Frasers Centrepoint Trust (“FCT”) is a leading developer-sponsored retail real estate investment trust (“REIT”) and one of the largest suburban retail mall owners in Singapore. FCT’s property portfolio comprises 9 retail malls and an office building located in the suburban regions of Singapore, near homes and within minutes to transportation amenities. The retail portfolio has approximately 2.2 million square feet of net lettable area with over 1,400 leases with a strong focus on providing necessity spending, food & beverage and essential services.

FCT is among the TOP 10 largest Singapore REITs (“S-REITs”) by market capitalization. Moreover, FCT is constituent of several benchmark indices. These include the likes of FTSE EPRA/NAREIT Global Real Estate Index Series (Global Developed Index), FTSE ST Real Estate Investment Trust Index, MSCI Singapore Small Cap Index and the SGX iEdge S-REIT Leaders Index.

FCT has an asset under management of SGD 6.2 billion.

Let’s take a look at what Frasers Centrepoint Trust has to offer.

Overview of Business

Key Highlights to Note:

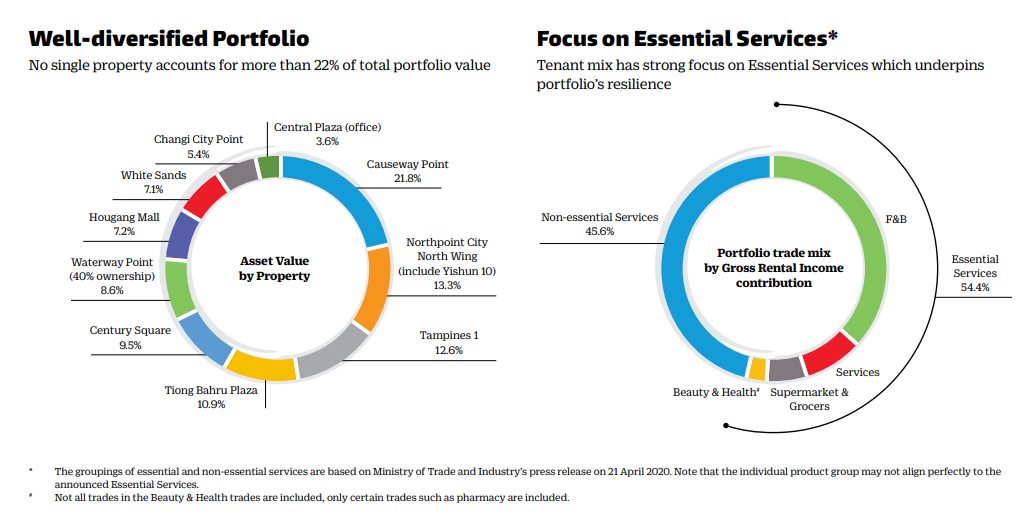

- Portfolio: 9 suburban malls and 1 office building

- Portfolio Breakdown:

- Central Plaza – Office (3.6%)

- Changi City Point (5.4%)

- White Sands (7.1%)

- Hougang Mall (7.2%)

- Waterway Point – 40% ownership (8.6%)

- Century Square (9.5%)

- Tiong Bahru Plaza (10.9%)

- Tampines 1 (12.6%)

- Northpoint City North Wing – Include Yishun 10 (13.3%)

- Causeway Point (21.8%)

- Focus on Essential Services – F&B, Services, Supermarket & Grocers and Beauty & Health

- Portfolio Breakdown:

