It’s no secret that financial planning is an essential part of achieving a secure future. But having a plan in place can also be a great way to reach your goals in the near future. With 2023 quickly approaching, now is the perfect time to start putting together a financial plan. This will enable you to have a roadmap to potentially achieve your goals and lead you to success. I am sure this is not a foreign topic to many. Financial planners and insurance agents frequently begin their conversations with this subject.

Some may ask, how necessary is it for one to put together a financial plan?

If you want to be successful in life, it’s important to have a financial plan. A financial plan will help you set goals and track your progress. It will also help you make informed decisions about your money.

Without a financial plan, it’s easy to make impulse purchases or decisions that are not in your best interest. A financial plan can help you avoid these mistakes and stay on track with your goals. A financial plan can also help you during tough times. This is especially true in times when you experience a job loss or unexpected medical bills. Having a plan in place will give you peace of mind and help you weather any storms that come your way.

In this blog post, we’ll discuss how to create an effective financial plan for 2023 that covers all areas of your life. We’ll look at creating budgets across different aspects. Savings goals, Investing wisely, Purchasing insurance so that you can maximise your chances of success in the coming year.

#Step 1 in Financial Plan: Track your current Net worth

For anyone that is new to financial planning, you should first track your current net worth. This provides you with a snapshot of your current financial health while mapping out your financial strategy.

To calculate your net worth, it is the summation of all your assets and then subtracting any outstanding debts. All forms of savings, financial investments, and real estate are considered assets. On the other hand, debts refers to any financial liabilities to banks or creditors. Consolidating all these together will provide you a clearer snapshot of your current financial health.

If you haven’t already done that, you’re in luck. Below is a Stock and Assets Template that we have created for our readers. Feel free to duplicate a copy to start tracking your assets and calculate your net worth. In addition, if you find our template to be extremely helpful, please follow us. Both our Instagram or Telegram shares any updates on new templates and articles.

#Step 2 in Financial Plan: Set your Financial Goal for 2023

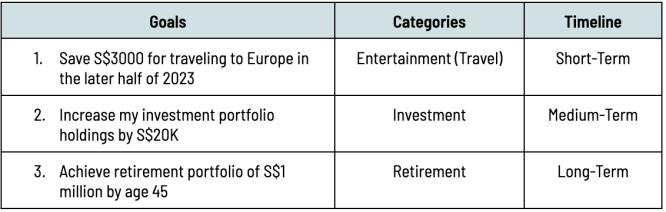

Next would be setting tangible and realistic financial goals for 2023. Depending on each person’s needs and the different stages of their lives, these goals may vary. Savings for a holiday, clearing off debt, or investing for retirement may be preferred by some.

Hence, I would advise people to break down their financial goals into different categories and across different timelines. This is because some goals may be short-term (within a year), whereas others may span over a number of years.

Below is an example of my financial goals for 2023:

#Step 3 in Financial Plan: Develop a Budget

The next stage would be to keep tabs on your monthly earnings and spendings in order to create a budget. This budget will allow you to stay on track with your financial goals that you set in Step 2.

For tracking of spendings, there are a couple of good applications which include Spendee, Planner Bee, Seedly and more. You can check out this article written by Planner Bee which shares the best budgeting apps to manage their expenses. Personally, I have used Spendee for tracking my monthly expenses for more than two years now. My current monthly spending is estimated to be at around $1.5K.

In Singapore, the median monthly income for Singaporeans recently rose to S$5,070 in 2022. This will translate to a take-home pay of S$4,056 after CPF contributions. This will translate into an average monthly savings of roughly S$2.5K when my expenses are subtracted.

Given my average monthly savings of S$2.5K, this is in-line with both my short and long-term financial goal. As a result, my objective will be to monitor my monthly expenditure and ensure that it stays within my budget.

