A company which has adapted and transitioned from the 20th century to the 21st century, is none other than Microsoft. Microsoft was founded in 1975 by Bill Gates and Paul Allen to create PC operating system software at the commencement of the personal computer age. The company’s Windows operating system eventually emerged to dominate the PC market. Microsoft has grown into productivity software, server software, internet services, video games, and PC hardware and accessories over the years.

Today, I am still a user of Windows, Microsoft Office, LinkedIn and Xbox almost daily. These suites of products have already become part of my life to do literally any task.

Current Chief Executive Officer Satya Nadella took the reins of the Redmond, Wash.-based company in 2014 and led Microsoft into cloud computing. Many believed he is the one that saved Microsoft, Satya essentially did a 180-degree turn on Microsoft’s philosophy. He not only embraced open source development but actively started supporting it, so much so that one of Satya’s biggest moves was to acquire Github.

Microsoft is the 3rd largest company by market cap – $1.95 Trillion (as at 15 May 2022). As Microsoft has shown its successful pivot from desktop computing to cloud computing, Microsoft stock has naturally risen as well. However after a recent pullback, many investors may be wondering: Is Microsoft stock a good buy right now?

Overview of Microsoft’s Business

- Key Product & Services under Microsoft

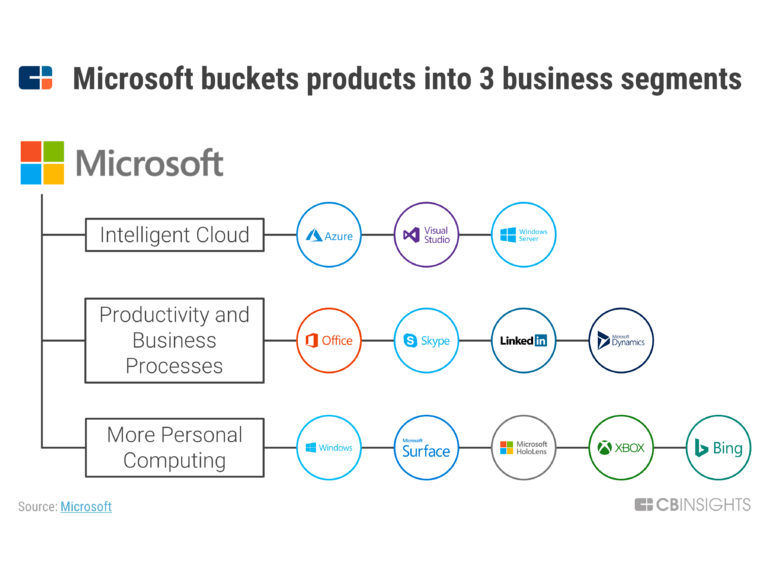

Microsoft segregates its business into the following 3 key segments: Productivity and Business Processes, Intelligent Cloud and More Person Computing.

Qualitative Factors affecting Microsoft

Let’s now take a deeper look into the qualitative aspects that affect the business

Microsoft’s Economic Moat

1. Economies of Scale

Microsoft is able to leverage on the benefits of economies of scale, and then pass those benefits on to their customers. One instance is storage costs. Microsoft have decreased significantly over the last decade as cloud providers are able to purchase large amounts of storage at significant discounts. They are then able to use that storage more significantly and pass on those benefits to end users in the form of lower prices.

2. High Switching Costs

Imaging moving away from Microsoft’s Operating System, Office Suite, and Azure Infrastructure. All of these services have extremely high switching fees, and you may be tied in by utilizing their proprietary APIs or applications offered on their platform. Furthermore, substantial effort and money will be spent. You may also need to re-learn the new software capabilities, which may require more training and effort.

Growth Opportunities for Microsoft

1. Activision Blizzard – Metaverse

Microsoft announced its acquisition of Activision Blizzard for $68.7 million in January 2022. The most significant in the company’s history. This is a stepping stone into the metaverse, according to CEO Satya Nadella. Furthermore, Microsoft can provide the entire metaverse transformation package. They have HoloLens and Virtual Reality devices, as well as platforms (Azure and LinkedIn) and technologies (AI, Graph and Mesh). This suite of products can be applied to the metaverse, which might be a huge growth opportunity if Microsoft is the first to “break the code”.

2. Microsoft Azure Cloud

Microsoft’s cloud business is its biggest source of revenue, accounting for over 38% of the company’s top line in the third quarter of fiscal 2022. This business is enjoying solid growth, as Microsoft reported a 26% year-over-year increase in the segment’s revenue last quarter. Microsoft is in a solid position to take advantage of the growing global cloud infrastructure market. As the second-largest public cloud service provider, Microsoft has shown signs of starting to eat into market leader Amazon’s share. Hence, Microsoft looks poised to benefit from this big growth opportunity.

