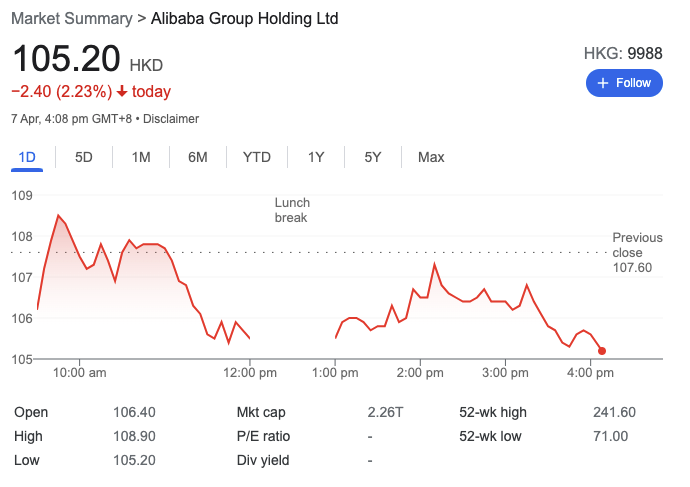

With the recent news on Charlie Munger slashing his stake in Alibaba Stock to the potential delisting news, this has definitely affected the stock price. All this has caused Alibaba’s share price to drop from its high of 300 HKD (Oct 2020) to about 105 HKD today.

That is approximately a 60% fall from its high, hence is now a good buying opportunity? Let’s take a deep dive to better understand the business and its financials.

For more than a year, Alibaba (BABA) has been on a downward trajectory, pulled down by regulatory fears. Hence, investors sentiment has been unfavourable toward Alibaba shares due to several concerns. Some of these bad news include potential delisting by the SEC and China’s potential involvement in the Russia-Ukraine conflict.

As a stock, Alibaba is rather unique as it is dual-listed in the Hong Kong and New York Stock Exchange. However, amidst all the unfavourable news, the Chinese government vow to improve capital market stability. Since then, there has been slight recovery for most of the Chinese equities. At its present share price, the firm has a market capitalisation of HKD$2.31 trillion or ~US$295 billion, which is still more than 60% lower than its all-time high. Multiple financial analysts and value investors have reiterated that most Chinese equities are currently undervalued. Hence, is this a good time to look into Alibaba stock and consider buying it?

Overview of Alibaba’s Business

Alibaba was founded in 1999 by Jack Ma and 17 friends and students as a China-based B2B Marketplace site. Their goal was to improve the domestic e-commerce market for Chinese businesses and assist in exporting Chinese products to the global market. Since 2002, Alibaba has launched multiple complementary initiatives like Taobao Marketplace and Alipay to enhance its e-commerce system. Furthermore, the company has also ventured into new areas like Cloud Computing, FinTech and Entertainment services.

Key Product & Services of Alibaba

Alibaba segregates its business into the following key segments: Commerce, Services, Logistic, Cloud and Digital Media.

Operating Model of Alibaba

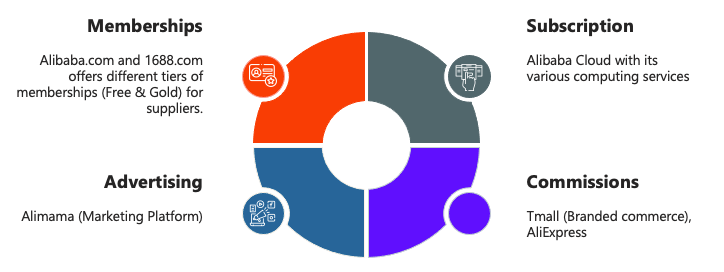

Alibaba Group is a holding company with multiple subsidiaries and profits from a wide range of services. From memberships to advertising and commissions, this is how the different business entities within Alibaba Group generate revenue. Firstly, for its wholesale commerce business (Alibaba and 1688), they generate revenue mainly from paid memberships for suppliers. Secondly, Tmall and Aliexpress, the business profit from each transaction made across both platforms. Lastly, Alimama works like Adsense in China by connecting advertisers to place advertisements across their platforms.

