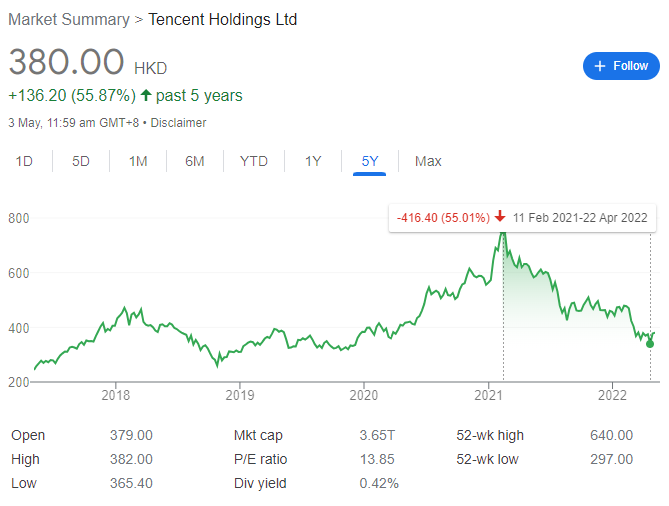

For more than a year, Tencent has also been on a downward trajectory, dragged down by regulatory fears. Recently, investors sentiment has been unfavorable toward Tencent shares due to several concerns. Potential delisting by the US SEC, China’s potential involvement in the Russia-Ukraine conflict just to name a few.

Tencent’s stock suffered a sharp drop after the company reported its slowest-ever growth due to a bruising crackdown by China on the country’s tech sector. This bruising crackdown started way back on 3rd November 2020, where Chinese regulators suspended Ant Group’s $37 billion IPO. In May 2022, China regulators signal ease of tech squeeze in bid to lift the China economy. As of today, Tencent has dropped drastically by ~55% from it’s all-time high. Many value investors have reiterated that most Chinese equities are currently undervalued and the market has bottomed. Hence, is this a good time to look into Tencent stock and consider buying it?

Overview of Tencent’s Business

Tencent was founded back in 1998 by co-founder Ma Huateng (also known as Pony Ma) which ranks among the nation’s largest businesses by market cap. Tencent publishes some of the world’s most popular video games and other high-quality digital content, enriching interactive entertainment experiences for people around the globe. Today, Tencent is a conglomerate which also offers a range of services such as cloud computing, advertising, FinTech, and other enterprise services to support our clients’ digital transformation and business growth.

Key Product & Services under Tencent

Tencent segregates its business into the following key segments: Value Added Services (VAS), Online Advertising, FinTech and Business Services and Others.