Business Risks for Microsoft

Competition – Microsoft 365 Office, Azure Cloud and Xbox Gaming

1. Microsoft 365 Office

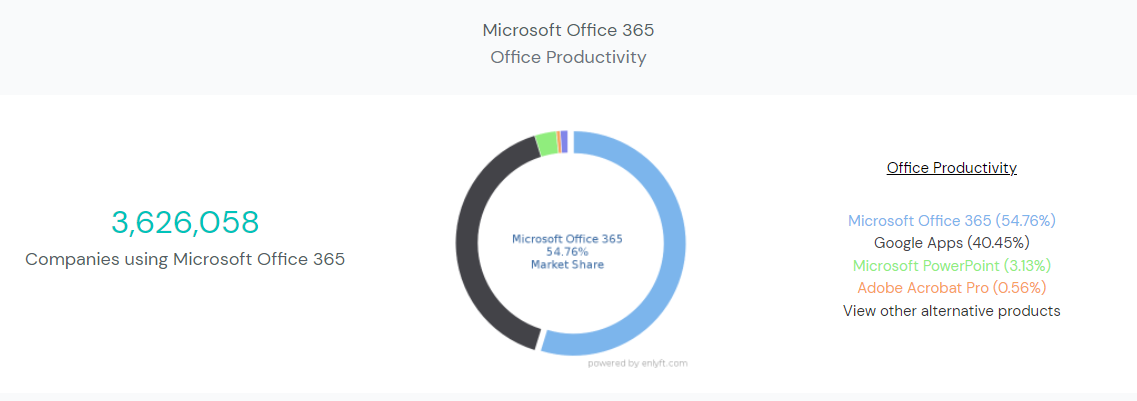

Office biggest competitor – Google Suite (40.45% market share). Ever since Google has made an impression in the Office Productivity market, it has been steadily growing market share. Companies that are smaller in size would rather use Google Suite due to their cheaper costs and seamless collaboration. If this continues, this could be detrimental to Microsoft Office subscription service.

2. Azure Cloud

Microsoft Azure Cloud faces diverse competition from companies such as Amazon, Google, IBM, Oracle, VMware and Alibaba. Although Microsoft is currently the #2 cloud service providers in the world, there are many companies looking into this industry due to the high margin business. This could potentially take up Azure’s market share in the future.

