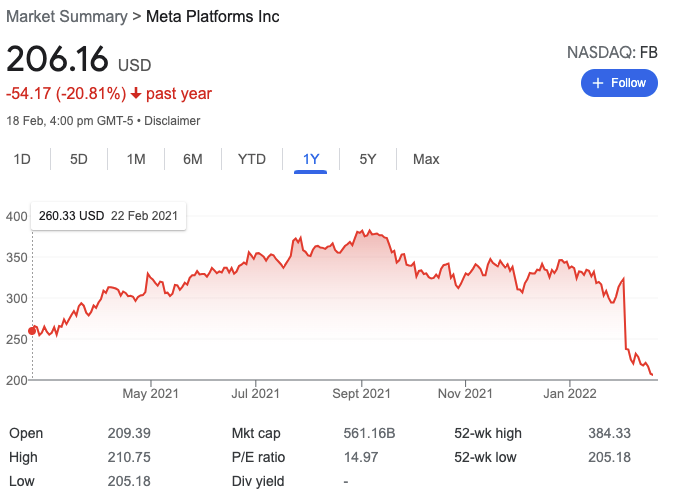

Meta (previously Facebook) has been swarmed with a slew of security and growth challenges. With the recent Apple and Google’s new privacy changes and the lowered growth outlook, this has resulted in significant beating to Meta stock. As a result, Meta’s share price has dropped more than 21% and is trading near its 52-week low. In this article, we will look to analysis Meta stock and determine its true valuation. Are investors currently mispricing Meta share price or should one avoid the value-trap that Meta stock is presenting?

Overview of Meta’s Business

Meta was created in 2004 as an online social network (FaceMash) within Harvard University by four Harvard students. One of its most renowned co-founders is Mark Zuckerberg, who is currently the company’s current CEO. Since then, Meta has grew significantly and now also own other applications like Instagram, Whatsapp, and Messenger. As of December 2021, Meta still dominates the social network space with over 7.5 billion Monthly Active Users (MAUs). Tencent’s WeChat, Qzone, and QQ are presently in second.

Meta Key Product & Services

Meta’s products and services are currently divided into two categories: Family of Apps (FoA) and Reality Labs (RL). FoA signifies their main social networking apps and business. While RL encompasses all future growth projects that will reshape the company future.

Operating Model

Meta makes the majority of their revenue via FoA (Facebook, Instagram, Messenger) by selling advertising slots to marketers. Advertisements on the platforms allow marketers to target users based on demographics, geographic and behaviours. On the other hand, RL generates revenue mainly from the sales of consumer hardware and software products.

Qualitative Factors for Meta

Let’s now look at the qualitative aspects that affects their business.

Economic Moat

- Network Effect

Meta’s network effect has always been its moat. It has been able to limit competition over the last decade by buying and duplicating competitors. The collapse of Google+ is one example of Facebook’s network effect. Google+ was an attempt by Google to compete with Facebook. However, Google’s de-emphasis of Google+ on its platforms from 2015 indicates that Google+ was unable to gain traction. Below are some past acquisitions made by Meta to strengthen its network effect.

Acquisitions has grew increasingly harder in the current day and age. Hence, it is critical for Meta to explore new growth possibilities to expand the business.

Growth Opportunities

- New Operating system (Eye OS)

Meta doesn’t want their new gears (Oculus Rift) to be heavily dependent on Google/Apple’s operating systems. With this in mind, the business tasked Mark Luckovsky with creating a new operating system Eye OS from scratch. They intend to develop an ecosystem of VR/AR gear and applications with this new Operating System.

- Metaverse

Meta’s Metaverse business isn’t centered on selling high-end hardware, but rather on making VR devices accessible to everyone. This is because the Metaverse market estimated to reach $800 billion by 2026. Hence, their plan is to lower the barrier to entry for new customers while increasing the size of the Metaverse’s economy. Eventually, Meta will focus primarily on advertising and digital commerce. This may be similar to games like Minecraft, which earn from every transactions made in the game.

Business Risks

- Risk Related to Product Offerings

Multiple factors have influenced Meta’s user growth and engagement. Strong competition from players like ByteDance have reduced users’ involvement with their products and services. This decrease in user growth and engagement may result in the loss of marketers and investment. This might be harmful to the company as advertising accounts for majority of their revenue. Hence, Meta has been on a lookout for new means of engaging and growing their user base.