Operating Model

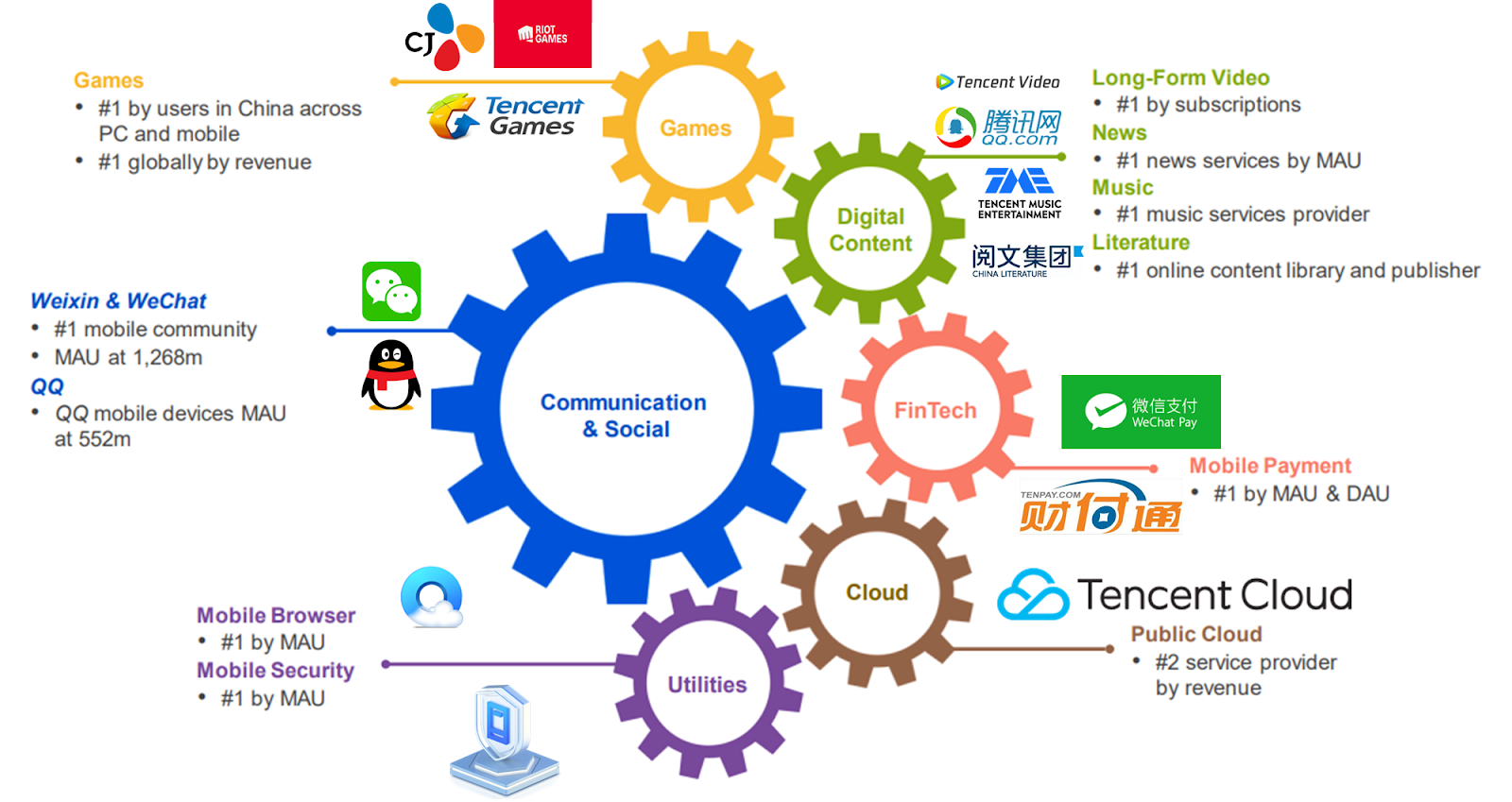

Tencent is a conglomerate in a series of technology-related spheres including video gaming, social media, entertainment, streaming and cloud services and advertising. Some of its most popular offerings include its instant messaging platform QQ, digital content like Tencent Games and Tencent Pictures, and fintech offerings WeiXin Pay and Credit Card Repayment. Furthermore, Tencent also focuses on AI and aims to be a leader in retail, healthcare, education and transport.

Qualitative Factors affecting Tencent

Let’s now take a deeper look into the qualitative aspects that affect the business

Tencent’s Economic Moat

1. Network Effects

Tencent is the #1 platform in many industries: Games, Long-Form Video, News, Music, Literature, Mobile Payment, Mobile Browser, Mobile Security, and of course its social media platform, Weixin/WeChat and QQ. In its essence, tencent is a huge (social) network with over 1 billion users, and over the past few years, Tencent has created a very complex and dense network. This allows every user to connect with one another which is difficult to replicate for other companies. As the value of a service or product increases with the number of people using it, the most valuable service or product will be the one that most people are using. Over time, we see a winner-take-it-all effect which is often referred to as the Matthews Effect.

