Is Adobe a dying business?

No, it’s Adobe Flash. Adobe Flash was critical in enabling websites to host movies and online games; but, with the advent of HTML5, a lot has changed.

In 2012, Adobe made a significant move, transitioning from a provider of one-time purchases to a subscription business model. Adobe’s progress was measured and thorough, effectively changing its primary business model. Meanwhile, it has now emerged as a “leader in the subscription economy.”

Adobe forecasts low guidance for Q2 FY2022, after the recent Q1 FY2022 Earnings Call. Adobe announced a suspension to all new sales of Adobe goods and services in Russia and Belarus on March 4, 2022. This might result in a $87 million reduction in overall ARR and a $75 million revenue impact for FY 2022. This resulted in a 10% drop in the share price. So today, we will be discussing whether we should buy Adobe.

Overview of Adobe Business

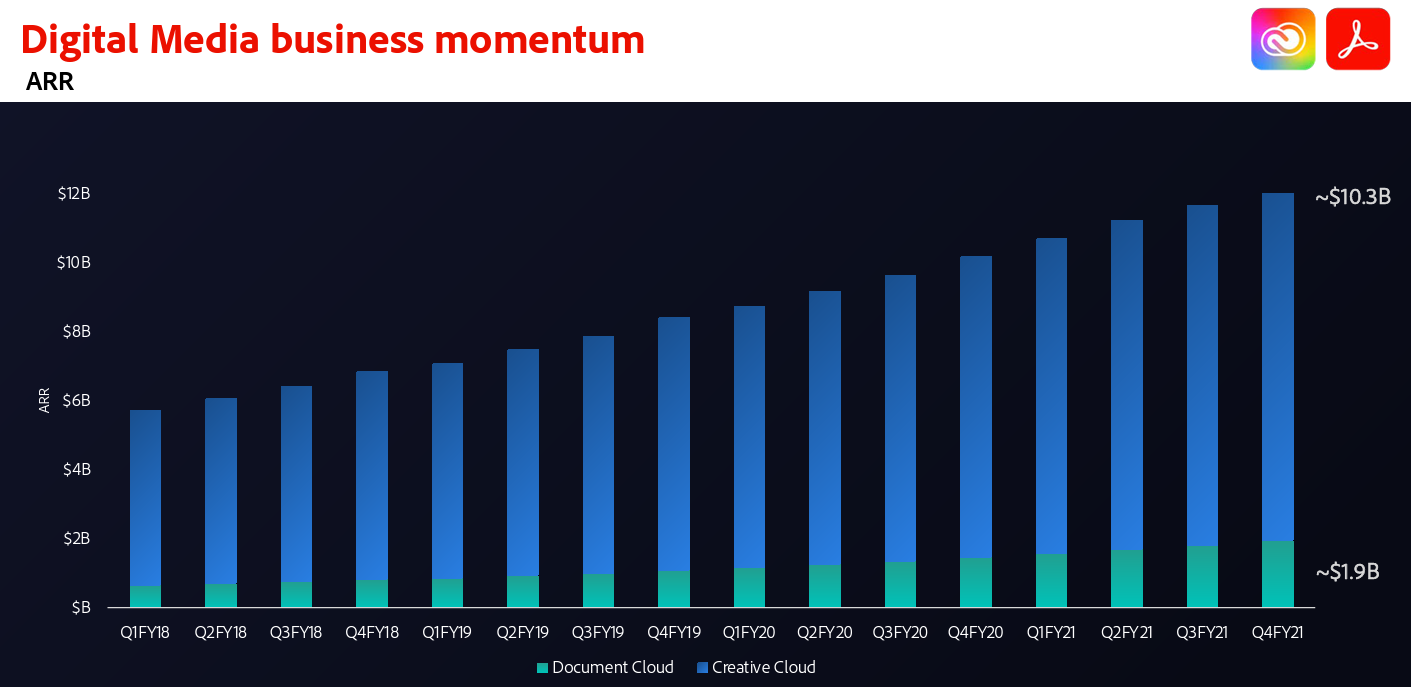

Adobe was founded in 1982 by John Warnock and Charles Geschke. They left Xerox PARC to develop and commercialize the Postscript page description language. Adobe is now a worldwide computer software firm that specializes in multimedia applications. Adobe provides a variety of solutions, the most notable of which being Adobe Photoshop, Adobe Illustrator, and Adobe Acrobat Reader. In Q1 FY2022, the Digital Media segment revenue grew to $12.57 billion.

Key Products and Services

Adobe has 3 key products and services:

- Creative Cloud,

- Document Cloud and

- Experience Cloud.