- Retail Portfolio Net Lettable Area (NLA): ~ 2.3 million square feet

- Retail Portfolio Leases: >1,400

- Catchment Population: 2.6 million

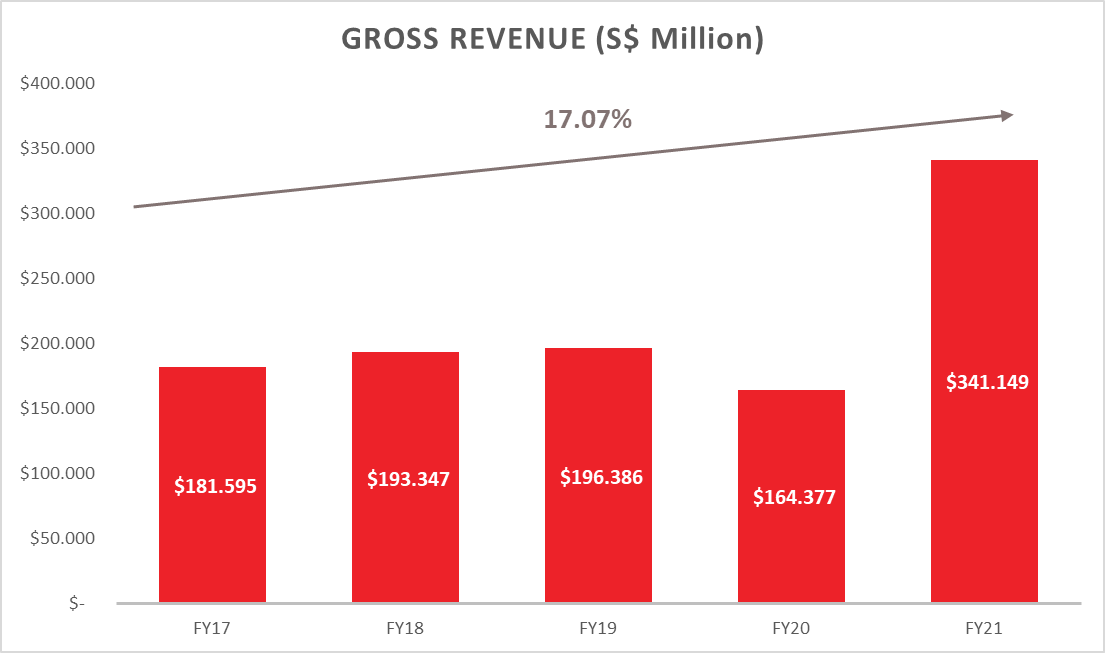

Gross Revenue & Net Property Income

Gross Revenue increased 107.5% year-over-year from S$164.38 million in FY20 to S$341.15 million in FY21. This exponential increase is greatly boosted by ARF Acquisition (approximately 11 months of contribution). The performance in 2H2021 was lower than 1H2021 as a result of:

- The rental rebates provided under the Government’s Rental Framework

- Additional Tenant Assistance provided

- The decrease was partially offset by full contribution in 2H2021 from the ARF Acquisition

Hence, the CAGR of FCT’s Gross Revenue over 5 years grew at an astounding rate of 17.07% from FY17 to FY21.