2. Economies of Scale

Additionally, Tencent can rely on huge economies of scale due to the size of the company. The barriers of entry for Tencent to penetrate into another industry is easier as compared to other company’s. Thus, the reduction in Tencent’s costs to the generated revenue shows massive economies of scale (due to millions of potential users, leveraging on the network effect).

Growth Opportunities for Tencent

1. Advertising

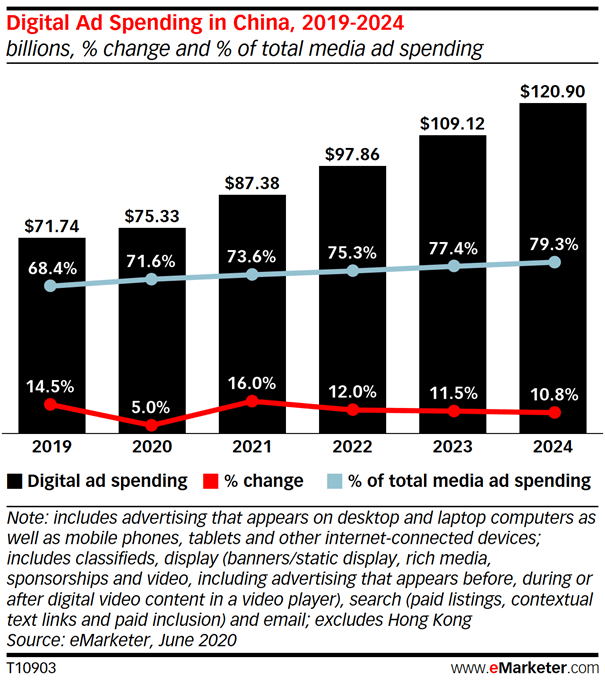

The digital ad spending in China, which is extremely important for Tencent, is expected to grow 16% in 2021 and between 10% to 12% annually in the following years.

As China is persistent on the Zero-Covid Policy, many states are seen on a lockdown even though the world is starting to open up. With lockdown, there is an increasing trend of people constantly on the web. Hence, many advertisers also flocked towards digitalisation and the cost for advertising is more valuable than ever. Tencent eCPM (effective Cost Per Thousand Impressions) rose last quarter, thanks to higher sales of video ads, indicating it still has plenty of pricing power in the crowded advertising market.

