Parkway Life REIT, one of Singapore’s most resilient and defensive REIT in Singapore?

Let’s check it out!

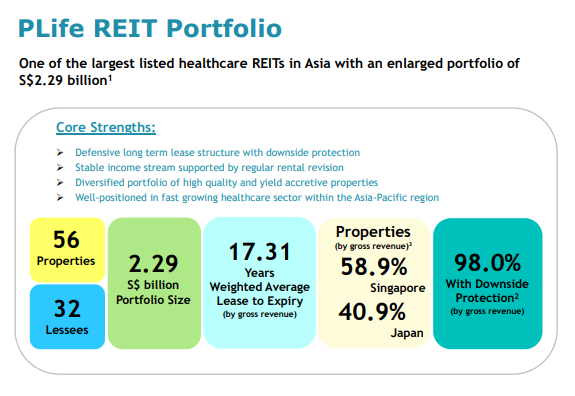

Parkway Life REIT (“PLife REIT”) is Asia’s largest listed healthcare REIT. It invests in income-producing real estate and real estate-related assets, used primarily for healthcare and/or healthcare-related purposes. As at 31 December 2021, PLife REIT’s total portfolio size stands at 56 properties totaling approximately S$2.29 billion.

Overview of Parkway Life REIT

Key highlights of Parkway Life REIT Portfolio:

- 56 Properties and 32 Lesses

- Portfolio Size: S$2.29 billion

- 17.31 Weighted Years Average Lease To Expiry (by Gross Revenue)

