Lockdowns have become the new norm as a result of the COVID-19 pandemic. Physical purchases of goods have increasingly become something of the past. Businesses and customers are becoming “more digital” as they provide and buy more products and services online. According to Statista, ecommerce will account for 20% of all global retail trade in 2022, up from 14% in 2019. One company that has greatly benefited from this trend is Sea Limited (NYSE:SE).

It is one of the largest e-commerce and digital entertainment platforms in ASEAN. Over the pandemic period, it has seen its revenue increase by more than threefold. Despite significant growth in revenue, the company has had trouble turning a profit. This is partly attributed to high operating expenses, rising interest rates, and low e-commerce profit margins. As a result, many would say that 2022 was not a fantastic year for Sea Limited investors. The stock has declined by over 70% in 2022 alone.

Hence, we have witnessed Sea Limited make significant moves to transition from unconstrained growth to Profitability. This includes top management forgoing salaries during multiple rounds of layoffs, limiting travel expenses, and more. On March 7th, Sea Limited recently released its Q4 earnings. In this article, we’ll examine the most recent earnings report in greater detail and explore its long-term prospects.

Key Highlights of Sea Limited’s Q4 Earnings

1. Ecommerce Business (Shopee) strong revenue growth and Positive EBITDA

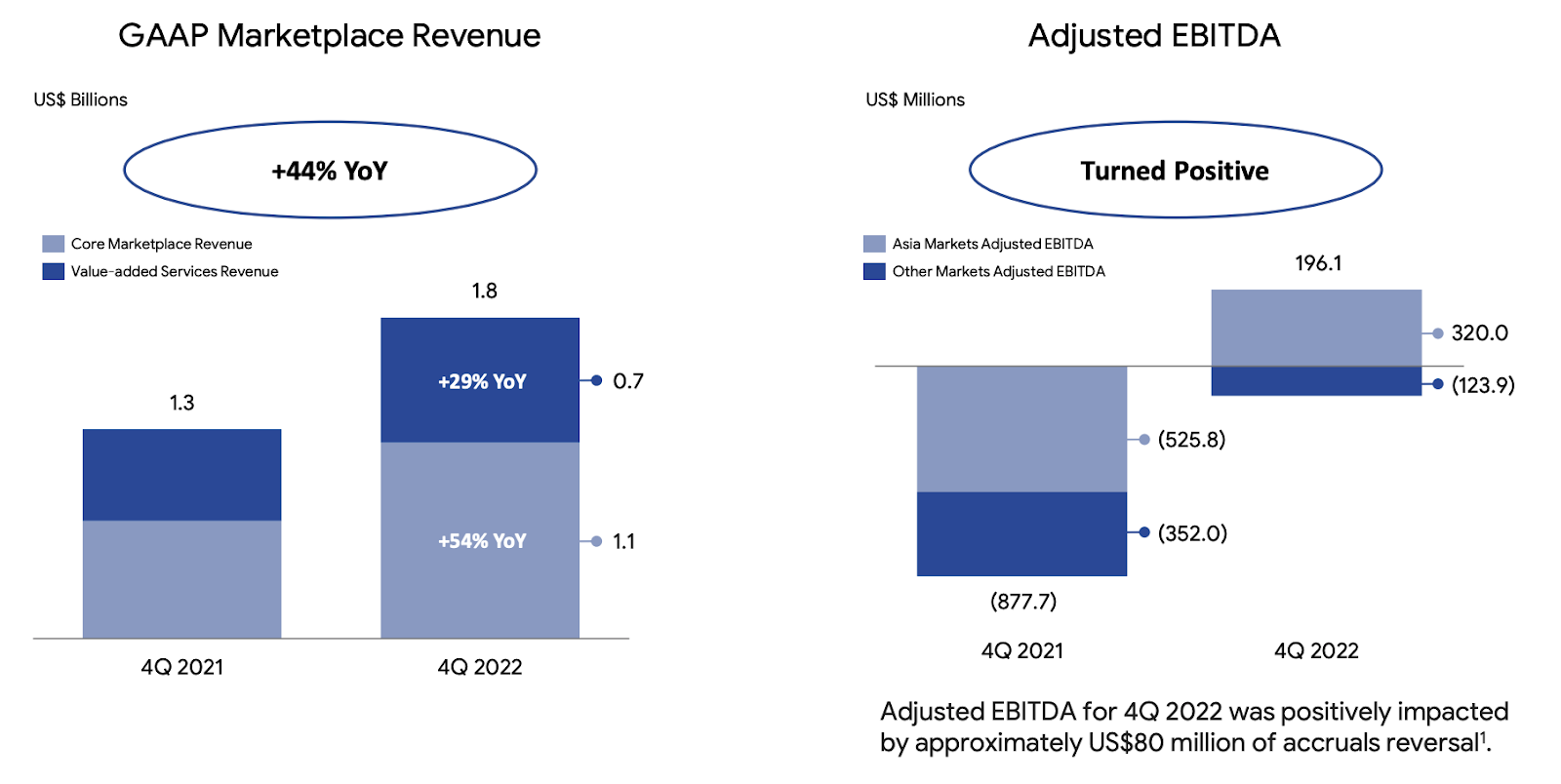

Shopee reported total revenue of US$1.8 billion for the fourth quarter of 2022. It increased its core marketplace revenue by 29% year over year to US$0.7 billion. This was primarily due to higher transaction-based fees and advertising revenue contributed by platform sellers in order to better serve buyers. As a result, Shopee’s quarterly EBITDA has turned positive for the first time. It has reported US$196.1 million in EBITDA due to revenue and operating cost improvements. Additionally, full year revenue performance generally mirrored the strong growth in the fourth quarter, growing 44% from 2021.