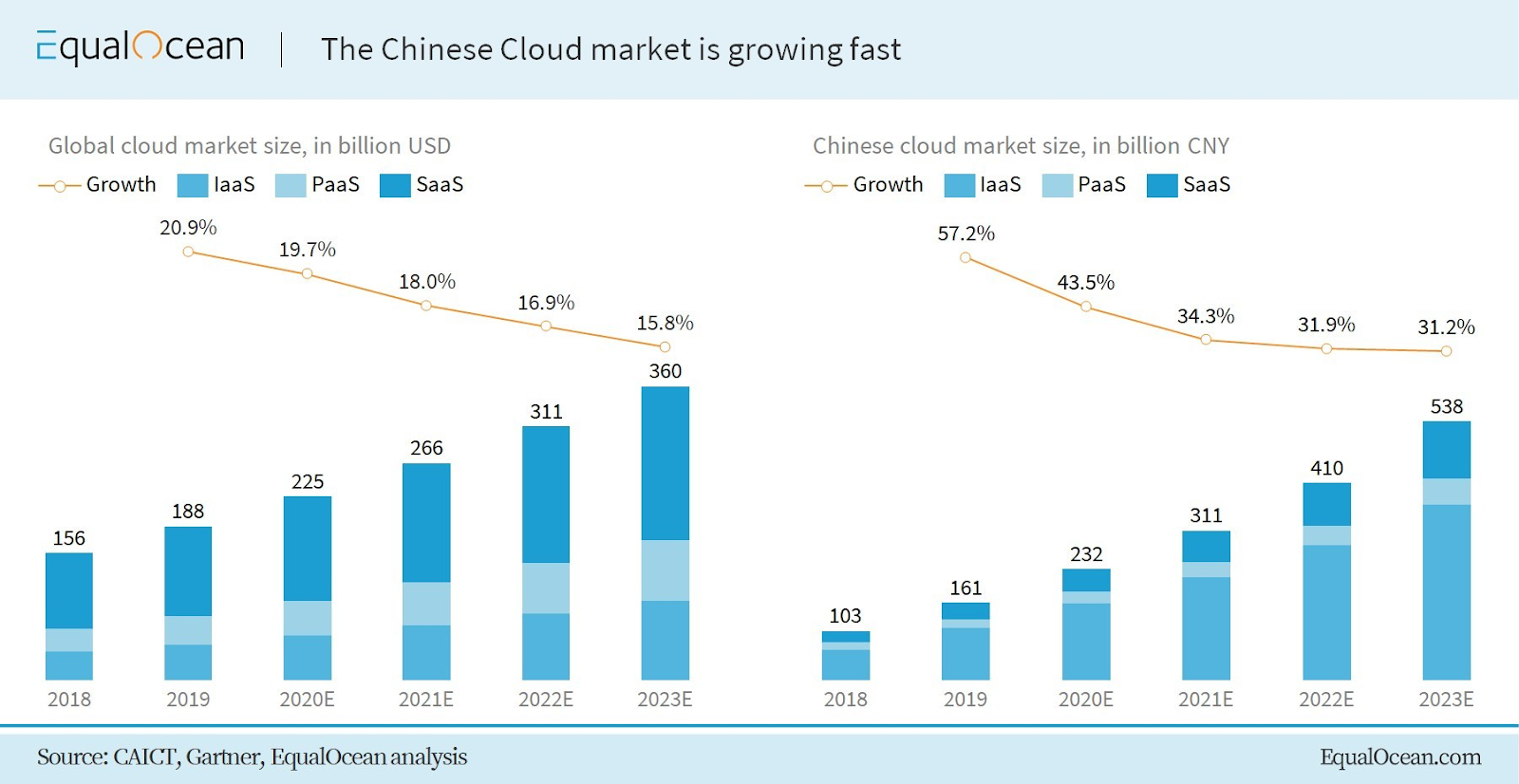

2. Cloud Computing

Tencent has invested a log of capital in developing Tencent Cloud and the business has been growing very quickly in the last few quarters. As a result, it has realized more scale that could potentially allow it to gain more margins. As the #2 player in China for Cloud, Tencent could be profitable within a few years as its competitors Tencent Cloud just became profitable in terms of positive adjusted EBITDA. Furthermore, the Chinese Cloud Market Size is increasing ~30%+ which shows tremendous growth. Tencent is in an unique position poised to benefit from this opportunity of the growing Chinese Cloud Market.

3. Investment Portfolio

Tencent has stakes in over 700 companies according to its 2Q2020 earnings call. Some of these companies are large and well-known such as Epic Games, Supercell, Activision Blizzard, Spotify, Roblox, Discord, Pinduoduo, Sea, Afterpay, Nio, Ubisoft, Meituan etc. As at 31 December 2021, the total investment portfolio amounted to RMB878.65 billion (USD ~132.96 billion – about 30% of its market cap (RMB2.98 trillion/HKD3.54 trillion)).

Business Risks

1. Regulatory Risks

The Chinese Communist Party (CCP) heavily regulates the Internet which could potentially disrupt the growth of Tencent. Some instances where the CCP regulated heavily are the crackdown of Bitcoin miners, EdTech companies and monopolistic behaviors of Big Tech firms in China. The question as to whether Tencent will be heavily regulated: No, I don’t think so. As of today (4th May 2022), many value investors claim that these Chinese stocks could possibly bottom and any further crackdown has already been priced in given its astronomical dip in price.