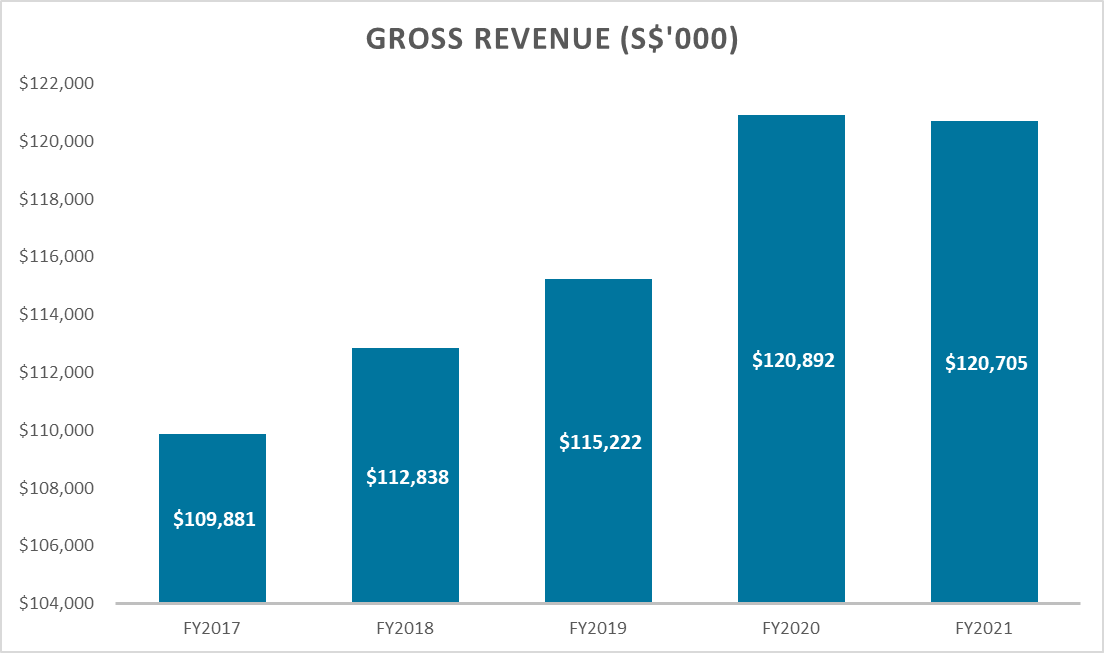

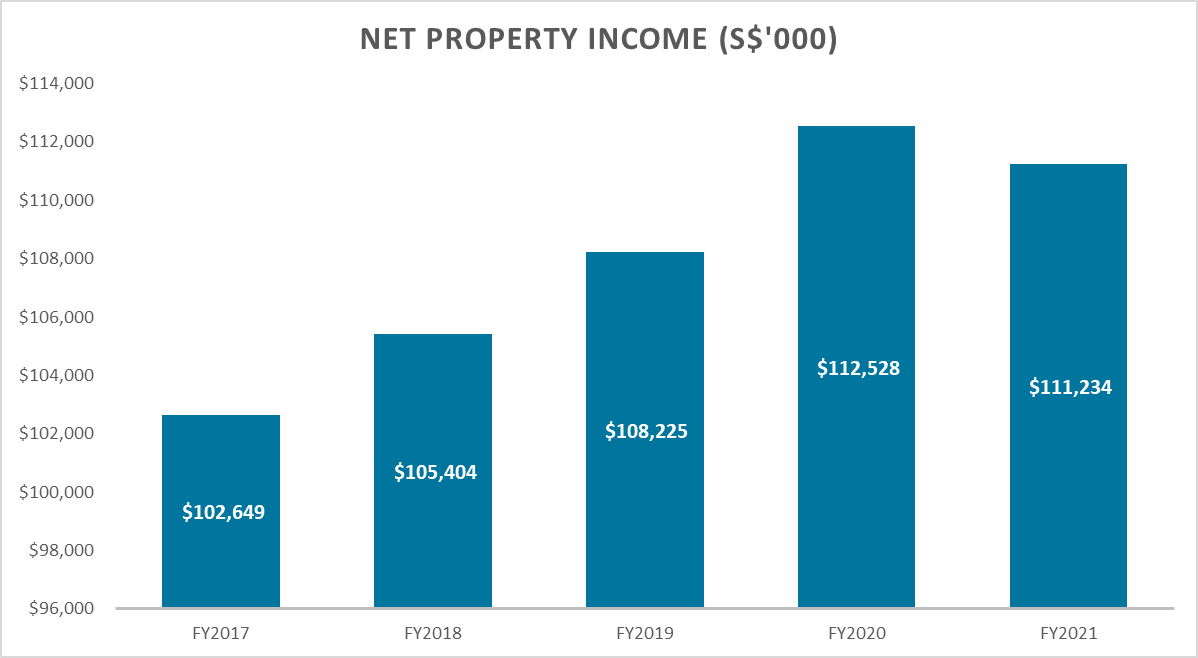

Parkway Life REIT: Gross Revenue and Net Property Income

Gross Revenue for FY21 fell slightly to S$120.71 million from FY20 S$120.89 million. The Compound Annual Growth Rate (CAGR) of PLife’s Gross Revenue over 5 years amounted to 2.38%. Gross Revenue by geography from its properties are 58.9% in Singapore and 40.9% in Japan as at FY21.

Net Property Income (NPI) for FY21 fell slightly to S$111.23 million from FY20 S$112.53 million. Both decline in Gross Revenue and Net Property Income (NPI) for FY21 was largely attributable to the divestment of P-Life Matsudo property in Japan and the depreciation of Japanese yen. The Compound Annual Growth Rate (CAGR) of PLife’s NPI over 5 years amounted to 2.03%.