2. Digital Entertainment (Garena) business slumped drastically

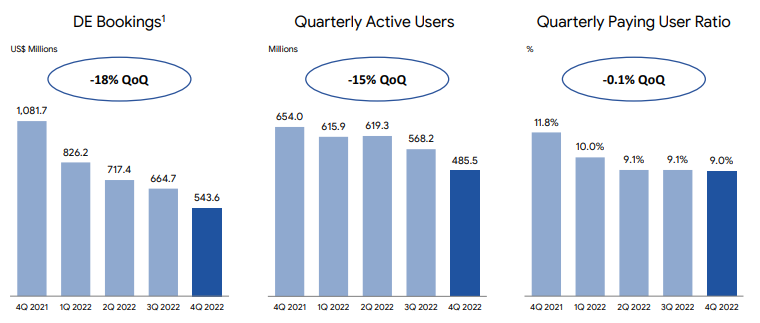

This quarter has been challenging for its Digital Entertainment business, with overall booking revenue of US$544 million. This is down 18% from its previous quarter. Bookings is an operational metric that approximates the amount of money spent by users during the relevant period. The market has been broadly affected by moderation in user engagement and monetization across various regions’ regulations.

Furthermore, it has quarterly active users of US$ 486 million with 44 million quarterly paying users. This is a 15% decrease from its previous quarter. Revenue and profitability have suffered as a result of a drop in both bookings and quarterly paying users.

3. New growth engine in its Digital Financial Service Business (SeaMoney)

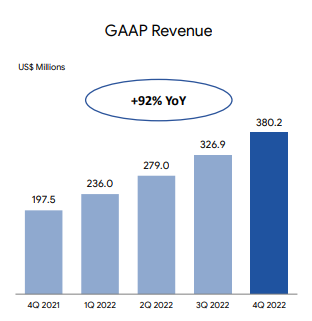

In the fourth quarter of 2022, SeaMoney’s revenue was US$ 318 million, up 92% year over year. This was also its fourth positive EBITDA quarter at US$ 76 million. Profitability increased as a result of both strong revenue growth and optimization in sales and marketing spending. In addition, for the full 2022 year, its revenue was at US$ 1.2 billion, up 150% year over year.

4. Overall Sea Limited Group Performance demonstrated improved Profitability

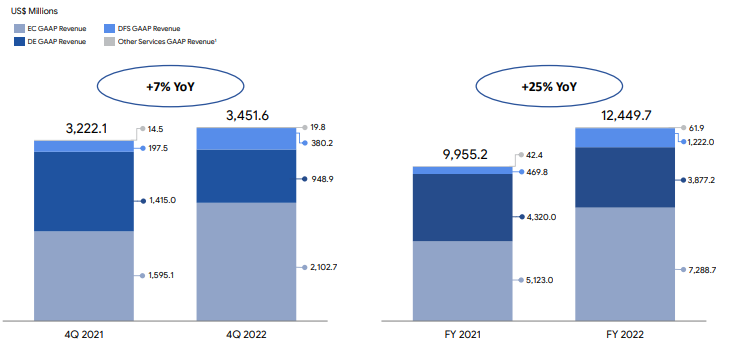

In the fourth quarter, Sea Limited’s total revenue increased 7% year on year to US$ 3.5 billion. It increased by 25% year on year to US$ 12.4 billion for the full year. As seen earlier, this was primarily driven by improved monetisation in its ecommerce and digital financial services businesses.