2. Competition – EA games, Facebook, Google and Bytedance

The 2 biggest players in China which dominate the whole economy are Tencent and Tencent. Unsurprisingly, parts of their business overlap each other which spurt monopolistic behaviors on each of their platforms – where one will not be able to share on another platform. The 3 key competitions which could disrupt Tencent growth are: Short-Form Video – Bytedance, Cloud – Tencent Cloud and Gaming – Netease. ByteDance, Tencent, and NetEase don’t directly compete with each other, but they all compete against Tencent. Therefore, investors should closely track their moves and see if they endanger Tencent’s evolution as a diversified tech company.

Quantitative Factors affecting Tencent

Let’s now take a deeper look into the quantitative aspects that affect the business.

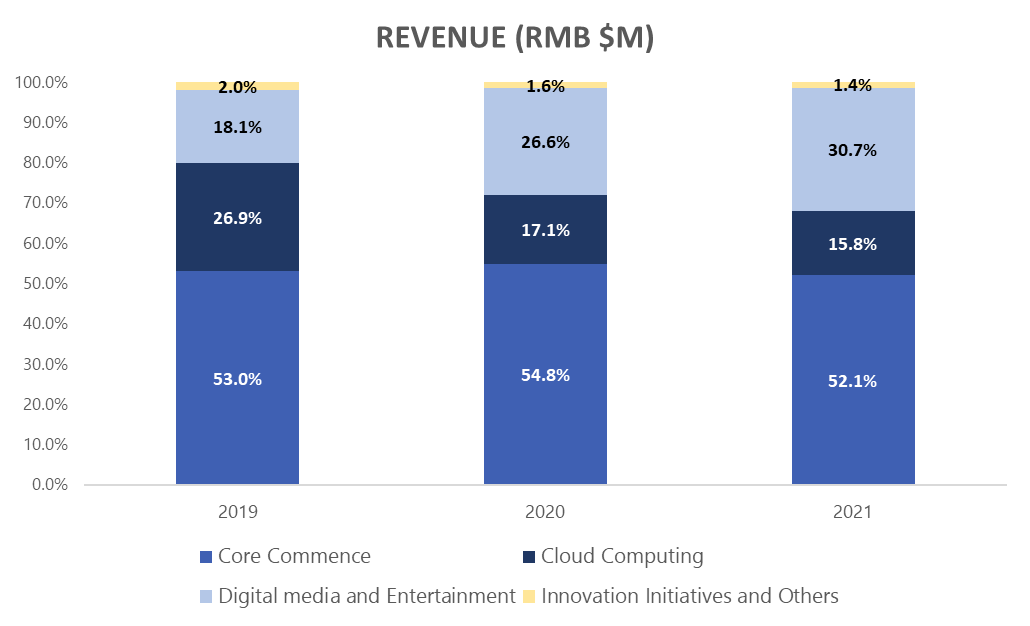

1. Financial Highlights (Revenue Breakdown)

The majority of Tencent’s revenue in 2021 predominantly comes from their core VAS business segment at ~52%. Its Cloud Computing business has grown tremendously over the years which together with their FinTech arm (payment services) contribute to ~30% of its revenue. The remaining revenue is split between Online Advertising (~15%) and Other (~1%).

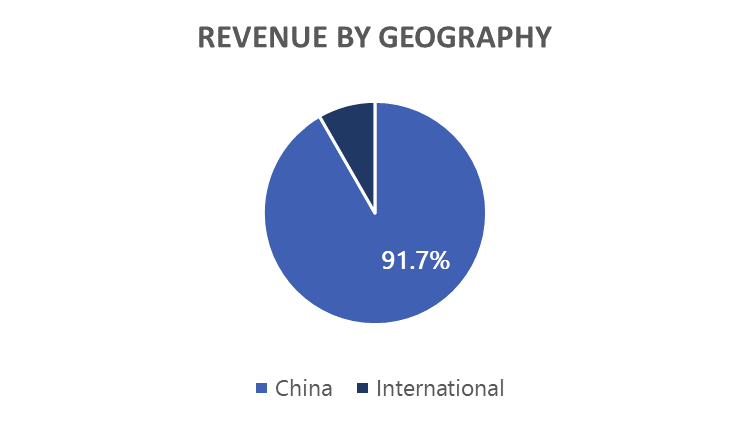

Without a doubt, Tencent’s core business came from China. It started out with the Chinese consumers which explains why ~90% of Tencent’s revenue still comes from China.