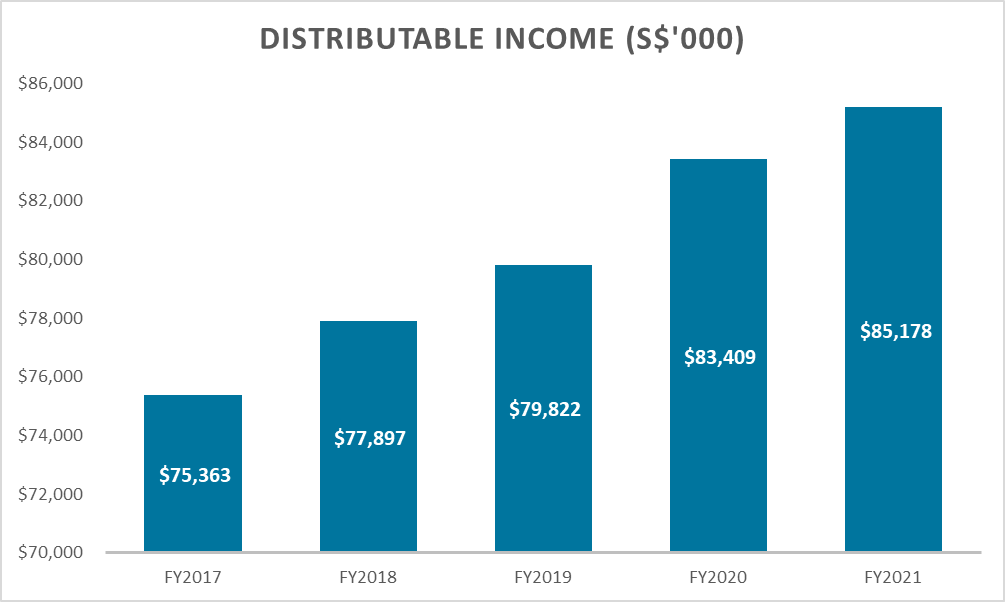

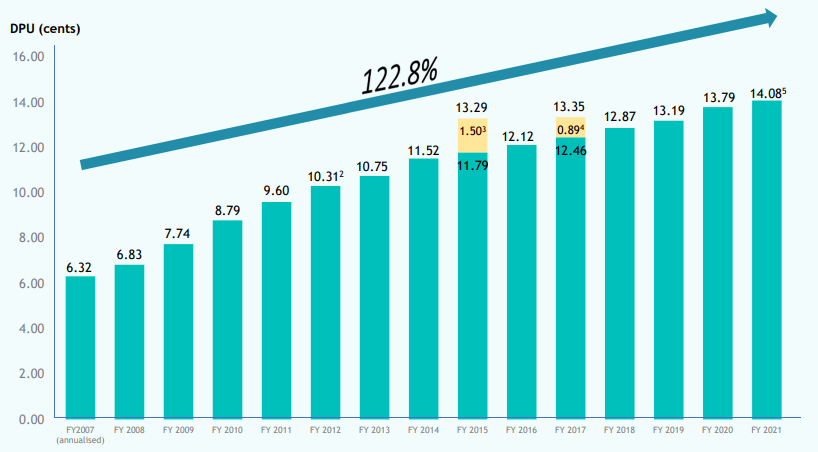

Parkway Life REIT: Distributable Income & Distribution Per Unit

Distributable Income for FY21 increased slightly to S$85.18 million from FY20 S$83.41 million. The Compound Annual Growth Rate (CAGR) of PLife’s Distributable Income over 5 years amounted to 3.11%.

PLife REIT’s Distribution Per Unit (DPU) has climbed by a remarkable 122.8% since its inception in FY2007. Its steady DPU shown that, despite the Global Financial Crisis in 2008 and the Coronavirus collapse in 2020, it will be able to weather market ups and downs.

