By restructuring into a new parent company, Alphabet was able to diversify beyond Google’s main search business. Some of its new big bets includes the likes of YouTube, FitBit, Kaggle, DeepMind and Looker. Recently, Alphabet announced a 20-for-1 forward stock split for mid-July, reducing the share price down to US$140. Let’s first take a closer look into its business and financials to better assess Alphabet’s share price.

Overview of Alphabet’s Business

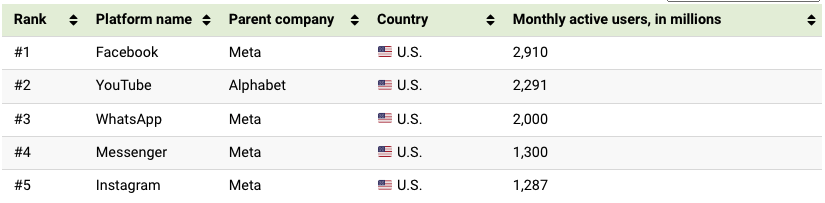

Google began as Backrub in 1995, a search engine created by two Stanford students Larry Page and Sergey Brin. The company’s constant pursuit for better solutions remains at the heart of all they do. From YouTube to Google Search, Google has produced products that are used by billions of across the world. Google Search still dominates the Search Engines software with over 92 percent market share worldwide as of January 2022. Its nearest competitor, Bing, comes in second with only 2.9 percent. Furthermore, YouTube has grown dramatically to become the second most popular social media site, with over 2.3 billion MAUs.

Alphabet’s Key Product & Services

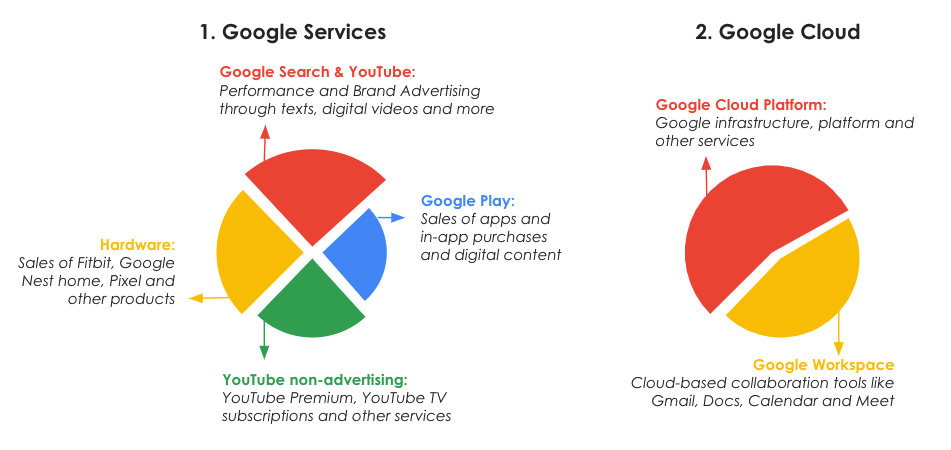

Alphabet is a conglomerate of companies, the most well-known of which is Google. For their business, it is broken down into three segments: Google Services and Google Cloud and Other Bets. Other Bets are early-stage innovations that aren’t related to Alphabets primary business. Alphabet take a long-term approach towards their “Other Bets” portfolio in hopes of generating long-term gains.

Alphabet’s Operating Model

Alphabet’s two primary business sectors, Google Services and Google Cloud, each have vastly different income model. Google Services’ revenues are divided into two categories: advertising and non-advertising. Performance and brand advertising that occurs on Google Search and YouTube are included under Advertising. Revenues from Google Play and hardware products falls under the non-advertising revenues. Google Cloud, on the other hand, generates revenue by providing infrastructure for developers and software for Enterprises. Some of their cloud-based collaboration products includes Gmail, Docs, Drive, Calendar, and Meet.

Qualitative Factors for Alphabet

Let’s now look at the qualitative aspects that affect Alphabet’s existing business.

Economic Moat

1. Data Vaults

Most businesses want to capitalise on their data but failed as not all data have the same value. However, Alphabet is in a strong position. It is able to leverage on their Search data which is used in high-demand services. Their first-mover advantage in Search data has grown into such a robust data moat. As of Jan 2022, Google Search still has over 92 percent market dominance in search. Over time, Alphabet has uncovered and built up new data sets with Maps, YouTube and Google Assistant.

