Investment, investment, investment… In today’s millennial dialogue, it has became increasingly popular.

As many of my friends have dabbled into investing, I’ve often pondered if they really know what they’re in for or if it’s just a case of FOMO.

These are my thoughts on the questions YOU should ask yourself before embarking on your investment adventure.

Key Investing Questions #1. Well-insured and and Safety Net

Term/Whole Life Insurance and Health Insurance (Hospitalisation Plan/Integrated Shield Plans) are essential to obtain for many people. These two insurances are vital once you enter the workforce since they will be necessary for our future. The question of how much to insure will be a good topic for another day. Instead, why do you need to be insured, you might wonder? Insurance, in my opinion, is Life’s GOALKEEPER – the last line of defense. In the event that all goes wrong, insurance will cover our financial losses.

Next, is your safety net ready?

When determining whether or not I have a ready safety net, I consider 1 key indicator. They are as follows:

- Basic Liquidity Ratio – Cash/Monthly Expenses > 6

NOTE: In case you are wondering, HIGH INTEREST DEBT (Credit Card Debt and Student Loan Debt) should be cleared before you start investing.

While having a Basic Liquidity Ratio of roughly 6 months is a good idea in case of an emergency or unanticipated circumstances that we may not have anticipated. Of course, these aren’t actual figures which you may want to follow, rather, they’re a suggestion to what you may want to work towards.

Key Investing Questions #2. Investment Goal

Having an investment goal is crucial as you will have a goal to work towards. On the road to FIRE, one of the milestones among FIRE followers is to build a net worth of S$100,000 by the age of 30.

This will be a good moment for you to analyze your personal cash flow to project how you can attain your investment objective in order to better project how feasible you will reach your investment target.

An example is as follows:

- Assume you graduate at 25, 5 years to age 30.

- Monthly Income of $4,000, Monthly Expenses of $1,700 and Monthly Cashflow of $2,300

By Age 30 – $27,600 * 5 years = $138,000 (with 0% interest!)

By Age 30 – $27,500 * 5 years = $174,871.64 (8% interest compounded)

As everyone’s circumstances are unique, this is by no means a definitive list of what one should strive towards. Instead, this can be a starting point for you to become financially independent!

Key Investing Questions #3. What is my risk appetite and investment time frame?

First, to determine your risk appetite, I have broken down into 3 risk profiles:

- Low Risk – Investors whom are concern about their capital, favor high-quality firms that offer consistent returns and moderate capital growth. These investors may want to consider investing in dividend stocks such as Singapore Banks and REITs. As such stocks, will pay them passively – Dividends.

- Medium Risk – Investors whom are willing to accept a little volatility in the value of their portfolio which may produce larger returns. This portfolio could concentrate on Exchange Traded Funds (ETFs) such as the S&P 500 or NASDAQ 100 Index, which have an excellent and consistent track record of yearly returns of above 8%.

- High Risk – For the purpose of capital gain, these investors are willing to expose their portfolio to increased risk and volatility. Investors are ready to risk not just their money in unpredictable financial markets, but also in growth companies with an unproven track record. They may also be considering cryptocurrencies as a way to diversify their holdings. This is not for the faint of heart, and it is certainly not for those with restricted funds.

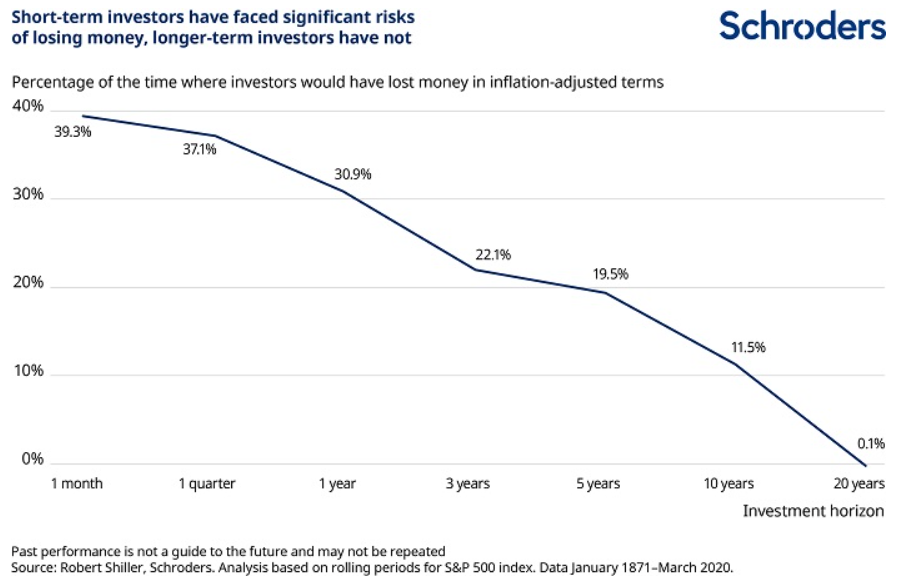

According to a study conducted by Schroders, the longer your investing horizon is, the lower your chances of losing money become. Short-term investors have an astounding 40% chance of losing money. Thus, if you invest for 20 years, your odds of losing money is greatly lowered to 0.1%.

As a result, it is critical to comprehend your investing time period. The longer an investor’s time horizon, the more aggressive (or riskier) a portfolio can be built. The investor’s portfolio should be more conservative, or less risky, the shorter the time horizon.

#4. What is my investment knowledge today?

It’s natural to feel hesitant about which investments to make, especially when you’re initially starting out. Nobody is born knowing everything there is to know about anything.

Be honest with yourself. If your expertise is minimal, investing in your circle of competency is an excellent place to start. For example, if you work in the technology field, your comprehension of how the industry works will be greater based on your experience than someone who researches and attempts to learn about it online. As a result, you’ll be more likely to make smarter judgments since you’ll be aware of cutting-edge technology as well as the competitive benefits and limits of each product.

As a result, if you want to learn how to invest, I recommend starting small. It’s pointless to invest a huge quantity of money if you’re not sure about the investments you’re making. Before investing, you may want to have an investment thesis before you invest, and you should check it on a regular basis to see whether it is still relevant.

Conclusion – To beat inflation

Money may be perceived as a taboo subject, one that even parents may be hesitant to discuss with their children. As money is hard earned, it should always be invested carefully, safely, and prudently. Let us not forget that the primary reason people begin investing is to fight inflation, and risks must always be managed.

If you are keen, check out our articles on other analysis: Trust Bank Referral.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.