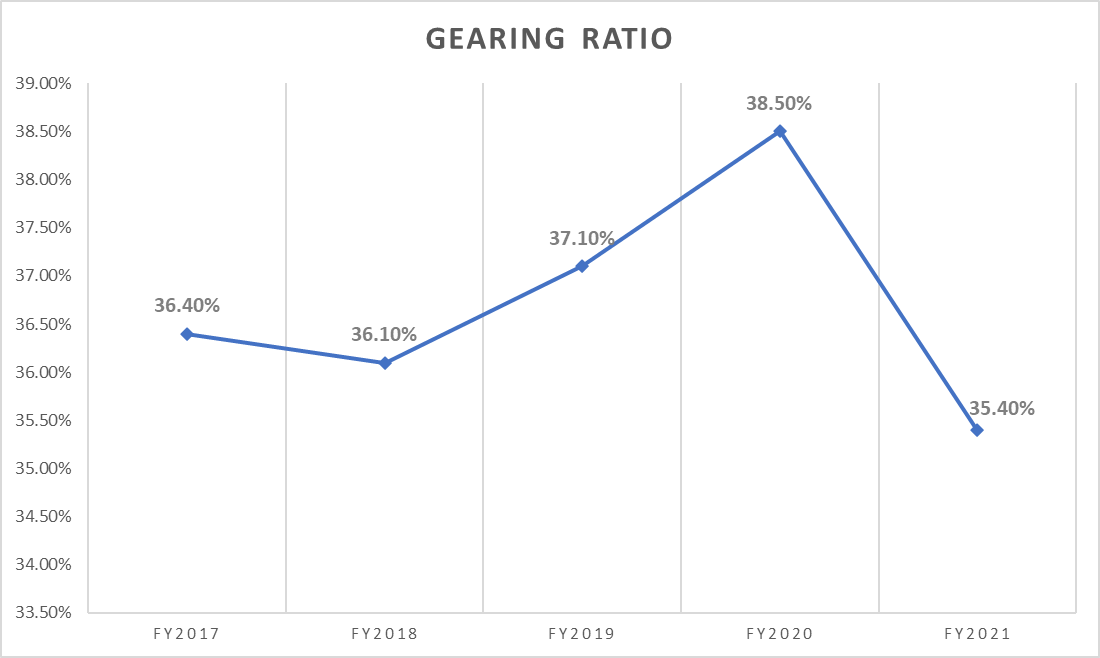

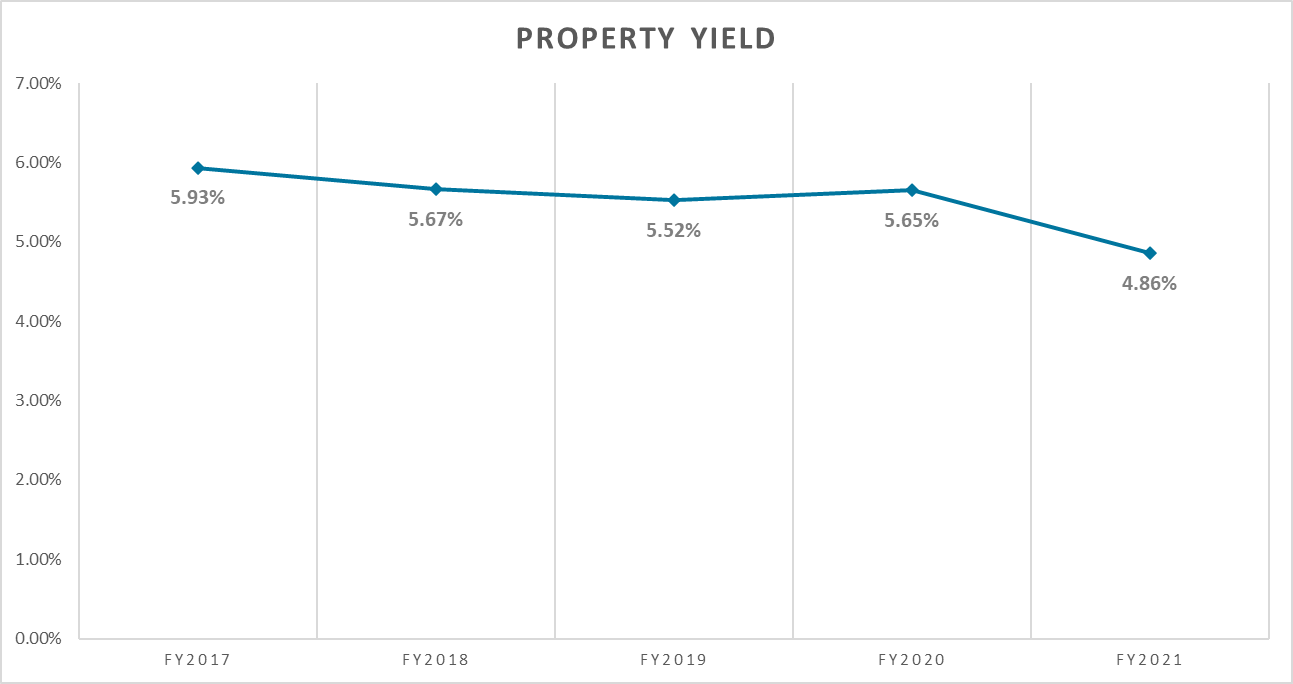

Parkway Life REIT: Gearing Ratio and Property Yield

Gearing Ratio fell to 35.4% ($828.5 million) for FY21 from 38.5% in FY20, owing to a valuation uplift and yearly value increase in Singapore Portfolio. As of December 31, 2021, it had a value gain of $239.2 million (11.7%) on the overall portfolio. This demonstrated that PLife REIT is financially sound, as it has $410.7 million and $686.0 million in debt headroom before meeting its 45 percent and 50 percent gearing limits respectively (On April 16, 2020, MAS raised the leverage ceiling for S-REITs from 45 percent to 50 percent).

Similarly, PLife REIT property yield fell mostly owing to a $239.2 million increase in valuation gain (11.7% ). As a result, the property yield in FY21 decreased to 4.86% from 5.65% in FY20.