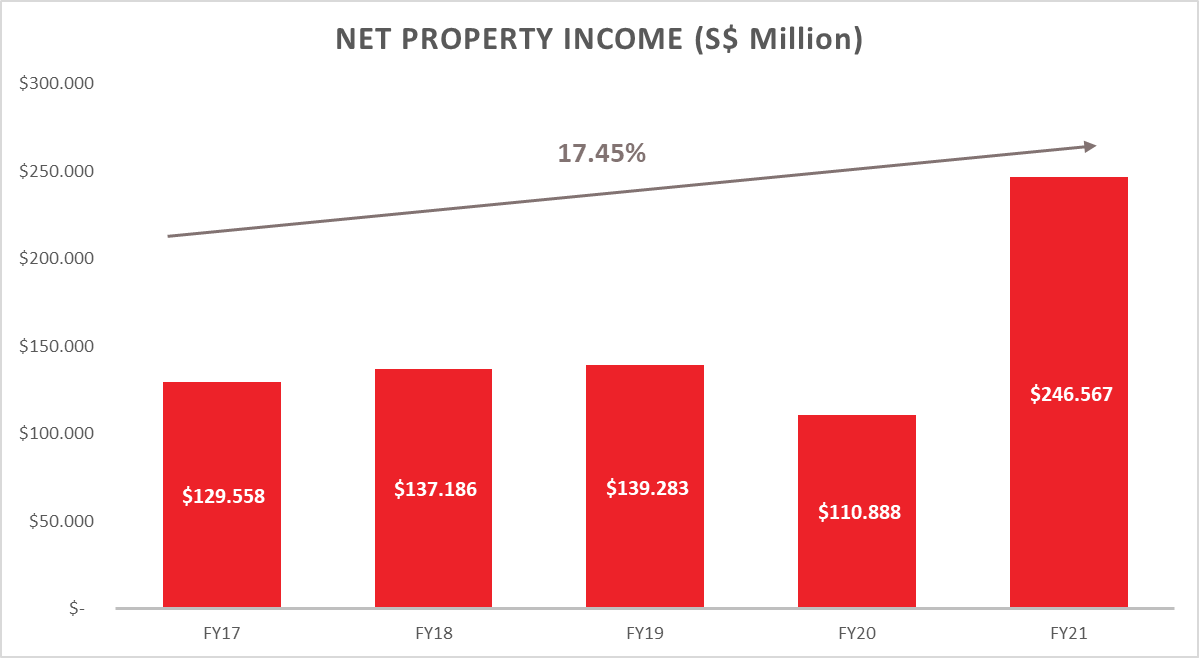

Net Property Income (NPI) increased 122.4% year-over-year from S$110.89 million in FY20 to S$246.57 million in FY21. Similar to the Gross Revenue, its strong performance is attributed to the portfolio acquisition of ARF. Moreover, FY21 Net Property Income margin recovered to 72.3% from 67.5% in FY20. Hence, the CAGR of FCT’s NPI over 5 years grew at a strong pace of 17.45% from FY17 to FY21.