Qualitative Factors affecting Alibaba

Let’s now take a deeper look into the qualitative aspects that affect the business

Alibaba’s Economic Moat

1. Strong E-commerce Network

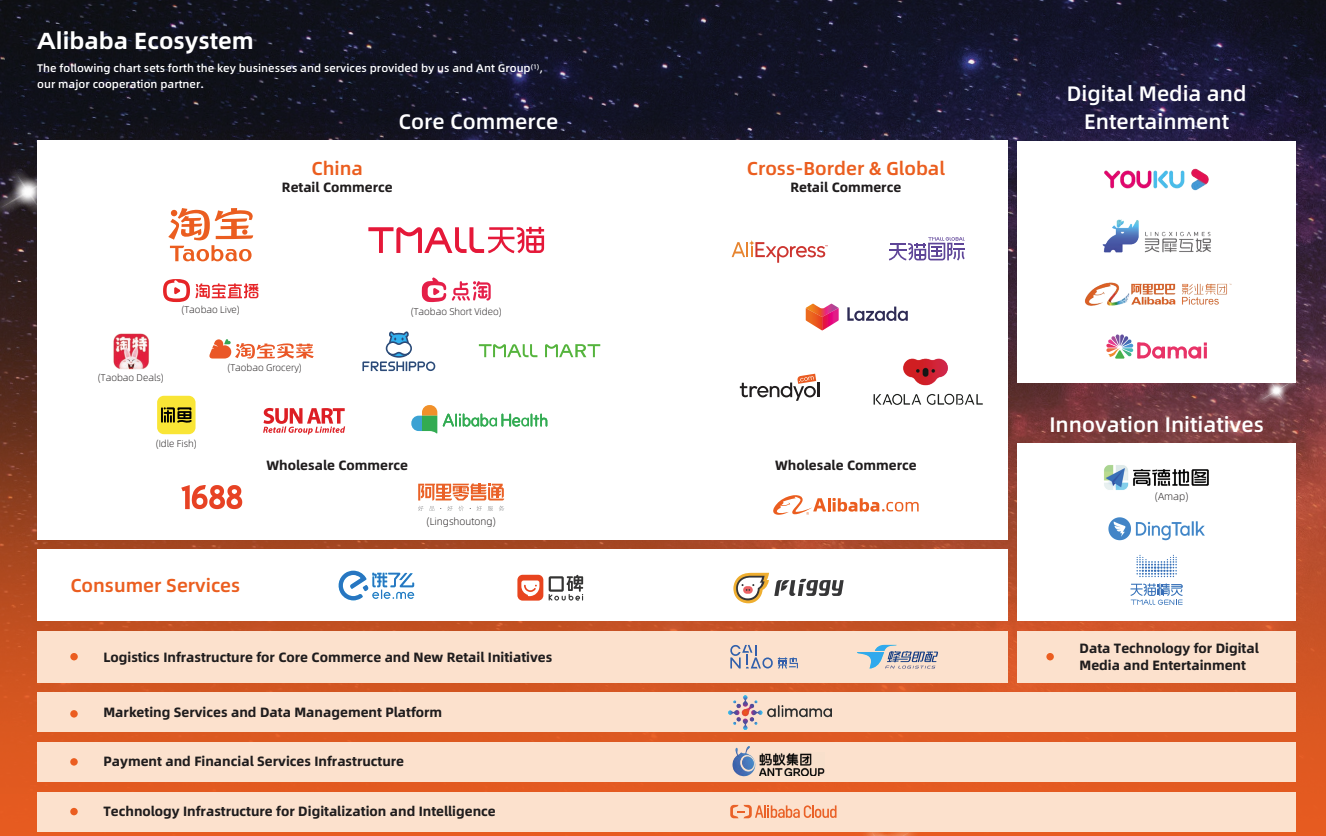

Over the years, Alibaba has grown into a conglomerate with clearly segregated business. For its ecommerce sector, Alibaba.com is for cross-border trade while 1688.com is for Chinese merchants searching for wholesale transactions. Apart from that, Taobao caters to Chinese retail clients, while Tmall caters to high-end branded goods. In addition, it also has enablers in place to make transactions and operation easier for its ecommerce business. For Example: Alimama for marketing, Alicloud for cloud computing, Cainiao for logistics and Ant Financial for payment services. By enabling an ecosystem of independent entities, this ensures accountability, transparency and efficiency for all the business.