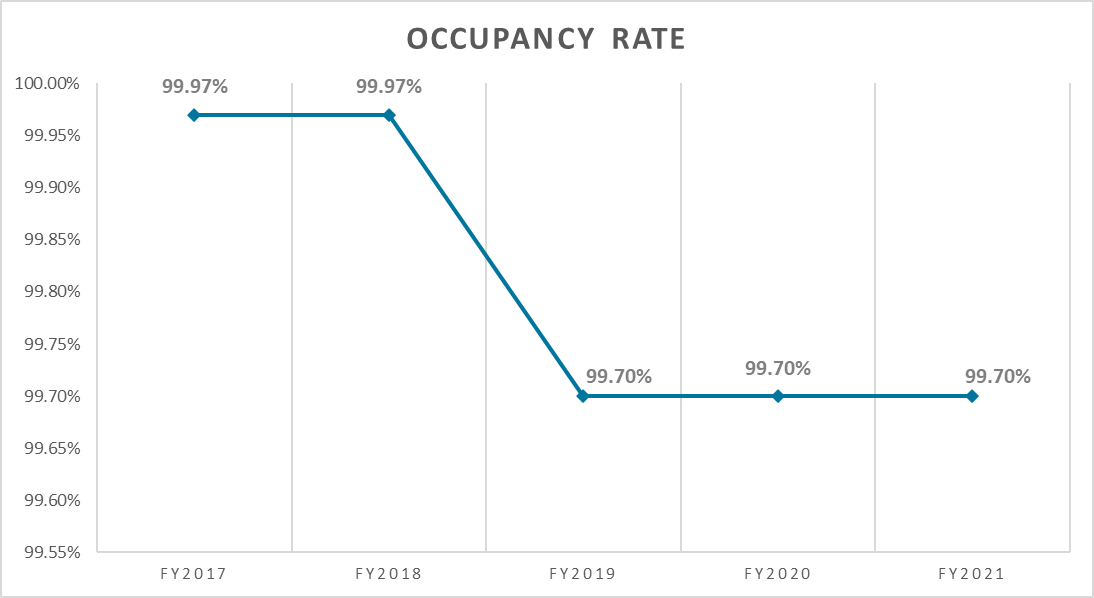

Parkway Life REIT: Occupancy Rate

Due to the fall in Malaysia committed occupancy, occupancy rates have declined to 99.70% (FY19, FY20, and FY21) from 99.97 % (FY17 and FY18). An existing lease is set to expire on February 28, 2019, and PLife REIT is considering converting its vacant space to Medical Suites.

Parkway Life REIT: Interest Coverage Ratio

PLife REIT has no long-term debt refinancing needs till June 2023. The Weighted Average Debt Term increased from 3.4 years to 3.9 years (as of December 31, 2021). PLife REIT has an impressive interest coverage ratio of 21.5 times, demonstrating its solid financial health and ability to satisfy interest commitments.

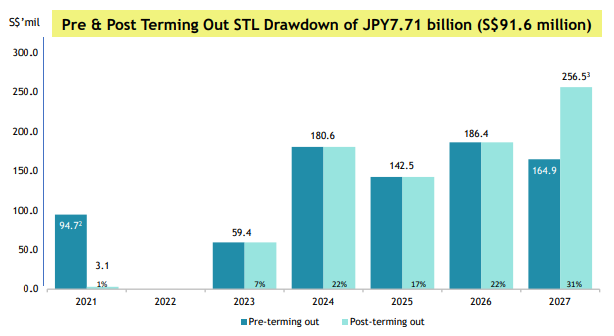

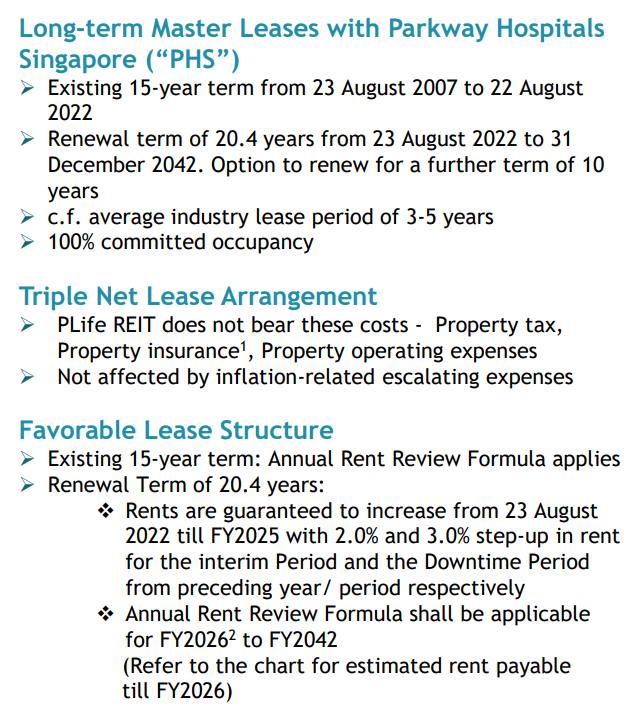

Parkway Life REIT: Rental Reversions

PLife REIT Singapore Portfol io is the master lessee of 3 Singapore Hospitals: Mount Elizabeth Hospital, Gleneagles Hospital and Parkway East Hospital. The triple net lease agreement’s renewal period will run from 23 August 2022 to 31 December 2042, with an option for a 10-year extension. Rents would rise by 2.0 percent in FY22 and FY23, and 3.0 percent in FY24 and FY25, according to the contract.