Adobe had a strong Q1 FY2022. They achieved a record $4.26 billion in revenue, 17% year-over-year growth on an adjusted basis. Digital Media Business, both Creative and Document Cloud, achieve $3.11 billion in revenue. The Experience Cloud Business has also shown strong growth, achieving $1.06 billion in revenue.

| Digital Media | Description |

|---|---|

| Adobe Creative Cloud | Creative Cloud is a collection of 20+ apps for photography, video, design, web, UX and social media — Adobe DC, Photoshop, Premiere Pro, Illustrator, InDesign and so on. |

| Adobe Document Cloud | The world’s leading PDF and electronic signature solutions – Adobe Acrobat, Acrobat Sign, Acrobat PDF Pack, Acrobat Export PDF and its suite of mobile apps. |

| Products | Description |

|---|---|

| Adobe Experience Cloud | Adobe Experience is a collection of business applications specifically for insights, content, engagement and more – Manager Sites, Manager Assets, Commerce, Analytics, Workflow and so on. |

Qualitative Factors for Adobe

Let’s now take a look at some of the qualitative factors that affects Adobe’s business:

Economic Moat

- High Switching Costs – Learning Curve and Industry Standards Trap

- The ‘Learning Curve Trap’ revolves around providing a fantastic value proposition that is only available to those who are prepared to learn how to use it. To keep clients hooked on their goods, Adobe employs the ‘learning curve trap,’ in which some users become certified experts in their program. As a result, switching to a different solution becomes difficult since professionals in your company will lose a skill that they have developed in order to use this program and will have to start again.

Industry Standards

- The ‘Industry Standards Trap’ compelled professionals and businesses to purchase industry-standard software. It presents itself as a market leader based on public acceptability. Adobe’s Digital Media software, as well as Adobe’s. pdf format has become the industry standard, making it difficult to utilize anything else. Hence, Adobe’s Digital Media software and its widely known file format around the world, made the switching expenses substantial.

- Network effects

The “network effect” is a common economic moat for platform enterprises. Adobe made a brilliant step by utilizing their Acrobat reader. It distributes the Acrobat reader for free in order to establish a market for the software that creates Acrobat files. This strategy combines a product line with a subscription platform for digital experiences have shown tremendous success to Adobe.

Quote:

“Normally, if you want to sell a car for more money, you need more features, for example traction control or fancy LED headlights,” explains Oliver Goldman, Technical Advisor to the CTO at Adobe.

Growth Opportunities

- Adobe Experience Cloud

Adobe’s Experience Cloud business continued to expand in the fourth quarter, bringing in $1.06 billion in revenue and $932 million in subscription revenue. Adobe Experience Cloud is a set of connected, AI-driven products and services designed to help businesses offer exceptional customer experiences across all elements of the customer journey. There are a few growth opportunities to note:

- Exciting Product Innovations: Real-Time Customer Data Capabilities (Adobe Real-Time CDP and Adobe Target)

- Strong performance in Adobe Experience Manager, emphasizing the need for unified content management to meet the ever-increasing demand for content at speed and scale

- An expanding partner ecosystem, including a partnership with OneTrust to simplify consent management, the next phase of e-commerce integrations with FedEx, Walmart and Payal as well as The Weather Company

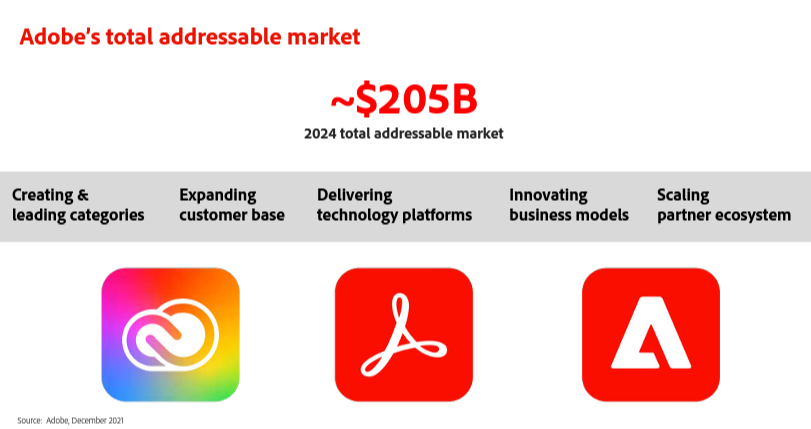

- Total Addressable Market

There is a big and exciting opportunity for Adobe ahead.

The rise of narrative is driving Adobe’s Creative Cloud. Content is always developing because everyone – people and corporate communicators alike – has a narrative to tell, and new technology allows them to do it.

Adobe’s Document Cloud is growing in popularity, assisting people who still use paper in their shift to the digital economy. It’s difficult to say how much of the potential market has switched to digital, but we know there are still many…

Adobe’s Experience Cloud intends to help its enterprise customers sell at a higher price point.

How so?

Companies are increasingly attempting to emulate the high-quality customer experience given by Amazon and other such companies. Adobe is one of them.

Creative Cloud, Document Cloud and Experience Cloud (TAM):

- 2024: ~$205 Billion

- 2021: ~$15.15 Billion

Business Risks for Adobe Stock

- War between Russia and Ukraine

Unsurprisingly, Russia and Ukraine have affected Adobe. Earlier this month, Adobe announced a cessation of all new sales in Russia and Belarus. Thus, Adobe has made the decision to reduce their Digital Media ARR balance by $87 million:

- $75 million (Russia and Belarus)

- $12 million (Ukraine)

Personally, we feel that this will be a short-term risk as such war will not exist for a long time. Indeed, it does create uncertainty to the market as the market is always forward looking. However, this $87 million in ARR is dismissalable as it is a very little portion of Adobe’s ARR – ~$13.5 Billion.