3. Xbox Gaming

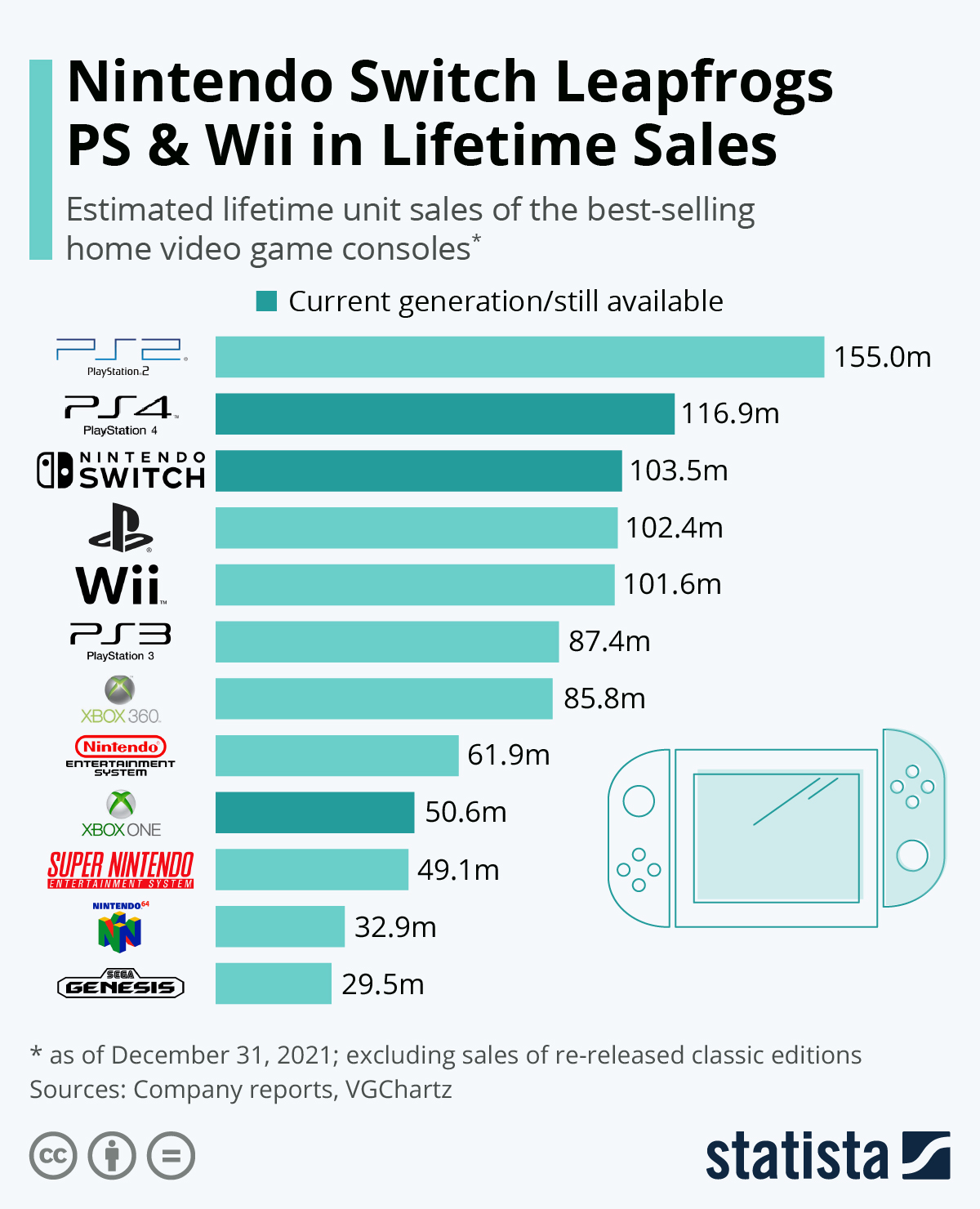

Microsoft Sony’s Playstation and Nintendo’s Switch/Wii compete fiercely with Xbox. With the most recent addition of video game consoles, Sony’s Playstation 5 and Microsoft’s Xbox Series X remain infamously difficult to locate more than 14 months after their respective November 2020 releases. Nintendo’s Switch has been selling like hotcakes over the last 21 months, with almost 48 million devices sold. Today, Xbox ranks third in the console gaming market. To acquire market share from Sony or Nintendo, Xbox must release a really groundbreaking device that changes the whole video gaming console landscape. A recent article published by Nintnedo showed its market presence – selling over 107 million Switch units!

Quantitative Factors affecting Microsoft

Let’s now take a deeper look into the quantitative aspects that affect the business

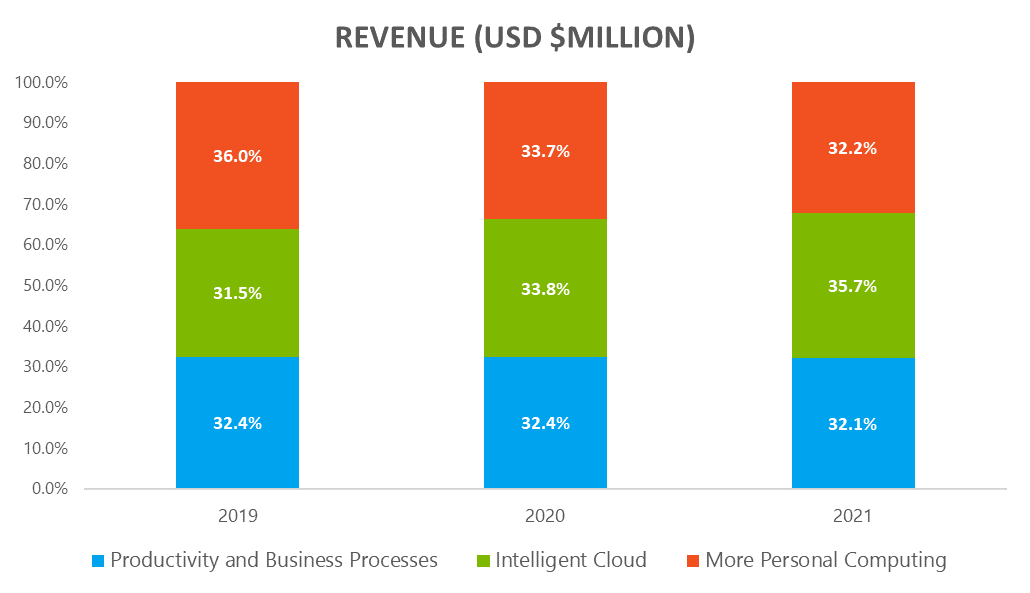

1. Financial Highlights (Revenue Breakdown)

The majority of Microsoft’s revenue in 2021 and LTM still predominantly comes from their Intelligent Cloud business at ~35%. Its cloud computing business has grown over the last 3 years from the lowest contributing segment to the highest. Productivity and Business Processes and More Personal Computing also contribute fairly of 32% each.