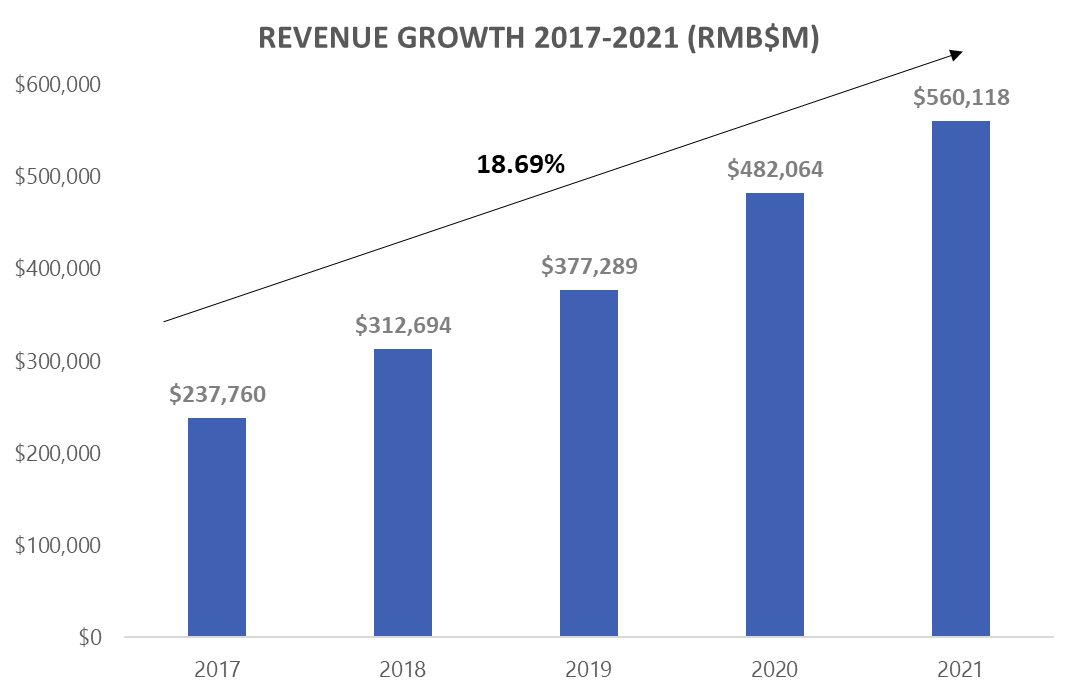

2. Revenue Growth (5 Year)

Tencent’s 2021 revenue is at RMB$560B with 16.4% (YoY growth) and 5-Year CAGR stands at 18.69%

3. Key Valuation Ratios

When evaluating the financial state of a growing firm like Tencent, we must assess key financial ratios such as Revenue Growth, P/S, P/E, Gross Margin%, Operating Margin%, and Free Cash Flow (FCF).