Growth Opportunities

1. Artificial Intelligence and Machine Learning

A significant amount of R&D has been placed by Alphabet into developing new AI methods and algorithms. This technology has been embedded into their core products like Google Search, YouTube, Maps, and Smart devices. Firstly, Alphabet’s new search algorithm, the Multitask Unified Model (MUM) was introduced in 2021. This new algorithm enables Google Search to be 1000 times more powerful and efficient. Furthermore, it also excels in handling a wide range of media formats, complicated search queries and language barriers.

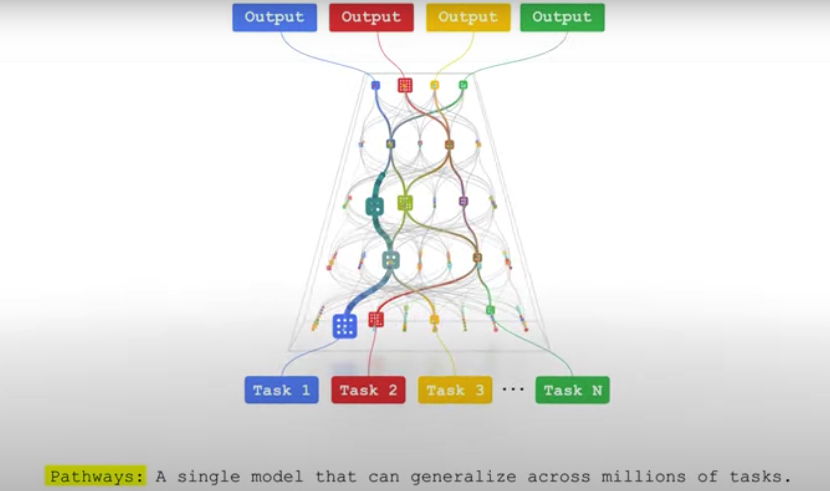

Secondly, Pathways is Alphabet’s breakthrough in AI architecture that can manage multiple activities and quickly learn new tasks. With Pathways, Google is taking the first few steps to building an Artificial General Intelligence system. If Alphabet is able to successfully build out a capable AGI, this will be a new revenue streams for Google to leverage on.

2. Google Cloud Platform (GCP)

Alphabet has a number of growth opportunities in the coming years and GCP is one of them. This revenue sector increased by more than 47% YoY to over $19B. GCP is currently ranked third among big cloud providers such as Amazon (AWS) and Microsoft (Azure). The global cloud computing industry is predicted to increase at a 16.3% CAGR to USD 947.3 billion in 2026. Hence, Google Cloud is well positioned to maintain its strong growth and revenue.

3. YouTube

YouTube is another high-growth segment as it is already one of the most popular video platforms in the world. In 2021, YouTube averaged $12.54 in revenue for each MAU while Facebook is averaging about $15.60. This shows that there is still room for YouTube to increase its revenue. In addition, YouTube has been generating cash from a variety of sources. YouTube Premium and YouTube TV are two examples of this. These are two services that require a constant subscription by users. The effort to diversify revenue sources is critical for YouTube and Alphabet’s long-term success.

Business Risks

1. Risk Related to Company

In 2021, the display of adverts online accounted for more than 80% of Alphabet’s total revenue. Any significant changes to advertising policies or macroeconomic conditions, such as Covid-19 could impact the firm. Hence, Alphabet has to always be prepared for any drastic changes to such matters.

2. Risk Related to Industry

Alphabet’s suite of products and services typically involve the storage and transmission of sensitive information. Software bugs and vulnerabilities in their goods and services place them at risk of losing or misusing information. This might lead to litigations, regulatory fines and reputational damages. Over the years, cyber attacks have definitely become more sophisticated and widespread. An example would be industry-wide vulnerabilities, such as the Log4j vulnerability revealed in December 2021.

3. Risk related to Govt Regulations

Many technology giants have been facing increased regulatory scrutiny and enforcement action. Alphabet has received a couple of antitrust complaints alleging that the company has violated the antitrust laws. As a result, Alphabet may have to change their products and services to meet and fulfil the different countries’ regulations. However, this may limit Alphabet’s ability to pursue certain business models or products. If they fail to do so, this may result in substantial penalties which may affect the financial condition.

Quantitative Factors for Alphabet

Let’s now look at the quantitative aspects that affect the current business.