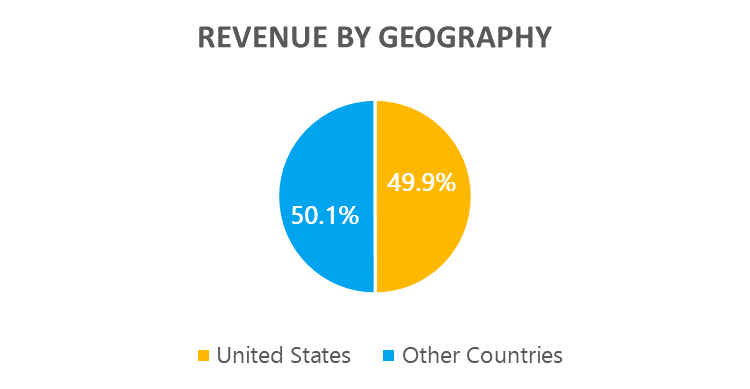

Microsoft back in 2019 had 51% of its revenue from the United States and 49% from Other Countries. In 2021, revenue from Other Countries came in more than the United States by a small margin of 49.9% to 50.1% respectively.

2. Key Valuation Ratios

When evaluating the financial state of a growing firm like Microsoft, we must assess key financial ratios such as Revenue Growth, P/S, P/E, Gross Margin%, Operating Margin%, and FCF.

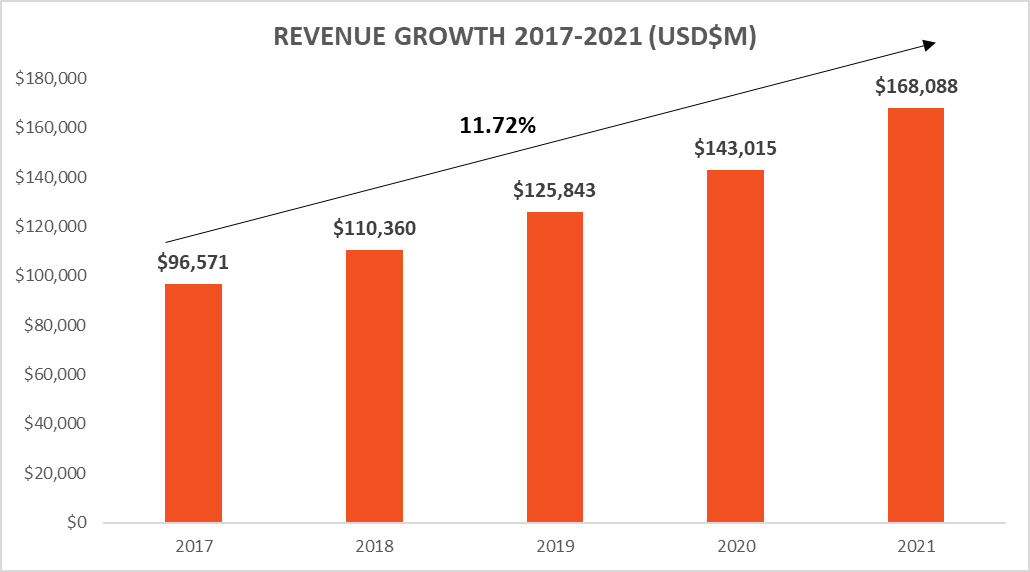

Revenue Growth (5 Year)

Microsoft’s FY2021 revenue is at USD$168.08B with 17.53% (YoY growth) and 5-Year CAGR stands at 11.72%

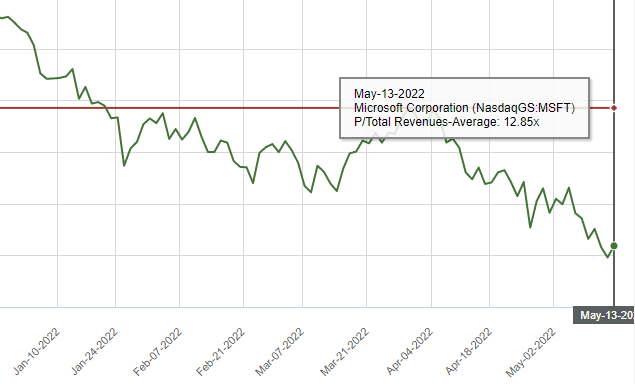

Price/Sales (P/S) ratio (1 Year)