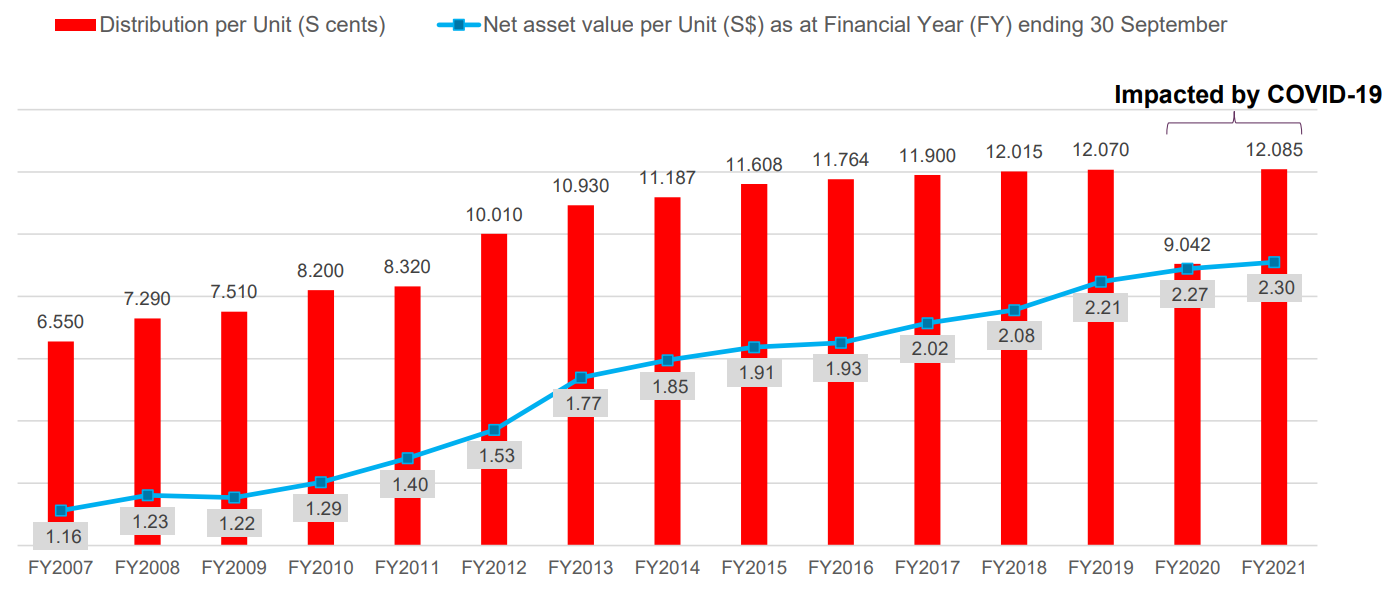

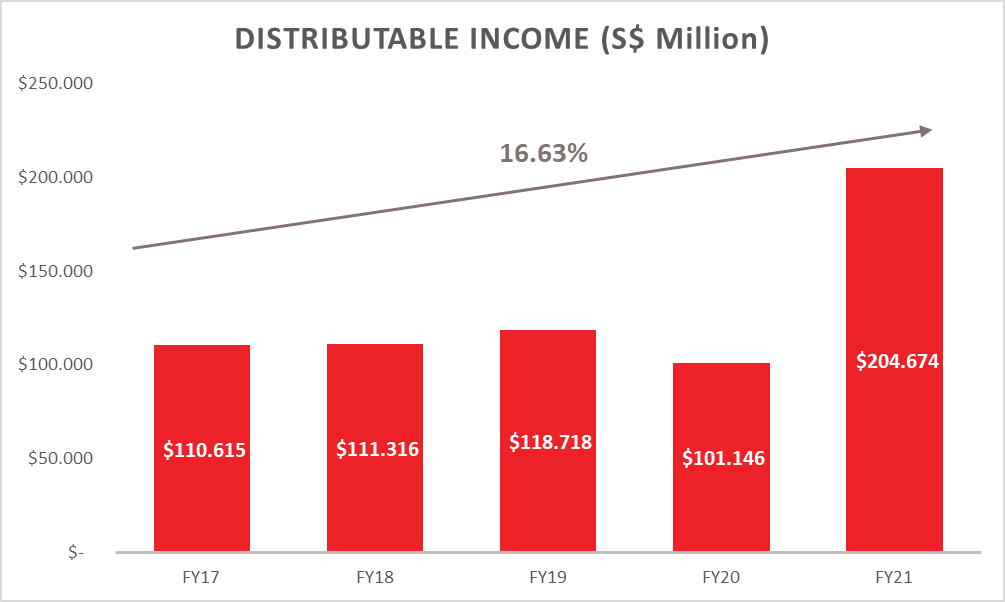

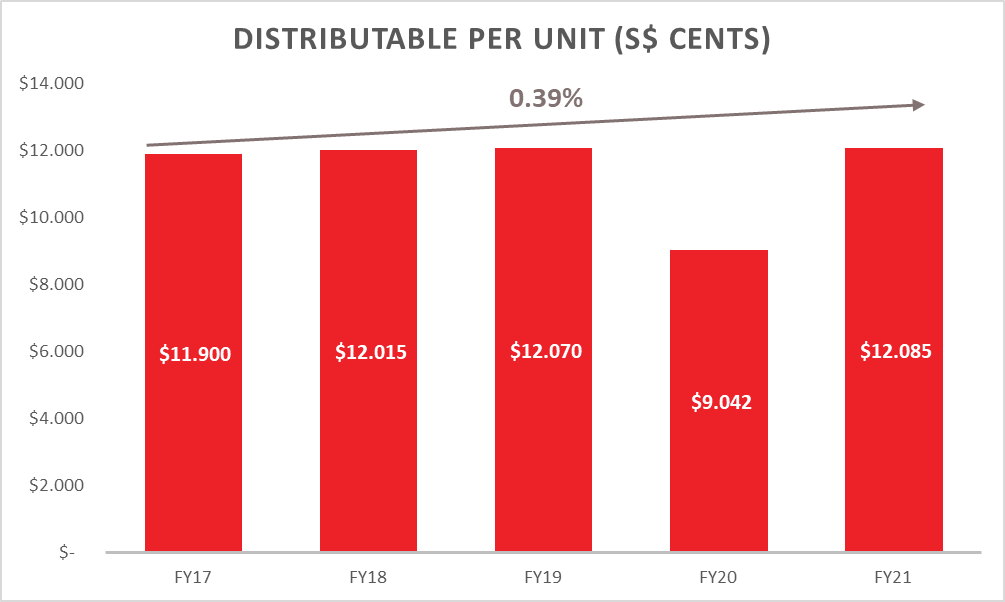

Distributable Income & Distribution Per Unit

Distributable Income increased 102.4% year-over-year from S$101.15 million in FY20 to S$204.67 million in FY21. Hence, the CAGR of FCT’s Distributable Income over 5 years grew at a rapid pace of 16.63% from FY17 to FY21.

Distribution Per Unit (DPU) increased 33.7% year-over-year from (S$) 9.042 cents in FY20 to (S$) 12.085 cents in FY21. FY21 DPU of (S$) 12.085 cents represents a trading yield of 5.3% based on the closing price of S$2.27 on 30 September 2021. Hence, the CAGR of FCT’s DPU over 5 years grew steadily at 0.39% from FY17 to FY21.