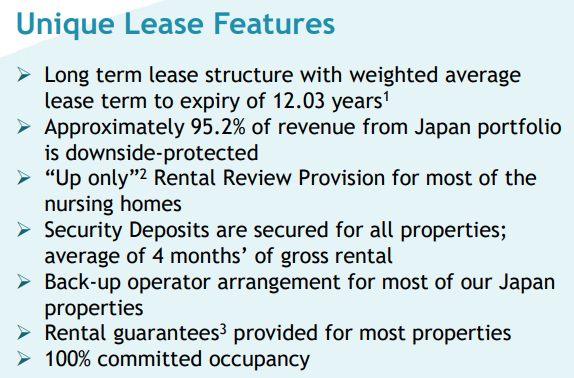

As for the Japan Portfolio, it has a unique lease future of a “Up only” rental structure for most of the nursing homes. In essence, this means that the leasing rate for its nursing home will only go up.

Thus, despite economic conditions, both the Singapore and Japan rental reversions portfolios demonstrate that rent will continue to rise gradually to keep inflation at bay.

Growth Prospects

PLife REIT’s growth goal is to form strategic long-term partnerships with high-quality local lessees and operators, as well as expand into expanding healthcare markets. PLife REIT will be able to benefit from the aging populations of Japan and Singapore. According to a projection published by World Population Prospects, by 2050, one-third of the population would be 65 or older. Similarly, Singapore, which has one of the world’s lowest fertility rates at 1.15 children per woman, has one of the lowest fertility rates in the world. Around a third of Singaporeans are predicted to be 65 or older by 2035, while the median age is expected to climb from 39.7 in 2015 to 53.4 in 2050.

With the Asia-Pacific region’s rapidly increasing healthcare industry, demand for excellent healthcare and aged care services will begin to rise. As a result, PLife REIT will be in a great position to benefit from these favorable conditions.

Dividend Yield

Dividend Yield (5 Year)

The current Dividend Yield of PLife REIT stands at 3.16%,it’s 5-year Avg Yield stands at 4.05%

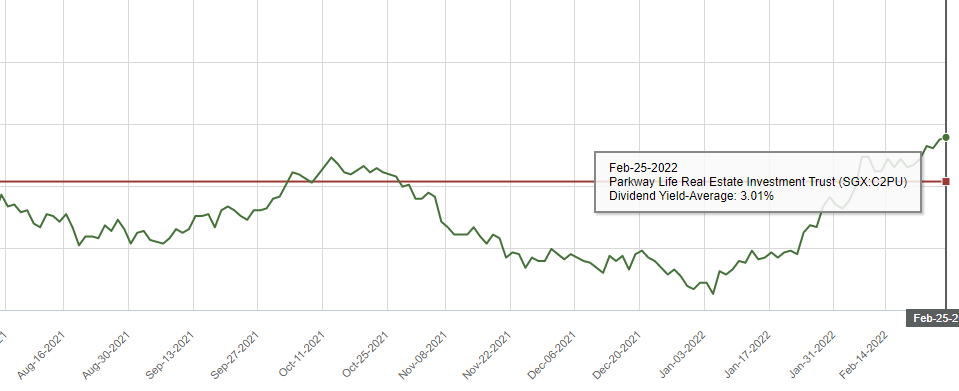

Dividend Yield (1 Year)

The current Dividend Yield of PLife REIT stands at 3.16%,it’s 1-year Avg Yield stands at 3.01%

Our Stand

PLife REIT has been one of the best performing REITs since its inception, PLife REIT has also built a long-term track record of delivering:

- Strong historical growth in Gross Revenue, NPI and DPU

- Favourable Lease Arrangements – Long Lease Tenure, Guaranteed Rent Increments

- Strong tailwinds for future growth

PLife REIT, despite its strong fundamentals, nevertheless appears a little overpriced to me, with a current dividend yield of 3.16%. Before investing, I would prefer a bigger margin of safety and a yield of about ~5% yield.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.