The current P/S Microsoft stands at 10.18x while it’s 1-year Avg P/S ratio stands at 12.85x

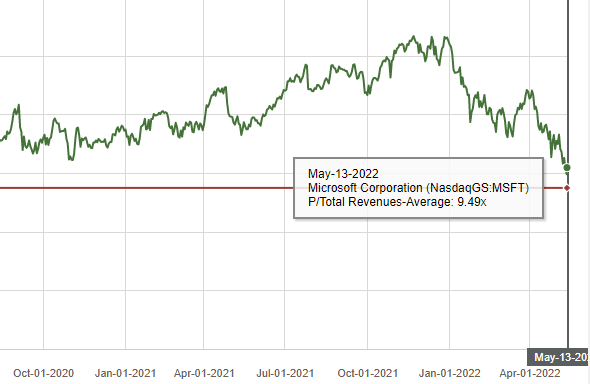

Price/Sales (P/S) ratio (5 Year)

The current P/S Microsoft stands at 10.18x while it’s 5-year Avg P/S ratio stands at 9.49x

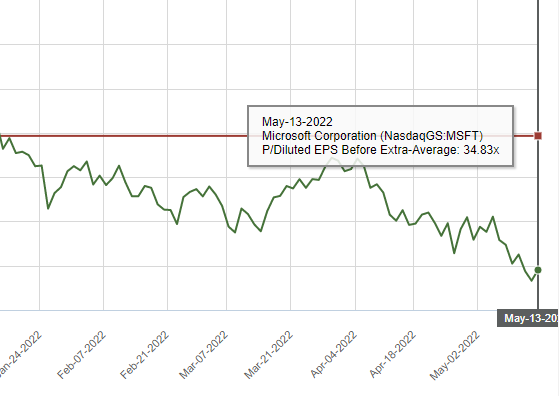

Price/Earnings (P/E) ratio (1 Year)

The current P/E Microsoft stands at 27.26x while it’s 1-year Avg P/E ratio stands at 34.83x

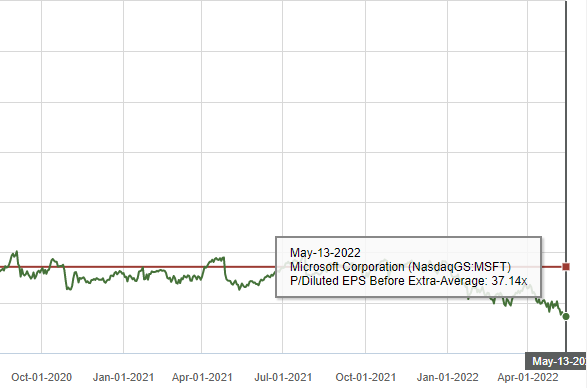

Price/Earnings (P/E) ratio (5 Year)

The current P/E Microsoft stands at 27.26x while it’s 5-year Avg P/E ratio stands at 37.14x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs, but operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Microsoft’s financials, its gross margin has remained relatively stable, as it increases steadily to ~69%. Its operating margin has also increased steadily from 37% back in 2013 to 45% in FY21. Its free cash flow margin has also increased steadily to 33%. The primary growth in margins behind Microsoft’s margin increase appear to be:

- Focusing on more lucrative segments of the business – Azure Cloud, while maintaining steady growth in the legacy business – Office 365.

- Expanding their Competitive Edge – Increasing their Capital Expenditure and Making Acquisitions

| Other Key Ratios | 2017 | 2018 | 2019 | 2020 | 2021 |

| Gross Margin % | 64.5% | 65.2% | 65.9% | 67.8% | 68.9% |

| Operating Margin % | 40.9% | 39.8% | 41.5% | 42.4% | 45.7% |

| FCF% | 32.5% | 29.2% | 30.4% | 31.6% | 33.4% |

Our Stand

Microsoft is a fantastic company with one of the strongest moats around. The various business areas benefit from switching costs, network effects, and, of course, Microsoft’s brand recognition adds to its competitive edge. Furthermore, Microsoft has a robust balance sheet and will very certainly continue to expand at a good rate.

Although Microsoft is a fundamentally excellent company and can fairly defend itself from current tech sector problems and supply chain disruptions, the value of the company’s stock may just be fairly valued after the recent market correction. Hence, I might wait for a better price before executing my first tranche into Microsoft.

You can check out our latest articles here: How to prepare your portfolio in Times of Recession and Rule of 72 Principle

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.