2. Market Share Dominance Moat

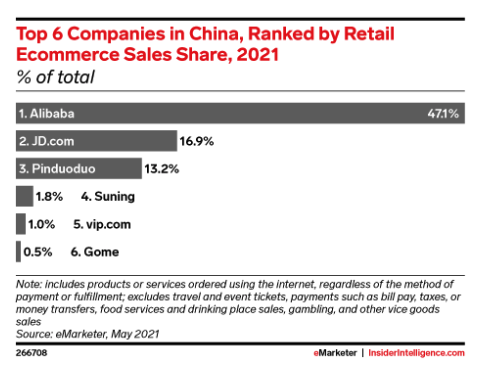

Alibaba intentionally concentrated on Chinese clients rather than omnipresence. It placed them in the center and then constructed the other business around them. As one of the first mover, it has grown to the point that any corporation attempting to enter the game would be thwarted. As a result, the only way to compete with Alibaba in China right now is to concentrate on smaller, niche industries and gradually expand. Hence even with the emergence of JD.com and Pinduoduo, Alibaba is still far ahead of its competitors.

Growth Opportunities for Alibaba

1. Cloud Computing Technology – AliCloud

Alibaba’s cloud platform, AliCloud, has proven to be profitable over the past few quarters. With China’s antitrust regulatory landscape still in place, Alibaba is finding it difficult to expand domestically. As a result, expanding outside of China has become a larger priority. Asia Pacific regions seem to be a key area where Alibaba plans to expand. In the last two years, they have already announced new data centers in South Korea, Thailand and Indonesia. Currently, the total spending for Cloud Infrastructure in China is hovering around $15 billion per annum. This is small when compared to Amazon Web Services (AWS), which made over $45.37 billion in 2021. However, the cloud infrastructure services in China is expanding massively and is the second-largest market. With a 39.8% market share in China Cloud Infrastructure, this shows that there is a massive growth runway available for AliCloud.

2. Ecommerce into Smaller Markets

Alibaba has been actively investing in markets outside of China. This includes Southeast Asian e-commerce sites like Lazada, Turkish e-commerce company Trendyol, and South Asian e-commerce platform Daraz. They have seen success in the developing economies with Lazada’s orders increasing by more than 82% year over year in 2021. Trendyol has also grown its gross merchandise value by more than 80% in 2021. In China, Alibaba has also been targeting more remote areas with value-for-money app Taobao Deals to Community Marketplaces. This has seen strong growth with 240 million deals on Taobao Deals and 150% growth for the Community Marketplaces. Hence, this shows that there is still plenty of room for Alibaba to grow and expand its ecommerce business.

Business Risks

1. Risk Related to Company

Alibaba is bound by an array of laws and regulations in the markets in which it operates. Additional obligations may be imposed by these regulations, which could have a negative impact on their business. Alibaba heavily relies on Alipay for all of the payment processing and escrow services on their marketplaces. If Alipay services and products are limited, this will definitely affect Alibaba’s business. With the crackdown on China’s big tech groups, regulators have plans to break up Alipay and this is definitely worrying for Alibaba.