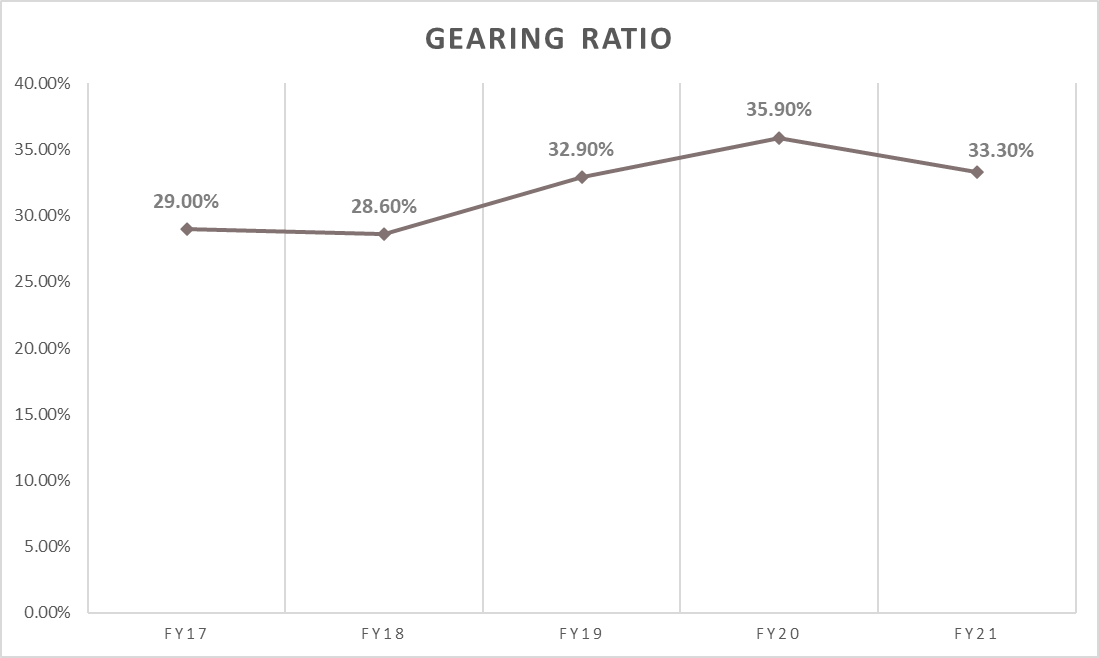

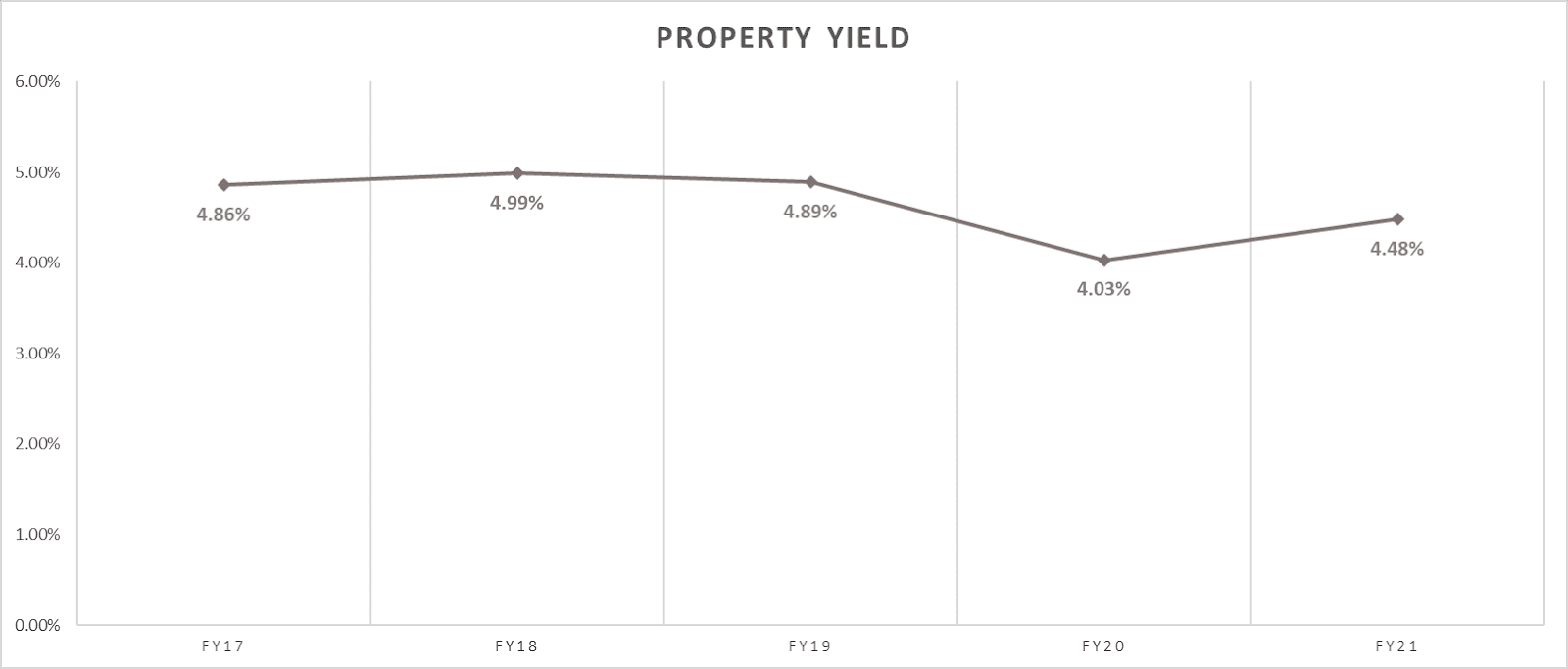

Gearing Ratio & Property Yield

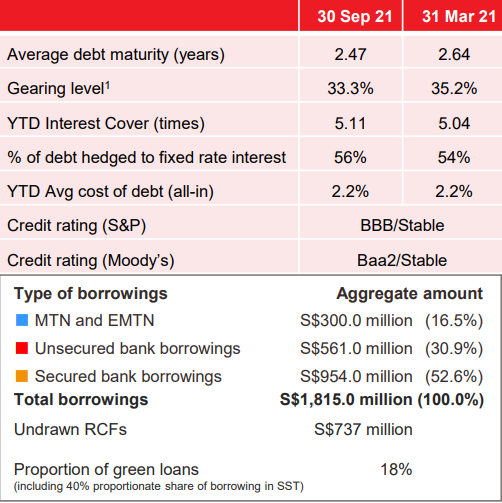

FCT’s gearing ratio is 33.3% as at 30th Sep 2021. FCT total debt increased to $1.82 billion, where the weighted average tenor of debt is 2.47 years. FCT is financially sound as it has additional $637.7 million and $910.2 million in debt headroom before meeting its 45% and 50% gearing limit respectively (In April 2020, MAS raised the leveraged ceiling for S-REITS from 45% to 50%).

Furthermore, FCT still have a strong balance sheet to purse growth opportunities:

- ‘BBB’ rating with stable outlook by S&P and ‘Baa2’ rating with stable outlook by Moody’s

- 5.11 times YTD Interest Cover

- 56% of debt hedged to fixed rate interest

Similarly, FCT’s property yield increased slightly to 4.48% in FY21 from 4.03% in FY20. This could be due to an increase in valuation, where valuations were depressed previously during the start of the pandemic.