#Step 4 in Financial Plan: Invest wisely in 2023

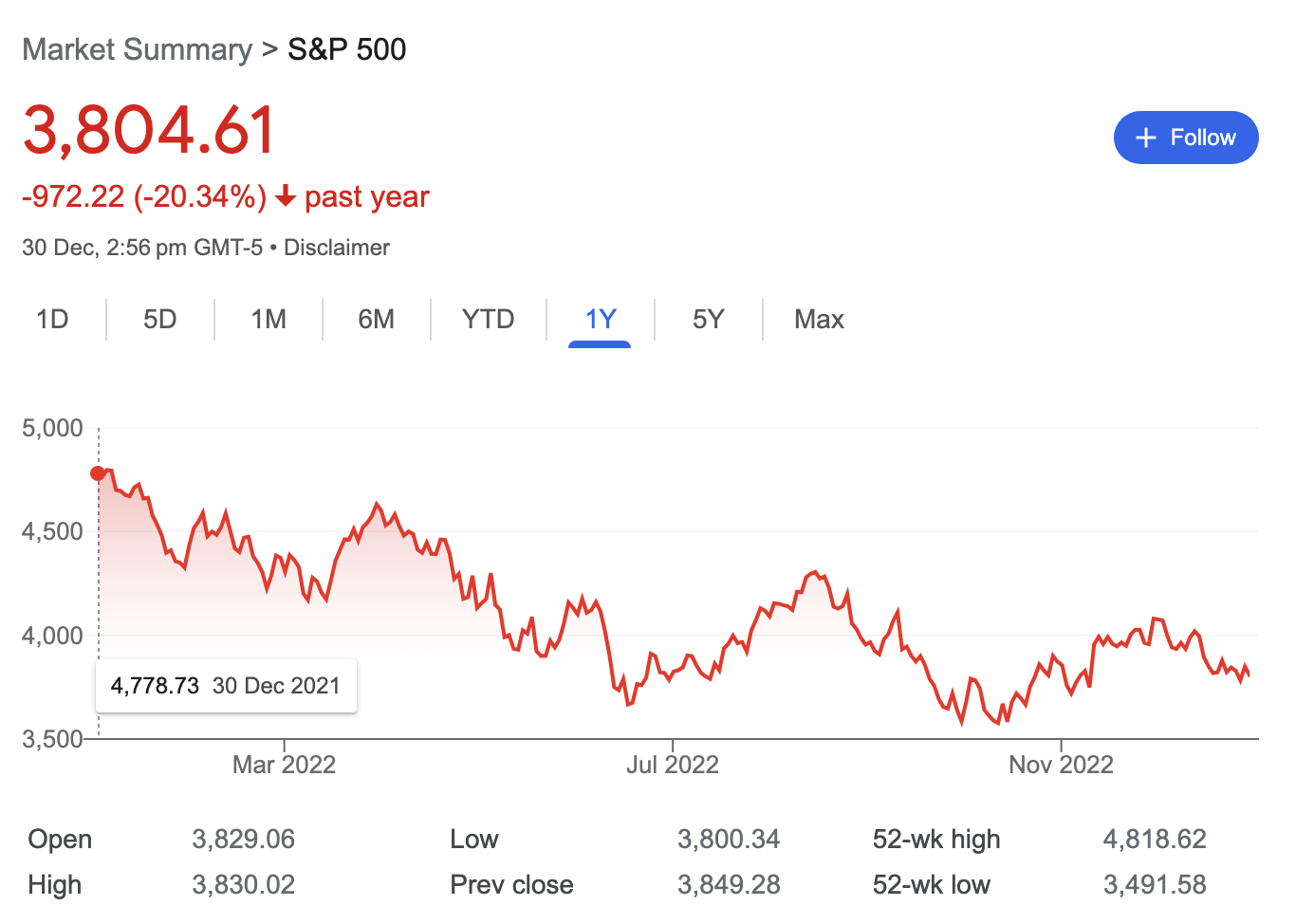

For many investors, 2022 has been incredibly overwhelming and life changing. This is a stark contrast to 2021, when the equity market is experiencing a bull market. As a result of experiencing both market circumstances, many investors have had to reconsider their investing approach. Saving Bonds and Treasury Bills have become a popular form of investment for many singaporeans.

Here are a few general investing tips that could be helpful as you approach 2023:

- Review and update your investment strategy: Take this time to review your current investment holdings. Ensure that it is aligned with your financial goals which in my case is Achieving a $1M retirement sum. Do check out our past article on how to prepare your portfolio in times of recession.

- Manage risk and investment timeline: It is crucial to carefully consider the risk and rewards for any investment. Depending on your risk appetite, choose the investment classes that best suit you. Lastly, do research on any investment opportunity before investing in them. Click here to check out our analysis on equities, REITs and banks in SG, HK and US markets.

#Step 5 in Financial Plan: Protect yourself and your family

Lastly, to end off your financial goals would be to understand your current insurance requirements. There are numerous insurance options, and the best combination will depend on your particular situation. The following are a few of the most popular types of insurance:

- Health / Hospitalisation Insurance

- Life Insurance

- Disability / Critical Illness Insurance

It’s important to review your coverage periodically to make sure it still meets your needs. As your life changes, so do your insurance needs. For example, you may need to adjust your life insurance coverage if you have a baby or get married. Or if you start working from home, you may be able to reduce your auto or homeowners insurance rates.

It’s crucial to frequently assess your coverage to make sure it still satisfies your needs. Your insurance requirements alter as you enter different phases of life. If you have a child or get married, for instance, you might need to change your life insurance policy. You could even remove your vehicle or home insurance as many of us are now working remotely.

Our Stand

Developing a financial plan for 2023 can seem like an intimidating task. However, with some careful consideration and research you can easily create a plan that meets your needs. By setting goals, budgeting wisely, taking advantage of investment opportunities, and staying informed about the state of your finances, you will have taken important steps towards achieving your financial objectives in 2023. If you feel overwhelmed or unsure how to start creating a financial plan for the year ahead then it’s worth consulting a professional who can provide tailored advice and guidance.

If you are keen, check out our other latest articles. Trust Bank Referral, How ChatGPT can change the world of copywriting and Best 2023 Citibank credit card deals.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock. All views expressed in the article are the independent opinions of Learn To Invest.