2. Risk Related to Industry (Competition)

Over the years, Chinese customers have embraced a variety of different buying methods. Consumers are increasingly preferring browsing and interacting with brands. Alibaba has faced increased competition with this new trend of shopping among the Chinese customers. Tencent Holdings Ltd., for example, has begun integrating online retailers inside its WeChat social-messaging platform. Pinduoduo has also introduced game-like elements into shopping. With the help of its algorithms, Douyin is also selling things through short movies and live-streaming. Hence, Alibaba market share has decreased from 78% in 2015 to 51% in 2021. As a result, it waits to see if Alibaba can evolve to meet the ever changing needs of the Chinese customers.

3. Risk related to Doing Business in China

There are risks to doing business in the People’s Republic of China. This includes constant changes to economic policies of the government and uncertainties with interpreting the laws. A good example would be Xin Jinping’s bid for “common prosperity” in 2021. Their aim is to reduce the prosperity gap and encourage the rich and business to give back more to society. To do so, the government is placing more scrutiny on the way these Big Chinese Tech firms use data. Since Alibaba business is still predominantly in China, they will have to closely abide by the regulations to operate smoothly.

Quantitative Factors affecting Alibaba

Let’s now take a deeper look into the quantitative aspects that affect the business

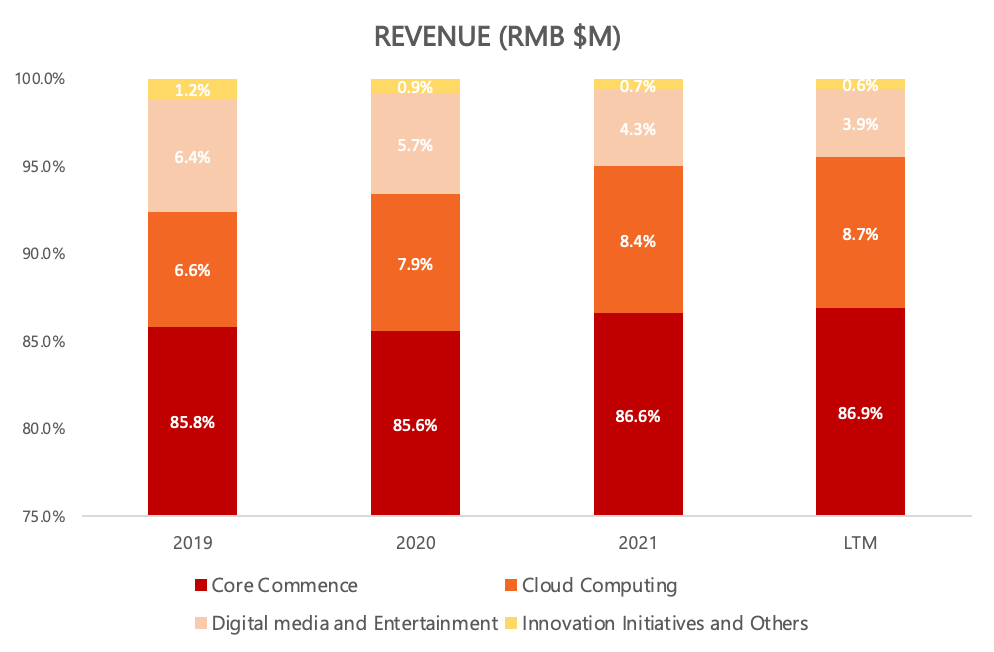

Financial Highlights (Revenue Breakdown)

The majority of Alibaba’s revenue in 2021 and LTM still predominantly comes from their Core Commence business at ~86%. Its cloud computing business has definitely grown over the years to contribute 8.7% of its revenue. The remaining revenue is split between its Digital Media and Innovation initiatives.