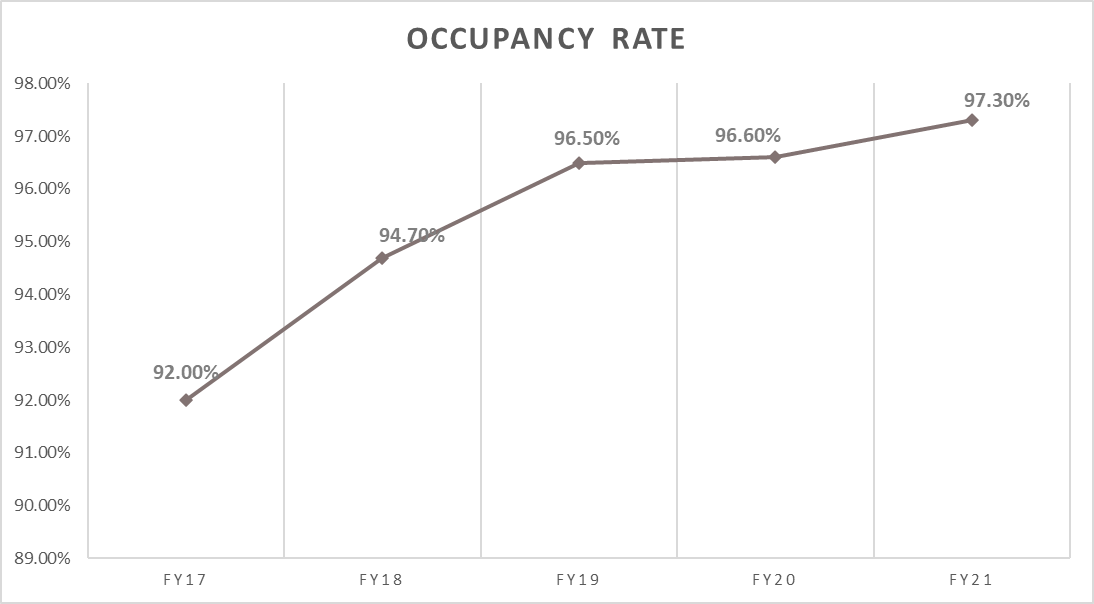

Occupancy Rate

FCT’s Occupancy rate of the Overall Portfolio is 97.3% in FY21 from 96.6% in FY20. Despite the challenges, FCT were able to achieve occupancy improvement and brought in new tenants to their malls. This enabled them to refresh the tenant mix to adapt to evolving consumer preferences. The portfolio occupancy increased with pick up in leasing activities as Singapore continues to work towards normalization. However, retailers remain cautious with the increase in community cases and tightening of safe management measures.

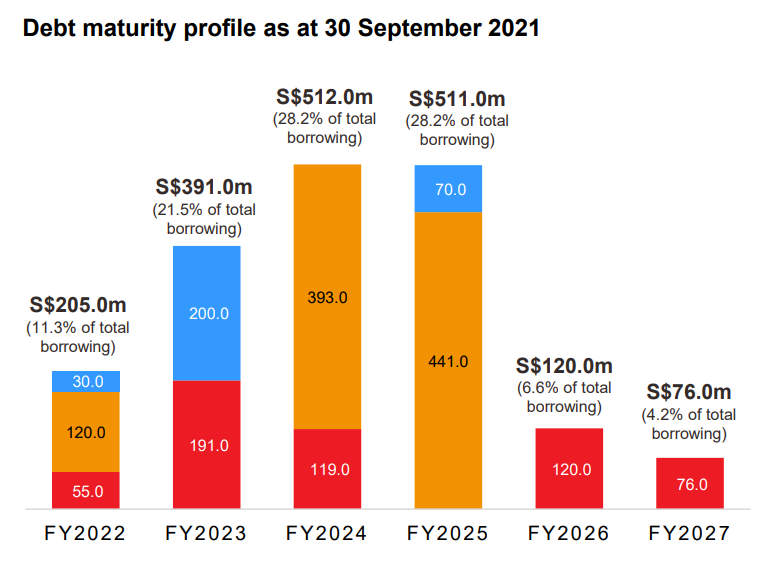

Debt Risk Management

FCT’s Average Debt Maturity is 2.47 years. Furthermore, FCT has an impressive Interest Coverage Ratio (ICR) for FY21 of 5.11 times, this demonstrates its solid financial health and ability to satisfy interest commitments. In FY22, it has a total debt of S$205.0 million which is 11.3% of total borrowing.

Rental Reversions

The Average Rental Reversion for the Retail Portfolio in FY21 was relatively flat at -0.6%, based on the variance between the rent in FY20 incoming lease and the rent in the FY21 outgoing lease. Furthermore, rental reversion in FY21 was lower than previous years, due to weaker retailer sentiments affected by the COVID-19 disruptions.