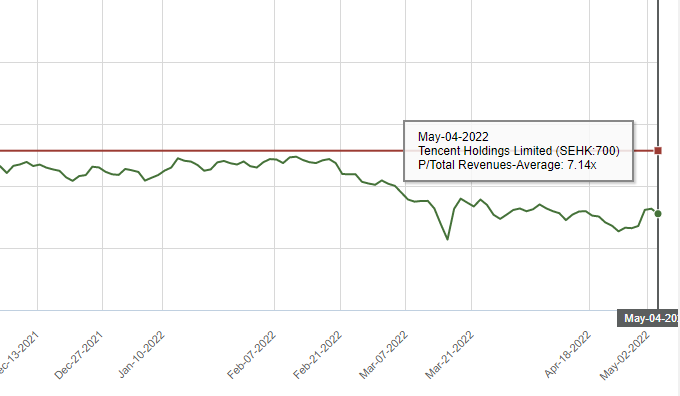

Price/Sales (P/S) ratio (1 Year)

The current P/S Tencent stands at 5.11x while it’s 1-year Avg P/S ratio stands at 7.14x

Price/Sales (P/S) ratio (5 Year)

The current P/S Tencent stands at 5.11x while it’s 5-year Avg P/S ratio stands at 10.30x

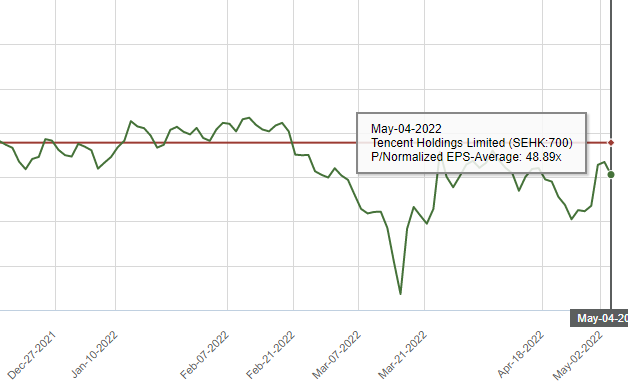

Price/Earnings (P/E) ratio (1 Year)

The current P/E Tencent stands at 45.28x while it’s 1-year Avg P/E ratio stands at 48.89x

Price/Earnings (P/E) ratio (5 Year)

The current P/E Tencent stands at 45.28x while it’s 5-year Avg P/E ratio stands at 61.23x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs, but operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Tencent’s financials, its gross margin has dropped to about 40+%, its operating margin has decreased to about ~30%, and its free cash flow margin has decreased to around 26%. The primary culprits behind Tencent’s margin decline appear to be:

- A ban on Tencent’s ability to monetize two of its key video games

- Increased Financial Regulation related to the company;s digital payments products

| Other Key Ratios | 2017 | 2018 | 2019 | 2020 | 2021 |

| Gross Margin % | 60.1% | 46.2% | 45.3% | 46.7% | 44.5% |

| Operating Margin % | 54.6% | 36.0% | 40.2% | 40.9% | 31.7% |

| FCF% | 48.4% | 29.6% | 34.0% | 33.7% | 26.4% |

Our Stand

Tencent has the world’s largest video game empire, its 1.268 billion user WeChat social media platform is the largest in China. Furthermore, it is also the owner of the largest Chinese video and music streaming platforms. Aside from these, Tencent also has an investment portfolio of RMB878.65 billion, ~USD130 billion which is about 30% of its total market capitalization.

Essentially, Tencent seems to be a mighty combination of Facebook social media and Berkshire Hathaway’s portfolio. With such a wide economic moat, I am certain that Tencent will be able to tide through this short-term headwind. Moreover, China’s rising middle class creates a formidable tailwind, and Tencent’s deliberate approach to monetization has allowed it to keep up consistent strong growth for a sustained period.

At Tencent, the current valuation of P/E – 45.28x, compared to its 1 year and 5 year average of 48.89x and 61.23x. I believe it is relatively undervalued for an industry leader with strong growth in Gaming, Cloud and Short-Form Video. Hence, in my humble opinion, I feel that Tencent stock itself looks attractive on its own today after the sell-off. It remains the best-run company in China in my eyes, which makes it a contender for the best in the world.

You can check out our latest articles here: Busting Myths 3 and Costco Stock Analysis

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.