- Risk related to Govt Regulations

Some governments has threatened to impose restrictions on Meta’s content and products in their countries. For example, the USA have complex international laws on privacy and data usage. However, many of these regulations are subject to interpretation by business which may result in monetary penalties. As a result, Meta has been cooperating very closely with authorities in the regions that they operate in.

Quantitative Factors for Meta

Let’s now take a deeper look into the quantitative aspects that affect the business.

Financial Highlights (Revenue Breakdown)

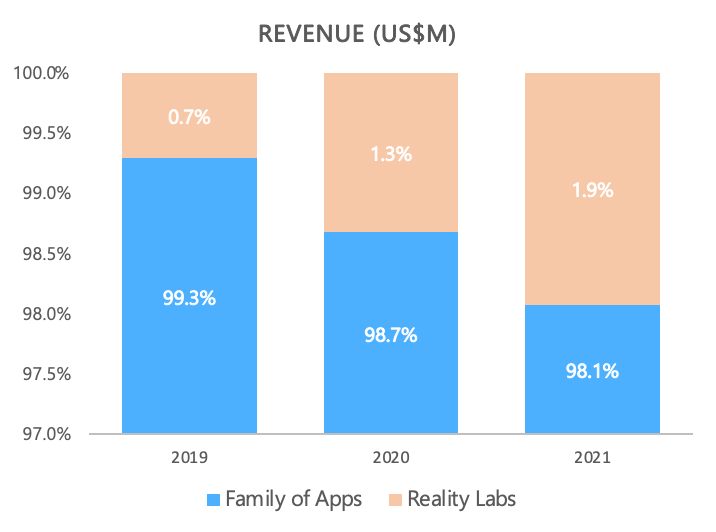

The majority of Meta’s revenue in 2021 still predominantly comes from their Family of Apps (Facebook, Instagram, WhatsApp, and Messenger). Reality Labs currently only accounts for 1.9 percent of their total revenue.

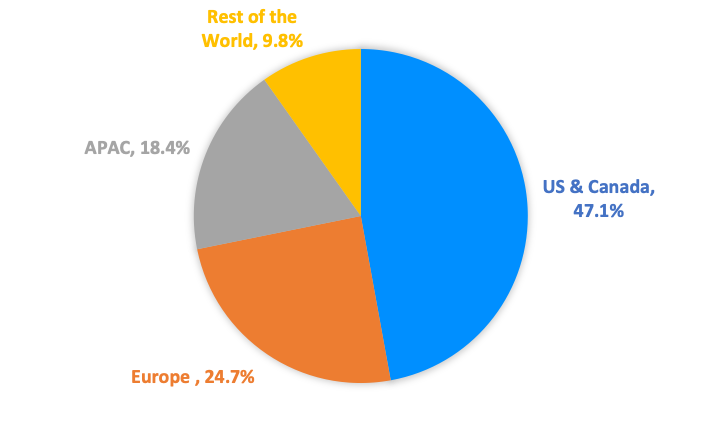

The current advertising landscape in USA and Europe are more mature as compared to other regions. Hence, Meta’s revenue in regions like the United States, Canada and Europe are considerably larger. The Average Revenue Per User (ARPU) in the United States and Canada was more than 12 times higher in 2021 than in the APAC. This explains why more than 72% of Meta’s revenue comes from the western countries.

Key Valuation Ratios

When evaluating the financial state of a growing firm like Meta, key ratios comes in handy. (P/S, P/E, Gross Margin%, Operating Margin% )

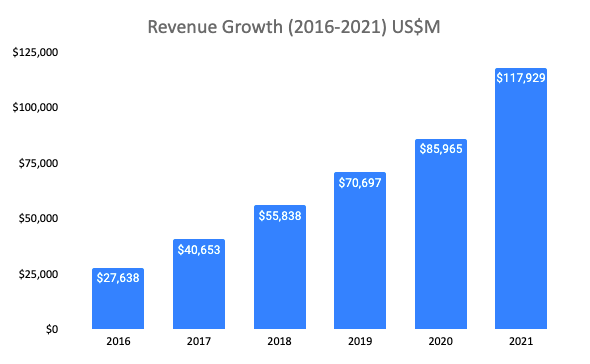

Revenue Growth (5 Year)

The Meta’s 2021 revenue stands at $117B with 37.2% (YoY growth) and 5-Year CAGR stands at 33.7%