With the overhang of COVID-19, these malls remained resilient:

- Causeway Point

- Northpoint City North Wing

- Waterway Point

- White Sands

- Tiong Bahru Plaza and

- Hougang Mall

In addition, Changi City Point suffered sharp negative rental reversion due to weak shopper traffic and sales. This is attributed to workers in Changi Business Park and Singapore Expo started adopting work-from-home which translated into reduced traffic.

Growth Prospects

There are a couple of potential growth prospects for Frasers Centrepoint Trust. FCT will be looking into its Sponsor’s pipeline: Northpoint City South Wing. which is owned by Frasers Property and the TCC Group. Concurrently, FCT will also continue to refine its portfolio to optimize returns for the Trust and its unitholders. FCT might also be looking into 3rd party opportunities, including potential for additional stake in Waterway Point. As FCT is in a strong financial position, it provides ample debt headroom for acquisition.

FCT is looking to adapt and position for omnichannel retailing. They have recently established 2 digital platforms: Frasers eStore and the Enhanced Makan Master. Frasers eStore saw 3X Sales growth between Jan 2021 (launch) and August 2021. While Makan Master saw a 7X Sales Growth and Avg Order Size increased 2X between April 2020 (launch) and August 2021.

Fortunately, the suburban retail sector in Singapore has remained relatively resilient through the various COVID-19 phases. The easing of the safe management measures will support the recovery of tenants’ sales and shopper traffic at FCT’s malls. In the near-term, the Manager will continue to focus on managing the operational and financial performance of FCT’s portfolio, taking into consideration the evolving COVID-19 pandemic.

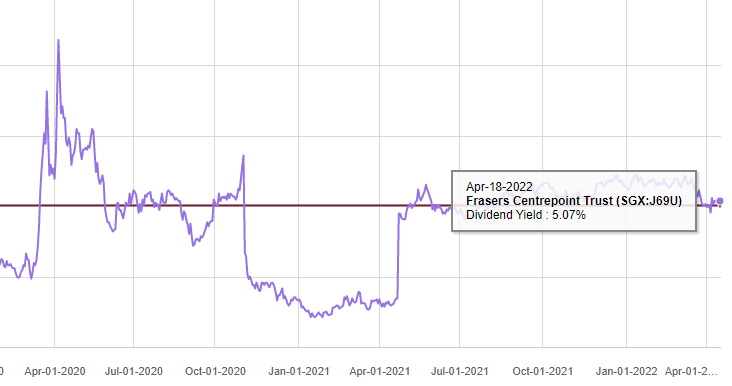

Dividend Yield

Dividend Yield (5 Year)

The current Dividend Yield of FCT stands at 5.07%,it’s 5-year Avg Yield stands at 5.01%

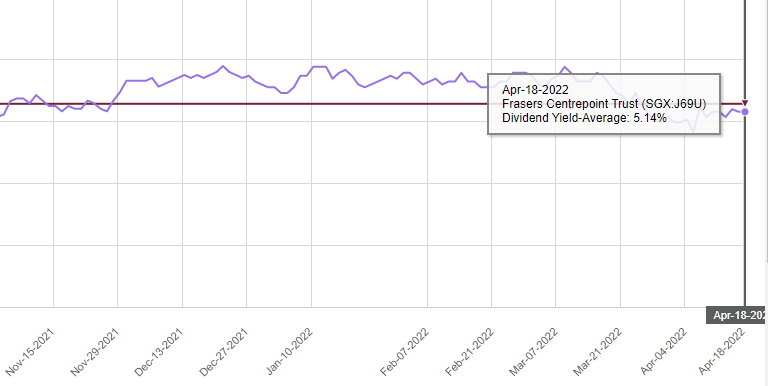

Dividend Yield (1 Year)

The current Dividend Yield of FCT stands at 5.07%,it’s 5-year Avg Yield stands at 5.14%

Our Stand

FCT has been one of the best performing REITs since its inception, as it has built a long-term track record of delivering:

- Consistent historical growth in Gross Revenue, NPI and DPU

- Management are looking for AEI and Acquisition opportunities

- Manageable debt which displays how prudent the management team are

FCT, with its consistent fundamentals, appears fairly priced to me, with a current dividend yield of 5.07%.If the yield rises to ~7+%, I would consider adding it to my portfolio. Other interesting REITs that you may want to look at are: Parkway Life REIT and Mapletree Industrial Trust REIT.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.