Strategic Initiatives taken by Sea Limited for 2022 and Beyond

1. Enforcing principle of “doing less, but doing it better”

Going forward, Sea Limited has embraced this principle and plans to focus on areas with the greatest potential. This includes measures like exiting or downsizing non-core market operations. For instance, Shopee has already announced the closure of operations in Poland, Argentina, Chile, Colombia, and Mexico as of 2023.

Furthermore, Sea Limited intends to streamline its investments by closing or deprioritizing non-core initiatives. In particular, Garena has already halted its game live stream service Booyah! and closed projects that are still in development. This is expected to assist the company in providing immediate cost savings and better allocate its operational and financial resources.

2. Shopee continual pursue for Logistics optimisation

Shopee has done exceptionally well for its fourth quarter and the management plans to continue solidifying its returns. As such, their long term focus will be on its Logistics optimisation which includes lowering cost while improving user experience. For example, in Asia, they will continue to leverage on its leading position to expand its logistics partners network. This will enable Shopee to compress partner pricing and provide the best price for both buyers and sellers.

In addition, Shopee conducts periodic reviews of their customer service process management. This review focuses on topics such as reducing wait times and minimizing delivery losses. Their goal is to make logistics management on their platform more seamless for both buyers and sellers.

3. SeaMoney as the growth engine to bind and grow its digital ecosystem

Today, the SeaMoney services include mobile wallets, point of sale, BNPL, merchant financing and banking. However, SeaMoney’s main role will be to handle payments for its other business, Garena and Shopee. Through the transactions it processes, it will be able to provide Garena and Shopee with insights on their user habits. Leveraging these insights will allow the business to identify popular purchases and possibly use them to expand their user base.

Additionally, these insights could also expand into underwriting insights for Sea Limited to manage the risks posed by different users. As a result, we can expect Seamoney to serve as an important long-term engine for all of its digital ecosystem.

Investment Analysis: Is now a good time to buy the stock?

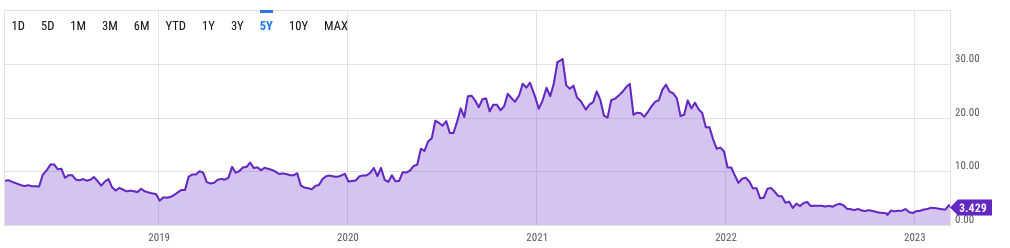

The fourth quarter has definitely been one of Sea Limited’s better performing quarters. After its earnings results, its share price has increased by more than 12%. However, is this really a good time to look to start purchasing the share? In order to better determine this, we have to examine several important indicators like Price/Earnings and Price/Sales ratio. As Sea Limited is still currently unprofitable, the PE ratio may not be that appropriate of an indicator.

As such, we will only be focusing on the P/S ratio. Its current PS ratio stands at 3.429. This seems fairly attractive as compared to its 5 year average of 11.86.

Conclusion

For investors who haven’t yet invested in Sea Limited, the share price of US$ 74 does look rather appealing. Personally, I would place a small position if I have yet to invest in the company. However, be aware this is the first quarter that the company has reported positive net income. As a result, we will advise investors to enter in tranches and observe patiently for a couple more earnings results. This is to ensure that Sea Limited is on its right trajectory of growth and profitability.

Disclosure: Do have existing position in Sea Limited shares.

If you are keen, check out our articles on other analysis: Trust Bank Referral, Best Transport cashback and Standard Chartered Credit card deals.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.