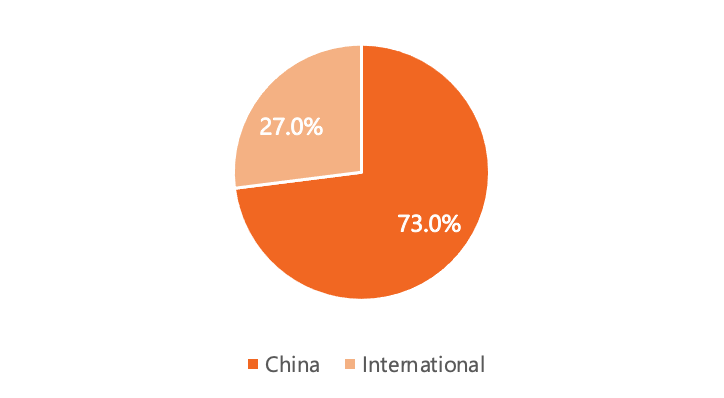

Alibaba started out with the Chinese consumers and business at its core. This explains why ~70% of Alibaba’s revenue still comes from China.

Key Valuation Ratios

When evaluating the financial state of a growing firm like Alibaba, we must assess key financial ratios such as Revenue Growth, P/S, P/E, Gross Margin%, Operating Margin%, and FCF.

Revenue Growth (5 Year)

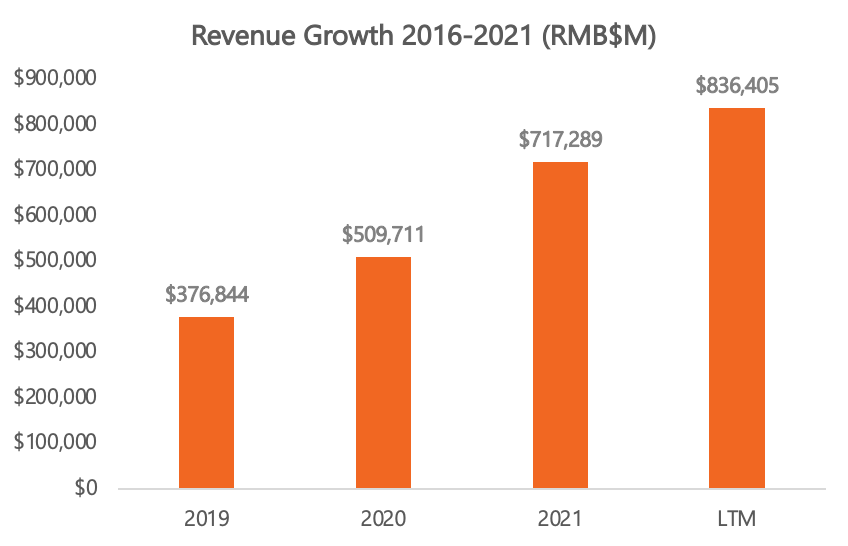

Alibaba’s LTM revenue is at RMB$836B with 29.8% (YoY growth) and 5-Year CAGR stands at 42.2%