- Intense Competition – Strategic Alliances

Many of Adobe’s competitors are Multinational Companies (MNCs) such as Salesforce, Oracle, SAP, SAS and Google.

In addition, many of these firms develop new worldwide strategic alliances. Salesforce and Google are two such instances. Google will be able to use their existing advertising networks, which are massive in and of themselves, while Salesforce will use its analytics platform. These strategic alliances will benefit both Salesforce and Google, but they will put greater pressure on Adobe.

Quantitative Factors for Adobe

Financial Highlights

- Revenue by Segment/Product

The Subscription segment, which includes Digital Media (Creative Cloud and Document Cloud), Document Experience and Publishing and Advertising, accounts for the majority of Adobe’s revenue in 2021 – 92.3%, while the Product segment (License for on-premise software) accounts for 3.5% and the Services and other segment (Consulting, Training, Maintenance and support) accounts for 4.2%.

- Revenue by Geography

Overall revenue grew in all geographic regions in FY21 compared to FY20, owing principally to higher Digital Media revenue and, to a lesser extent, higher Digital Experience revenue. The reasons listed in the segment information above were responsible for the variations in revenue by reportable segment within each geographic location. Furthermore, the U.S. dollar primarily weakened against EMEA currencies and the Australian Dollar.

Key Valuation Ratios

- Revenue Growth

Adobe’s 2021 revenue stands at $15.79B with 23% (YoY growth) and 5-Year CAGR stands at 16.7%.

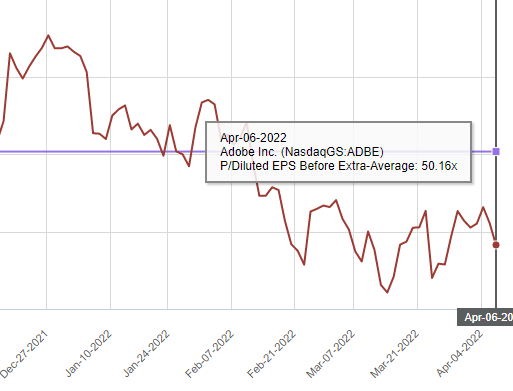

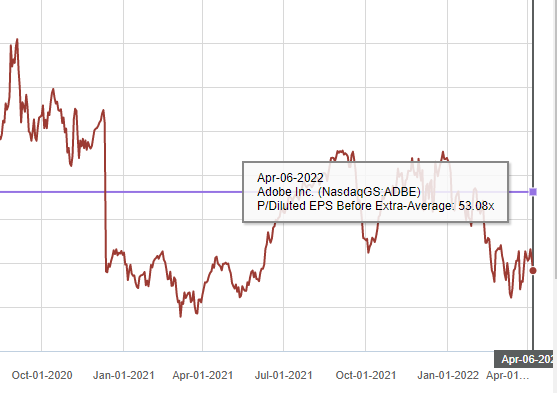

- Price to Earnings (P/E ratio) – 1 year and 5 year

P/E – 1 year

The current Adobe P/E stands at 44.13x while its 1-year Avg P/S ratio stands at 50.16x.

P/E – 5 year

The current Adobe P/E stands at 44.13x while it’s 5-year Avg P/S ratio stands at 53.08x.

- Other Key Ratios

A company’s profitability is measured using two metrics: gross profit margin and operating profit margin. The difference is that gross profit margin only considers direct manufacturing costs, but operating profit margin also considers running expenses such as overhead. While Free Cash Flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.

Adobe’s financials look phenomenal, its gross margin has been lingering around 85+%, its operating margin has been around 40+%, and its free cash flow margin has been hovering around 40%. An operating margin of more than 15% is regarded as good in most businesses as a rule of thumb. As a result, this clearly demonstrates that Adobe has been doing well financially. Furthermore, Adobe’s margins are steadily increasing, indicating that the company is expanding its margins, which is a positive indicator for the company.

| Other Key Ratios | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|

| Gross Margin % | 86.0% | 86.2% | 86.8% | 85.0% | 86.6% | 88.2% |

| Operating Margin % | 39.7% | 43.3% | 41.7% | 45.7% | 45.9% | 51.1% |

| FCF% | 34.1% | 37.5% | 41.7% | 36.0% | 41.2% | 43.6% |

Our Stand

Given Adobe’s strong market position and large economic moat, I doubt that the war in Ukraine and Russia will have a significant impact on Adobe’s revenue in the immediate run. Adobe’s plan to target the USD$205 billion Total Addressable Market (TAM) demonstrates that there is still plenty of space for growth. Moreover, because of the stickiness of its cloud-based subscriptions, its industry-standard media tools have been widely adopted.

Adobe’s new suite of tools, in my opinion, is a reflection of the company’s continued innovation, and the Creative Cloud’s recent price hikes show that it still has a lot of pricing power in the digital media software industry. As a result, investors should overlook the near-term challenges, purchase the stock, and concentrate on the firm’s long-term growth potential.

If you are keen, check out our articles on other analysis: Trust Bank Referral.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.