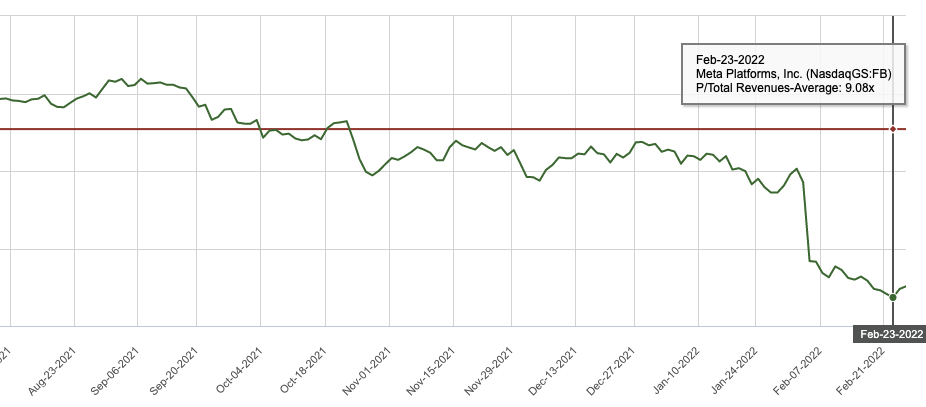

Price/Sales (P/S) ratio (1 Year)

The current P/S Meta stands at 5.02x while it’s 1-year Avg P/S ratio stands at 9.08x

Price/Sales (P/S) ratio (5 Year)

The current P/S Meta stands at 5.02x while it’s 5-year Avg P/S ratio stands at 10.36x

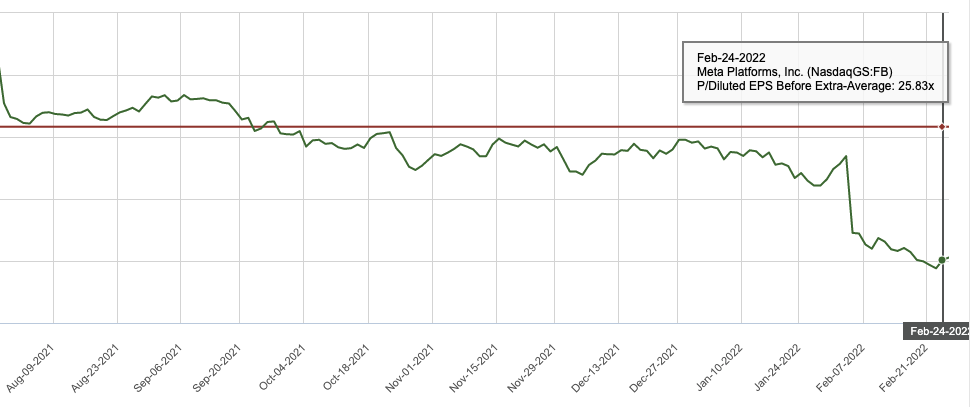

Price/Earnings (P/E) ratio (1 Year)

The current P/E Meta stands at 15.29x while it’s 1-year Avg P/E ratio stands at 25.83x

Price/Earnings (P/E) ratio (5 Year)

The current P/E Meta stands at 15.29x while it’s 5-year Avg P/E ratio stands at 30.06x

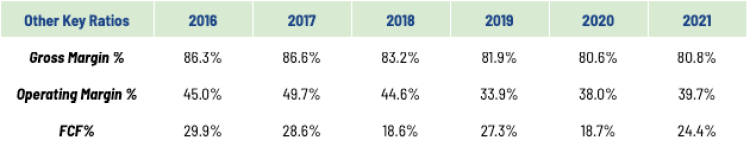

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs. Operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Meta’s financials, its gross margin has been lingering around 80%. Its operating margin has been around 35-40% and its free cash flow margin has been hovering around 20%. As a rule of thumb, business are considered good if they have an operating margin of more than 15%. As a result, this clearly demonstrates that Meta has been doing well financially.

Our Stand

Meta and its products, such as Facebook and Instagram, have become synonymous with “Social Media Apps” today. Meta’s P/E ratio is 15.3 at a stock price of US$210 as of 25 February 2022. This is relatively undervalued and attractive price for an industry leader with space to grow. By 2026, the global market for social networking platforms is predicted to increase at a CAGR of 25.4 percent to reach US$939.7 billion. Despite competition, Meta possesses the first-mover advantage and ecosystem to remain a key player alongside Google and ByteDance.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.