- Financial Highlights (Revenue Breakdown)

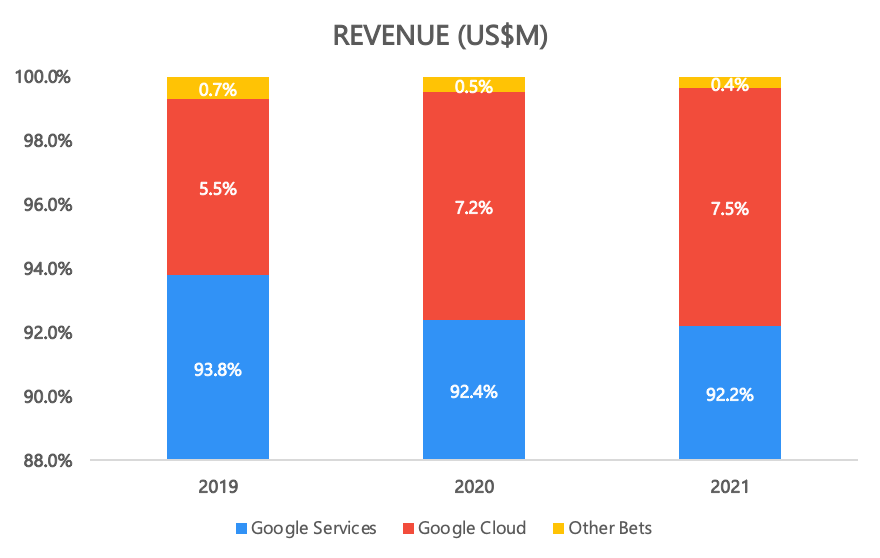

The majority of Alphabet’s revenue in 2021 still predominantly comes from their Google Services. Google Cloud accounts for 7.5% of their annual revenue and Other Bets takes the remaining 0.4%. Till date, Alphabet’s bets are still contributing less than 1% to their annual revenue.

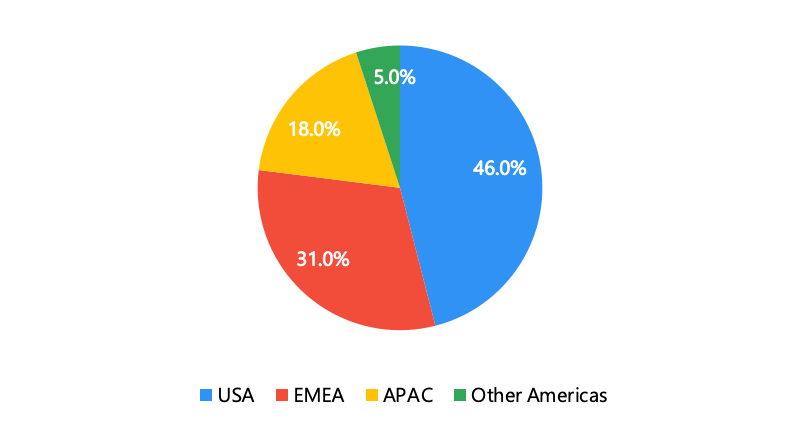

The current advertising landscape in USA and EMEA are more mature as compared to other regions. Hence, Alphabet’s revenue in regions like the USA and EMEA are considerably larger. This explains why ~77% of Alphabet’s revenue comes from the US and EMEA regions.

- Key Valuation Ratios

When evaluating the financial state of a growing firm like Alphabet, key ratios comes in handy. (P/S, P/E, Gross Margin%, Operating Margin% )

Revenue Growth (5 Year)

Alphabet’s 2021 revenue stands at $257B with 41.2% (YoY growth) and 5-Year CAGR stands at 23.3%

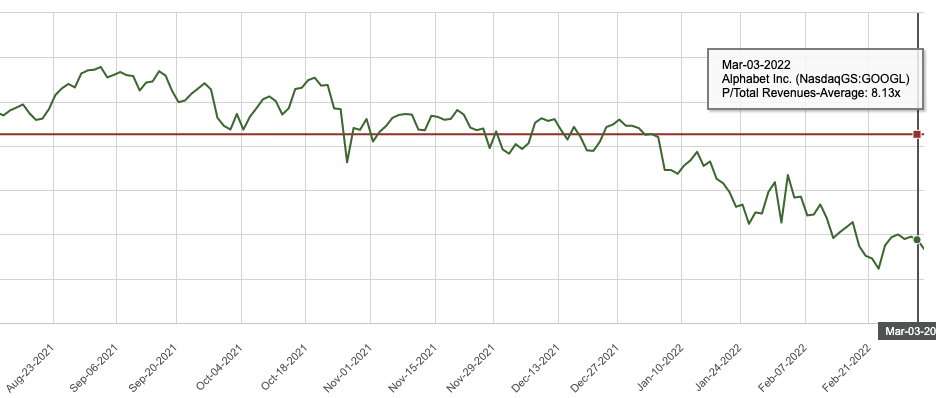

Price/Sales (P/S) ratio (1 Year)