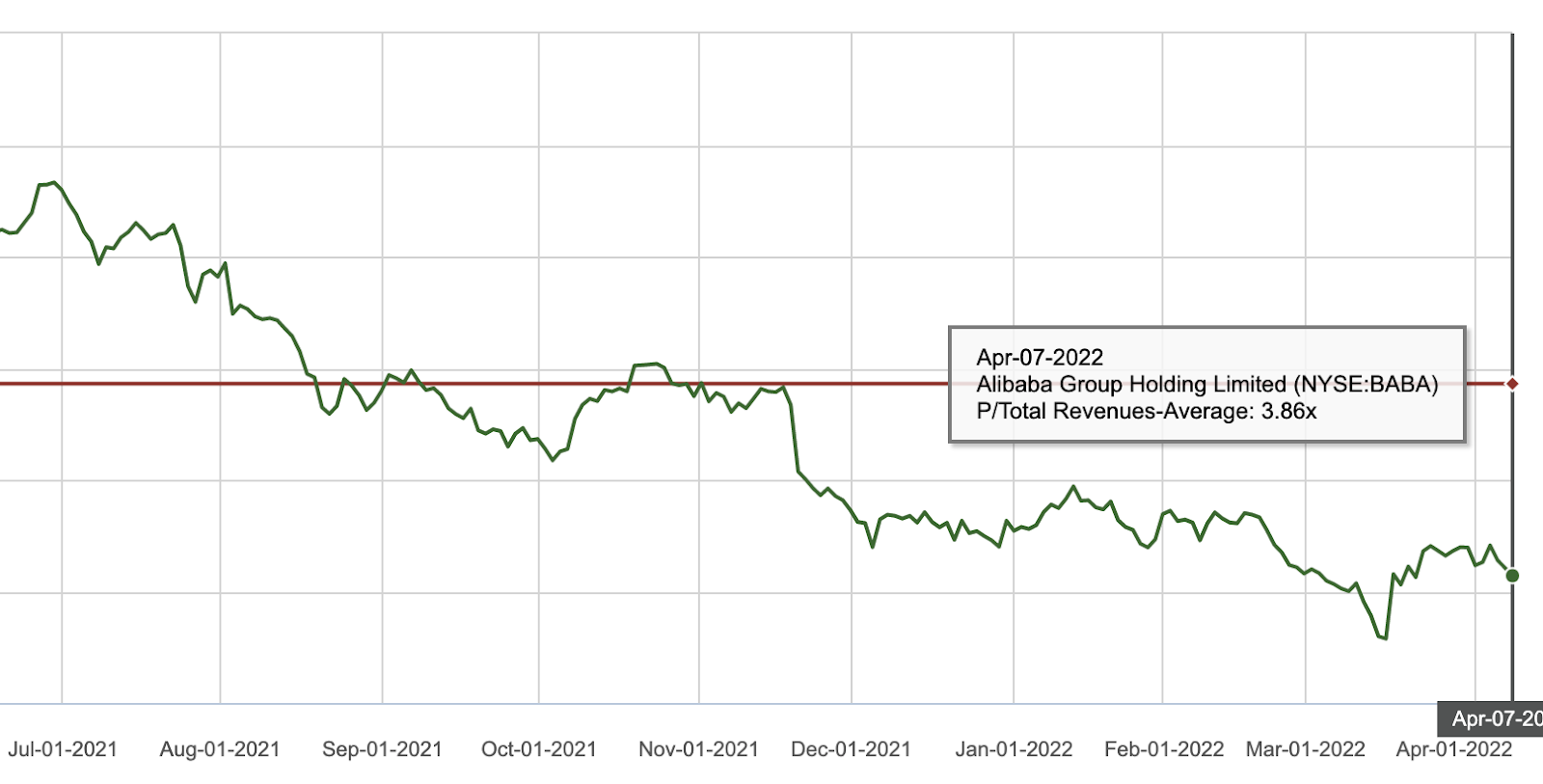

Price/Sales (P/S) ratio (1 Year)

The current P/S Alibaba stands at 2.14x while it’s 1-year Avg P/S ratio stands at 3.86x

Price/Sales (P/S) ratio (5 Year)

The current P/S Alibaba stands at 2.14x while it’s 5-year Avg P/S ratio stands at 9.12x

