dividend will be S$1.68 per share.

6. DBS CEO Piyush Gupta did share his macro economic outlook. While uncertainties remain, macroeconomic conditions are improving. The DBS Management team do expect interest rates to hold for the rest of the year. Moreover, China’s reopening will begin to benefit the regional operating environment. There are also potential tail risks which are highlighted as well, (1) Uncertain impact of high interest rates, (2) Ongoing US-China geopolitical tensions and (3) Volatile market conditions.

7. The DBS Management Team also shared about the business outlook. Net Interest Margin guidance of 2.25% with 5-7bps downside risk due to outflows to T-bills, strengthening SGD and higher Treasury Markets funding costs. They also gave full year guidance of mid-single digit loan growth, double digit fee income growth. The Cost growth guidance at 9-10% which will bring the full year cost income ratio to come in just below 40%. Moreover, DBS’s capital and liquidity positions remain extremely strong.

8. Digital Transformation has been a key focus for DBS. DBS has been enhancing their digital platforms and increasingly using data and artificial intelligence to provide them with the tools and insights to manage wealth on their own. DBS is investing heavily in technology and innovation, and the bank’s digital initiatives have helped it to reach new customers and provide better services. The management team expects these technologies to converge and bring forth extraordinary use cases.

Our Stand

In conclusion, the DBS 2023 AGM provided valuable insights into the bank’s performance, strategies, and plans for the future. DBS’s commitment to digital transformation are positive developments that bode well for the bank’s long-term success. As an attendee, I am optimistic about DBS’s future prospects and look forward to seeing the bank continue to thrive in the years to come.

The rising interest rates was indeed a huge catalyst for DBS Group. As of now, the interest rates seem to be near the top and DBS might soon run out of steam or any tailwinds. At S$32.57 a share (as of 15 April 2023), DBS Group price-to-book ratio is 1.45, which is higher than its long-term historical average of 1.25. Although there may be some upside left, DBS looks expensive.

Furthermore, if you have yet to open a Webull Account, head here as we show you a quick guide to get Free USD50 with just a simple deposit of $1.

If you are keen, check out our articles on other analysis: Trust Bank Referral, Diversification Strategies for a well-rounded portfolio and Standard Chartered Credit card deals.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.