The current P/S Alphabet stands at 6.84x while it’s 1-year Avg P/S ratio stands at 8.13x

Price/Sales (P/S) ratio (5 Year)

The current P/S Alphabet stands at 6.84x while it’s 5-year Avg P/S ratio stands at 6.71x

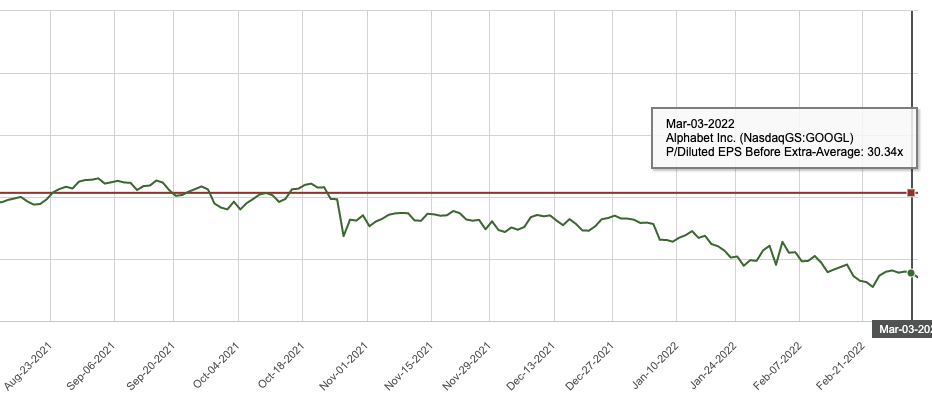

Price/Earnings (P/E) ratio (1 Year)

The current P/E Alphabet stands at 23.51x while it’s 1-year Avg P/E ratio stands at 30.34x

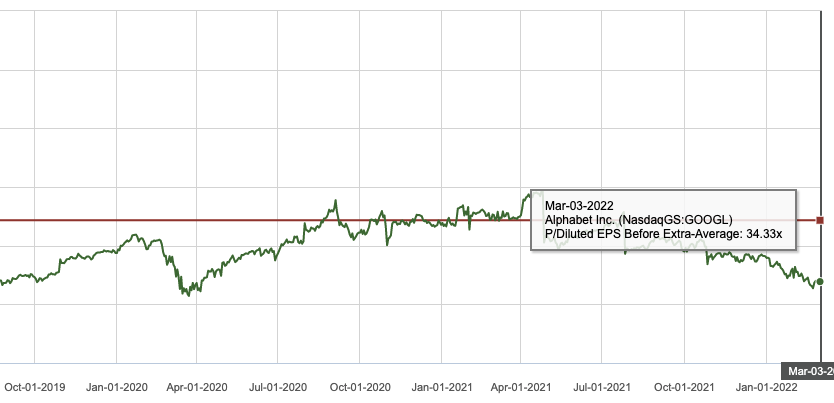

Price/Earnings (P/E) ratio (5 Year)

The current P/E Alphabet stands at 23.51x while it’s 5-year Avg P/E ratio stands at 34.33x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs, but operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Looking at Alphabet’s financials, its gross margin has been lingering around 50+%, its operating margin has been sitting around 22-30%, and its free cash flow margin has been hovering around 20%. An operating margin of more than 15% is regarded as good in most businesses as a rule of thumb. As a result, this clearly demonstrates that Alphabet has been doing well financially.

Our Stand

Alphabet and its products have become synonymous with “Social Media Advertising and Apps” today as the industry’s leaders. Alphabet’s P/E ratio is 23.51 at a stock price of US$2633 which is relatively fairly valued for an industry leader with space to grow. By 2026, the social networking platforms market is predicted to increase at 25.4 percent CAGR, reaching US$939.7 billion. Furthermore, the global cloud computing industry is predicted to increase to USD 947.3 billion in 2026. Lastly, with these strong growth in industries, Alphabet is poised to continue growing and be a key player for the foreseeable future.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.