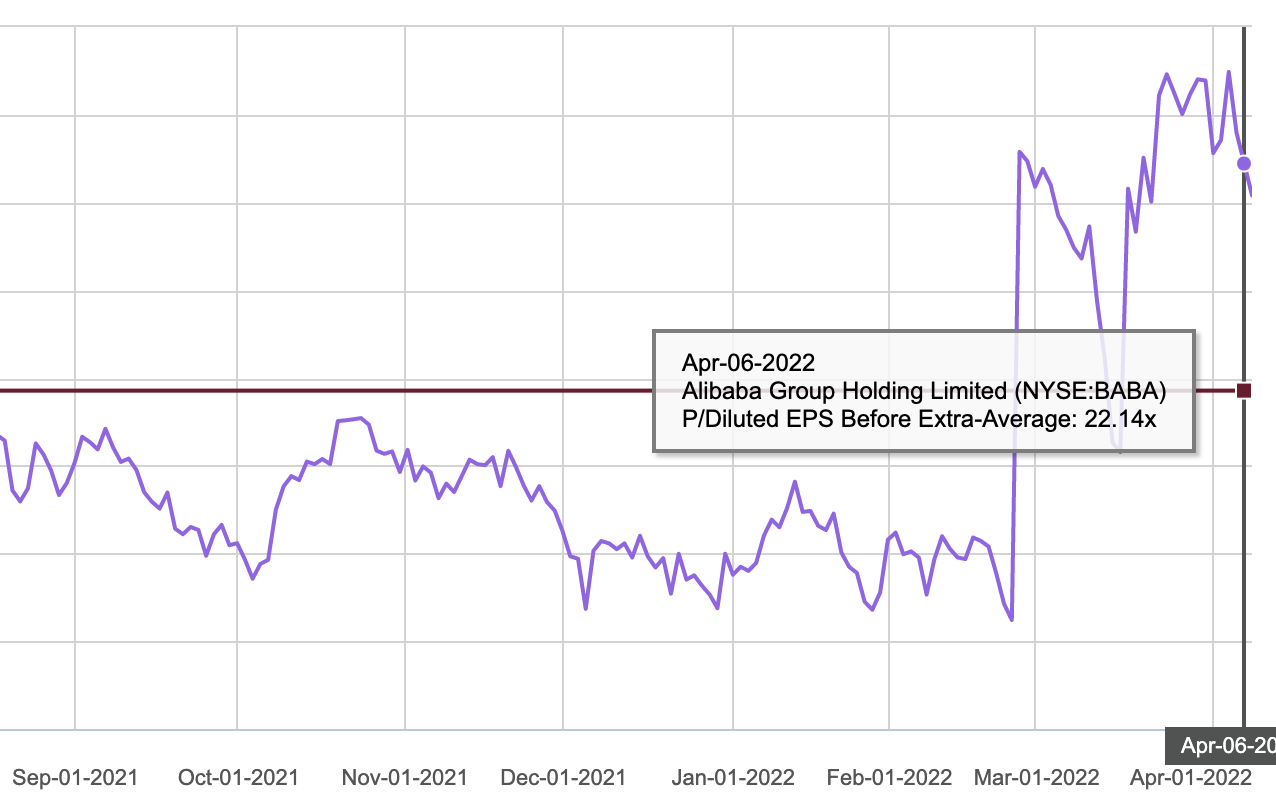

Price/Earning (P/E) ratio (1 Year)

The current P/E Alibaba stands at 27.7x while it’s 1-year Avg P/E ratio stands at 22.14x

