If you have been investing, you would know that 2022 hasn’t been the best year in terms of investment returns. The number of threats to the US economy has risen considerably in the first four months of 2022. This has left many investors unsure how to effectively protect their portfolio. E.g. Crisis in Ukraine and rising interest rates, as well as sky-high inflation and slowing economic development

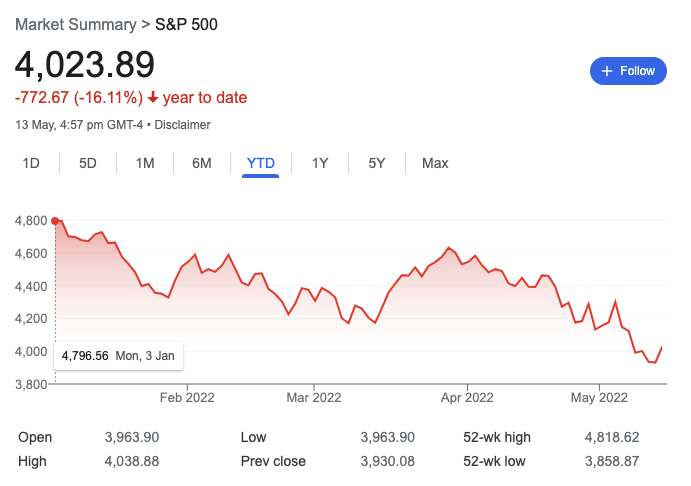

Since the beginning of the year, the S&P 500 has dropped by 16%. On the other hand, the Nasdaq and cryptocurrency like Bitcoin have also declined by 26% and 36% respectively.

It might be intimidating for investors if this is the first huge decline or recession you are experiencing. Before you do anything drastic, here are 5 tips to better prepare your portfolio in times of recession.

1. Reassess current portfolio

If the recent market correction has impacted your portfolio, now is an excellent moment to reassess it. Reassessment differs from rebalancing a portfolio as it mainly involves one requestioning each of their investment. Take some time to consider why you bought these stocks or funds from your Investing Journal. There are a variety of reasons why one would buy their stock or fund. E.g. Good valuation, potential growth outlook, hype, circle of competence etc.

Some questions you could ask yourself now:

- Why did you make this investment?

- Is your initial reason for purchasing the stock or fund still valid?

- Are you still confident of its potential growth of the stock?

- Has the fundamentals of the business changed for any of the investments?

If the fundamentals of the business have changed then one may consider to reduce or sell the investments. That is why it is key to have an Investing Journal to pin down one’s investment journey. If you haven’t started a journal yet, don’t be hesitant to do so. It not only clarifies your thoughts and investment purpose but also generates a solid journal for future evaluation.

2. Think of long-term goals and formulate an investment plan

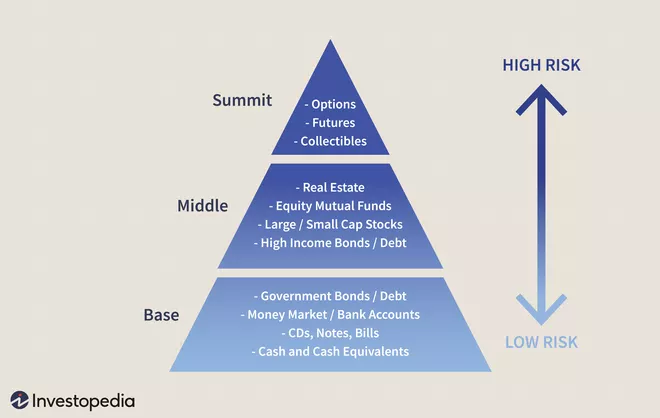

85% of Hedge Fund Managers has failed to consistently beat the index thus illustrating the difficulty of active investing. The S&P 500 returned nearly twice as much as the average hedge fund from 2011 to 2020. Thus, as an investor, one should set their financial goals based on their risks and time horizons.

Below are different classes of assets which one can consider based on their risks. Generally, younger investors often dive into riskier investments as they have longer time horizons. However, there is no right answer to this and everyone’s portfolio is unique. Ideally, it should be a portfolio that lets one sleep well. Lastly, to begin, learn about the various financial assets and determine which one best meets your risk appetite.

3. “Buy the Dip” if you can

Consider market crashes as fire sales to help curb the panic. Do not be overly obsessed to time the moment when equities are at their lowest. Choose a few desired investments that one wishes to possess and set a price limit to purchase. At the current market condition, one might get a good deal if they decrease to or below that price level.

However, this is assuming that the investor is financially secured to buy during a market correction. Do not hedge bets on a volatile market if one may be facing unemployment or other financial issues. An emergency reserve is a better use of the money than a risky investment. Only “buy the dip” if one is willing to lose the money.

If you’re new to investing, do check out our latest articles: Tencent Stock and Costco Stock.

4. Stay invested for your Portfolio

Keep calm and remember that staying invested is almost always the best answer to bad headlines. The general guide is to have three to six months of living expenses saved up as an emergency fund. This may vary based on one’s family needs and expenses.

The excess beyond the emergency fund can then be channeled into investments. Historically, investors who stay on to their assets throughout recessions have seen their portfolios fully recover, while those who do not invest at all lose out. According to FactSet, even if someone had invested in 2007, they would have made 7.8 annualized returns after ten years.

5. Not Every Recession is the Great Recession

It is critical to distinguish between recessions of varying severity. The Great Recession of 2008/2009 was a banking crisis that resulted in a deep and long-lasting recession. However, in today’s economy, banks’ balance sheets remain solid which makes a repeat of the last recession unlikely. Thus, one should understand that given the low growth outlook, recessions may become more common but with less severity.

However, there may be additional variables that may contribute to a recession. Hence, the greatest thing an investor can do is keep up with the news to make a fair market assessment.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.