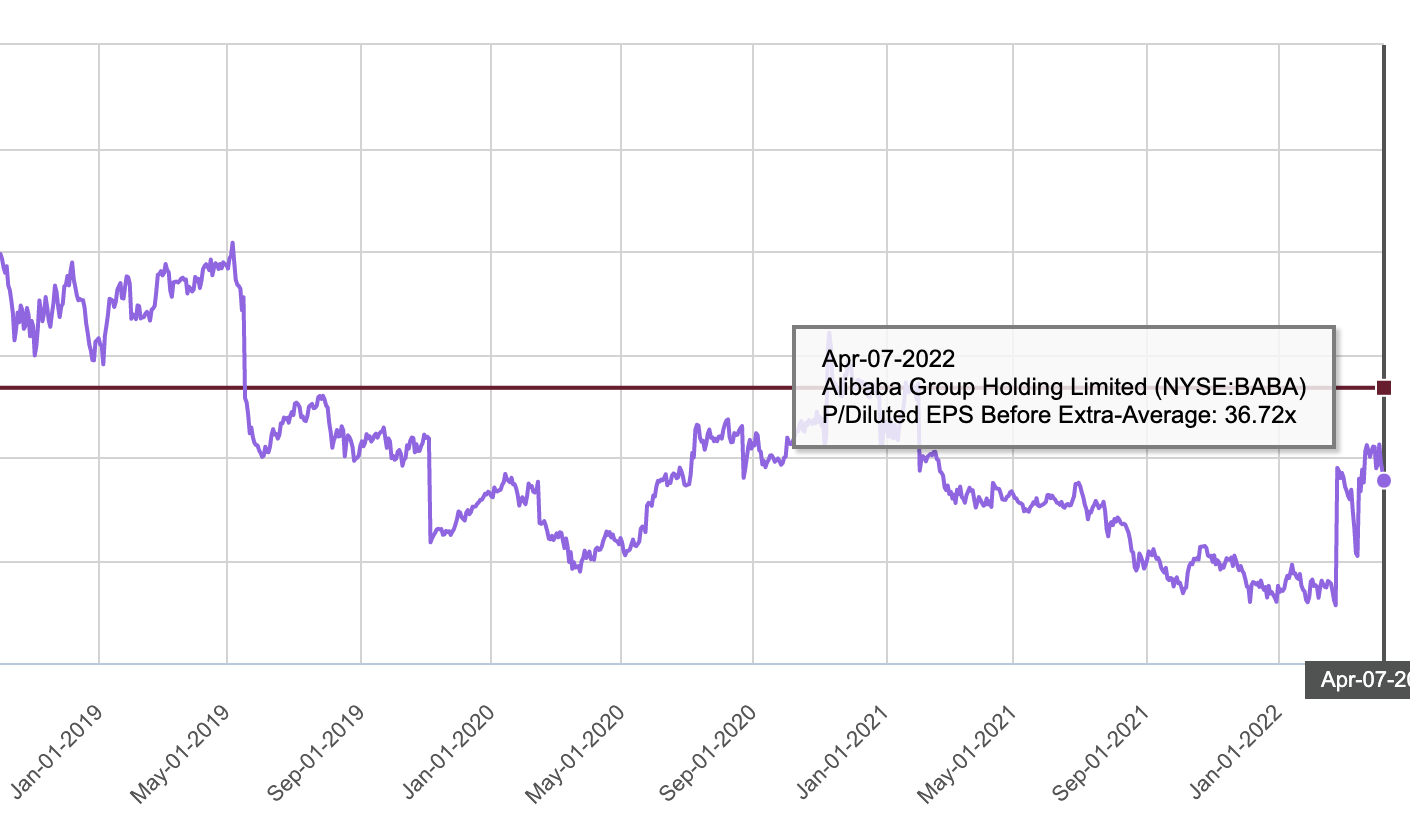

Price/Earning (P/E) ratio (5 Year)

The current P/E Alibaba stands at 27.7x while it’s 5-year Avg P/E ratio stands at 36.72x

Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs. On the other hand, operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends to investors.

Looking at Alibaba’s financials, its gross margin has dropped to about 40+%. Its operating margin has decreased to about ~10% while its FCF margin has decreased to around 13%. An operating margin of more than 15% is regarded as good in most businesses as a rule of thumb. As a result, this clearly demonstrates that Alibaba is still doing already financially.

| Other Key Ratios | 2017 | 2018 | 2019 | 2020 | 2021 | LTM |

| Gross Margin % | 63.0% | 57.5% | 45.8% | 45.1% | 41.5% | 37.3% |

| Operating Margin % | 30.9% | 28.2% | 16.3% | 18.7% | 15.3% | 10.8% |

| FCF% | 38.9% | 36.7% | 26.1% | 23.0% | 26.4% | 13.6% |

Our Stand

Given Alibaba’s strong market position in the Ecommerce space, it is a stock that investors should consider. Currently, Alibaba’s P/E ratio is 27.7 at a stock price of HK$105 (as of 7 April 2022), which is relatively undervalued for an industry leader with space to grow. Furthermore, IDC estimated that China’s public cloud market is predicted to be worth US$69.95 billion per year by 2024. With strong growth in Cloud business, Alibaba is poised to continue growing and be a key player in the Ecommerce and Cloud industry for the foreseeable future. However, the decrease in its margin is definitely a concern for investors. A reason for the decline in margin was due to the record US$2.8B fine that it had paid due to breach of Chinese regulations. However, it is crucial whether Alibaba can improve its margin in the future.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.