Finally, the end of the year is in sight once more. Yes, the holiday season is upon us, but it also marks the beginning of the FY22 tax filing season. Income tax may be a completely strange concept to many people who have recently joined the workforce.

Now would be an ideal time to begin calculating the projected income tax that you are likely to pay next year. To begin all this, you will have to first estimate your annual income from January 1 through December 31, 2022.

Let’s first calculate your taxable income for 2022 before discussing some income tax tips to lower your income tax in 2022.

Calculating your 2022 Taxable Income

For Singaporeans , you might have multiple sources of income. However, not all incomes are taxable. In Singapore, incomes that are taxable include Employment Income, Dividends, Interest, Rent, Royalty and more.

Refer to the IRAS website on what is and isn’t taxable in Singapore if you have any other sources of income about which you are uncertain.

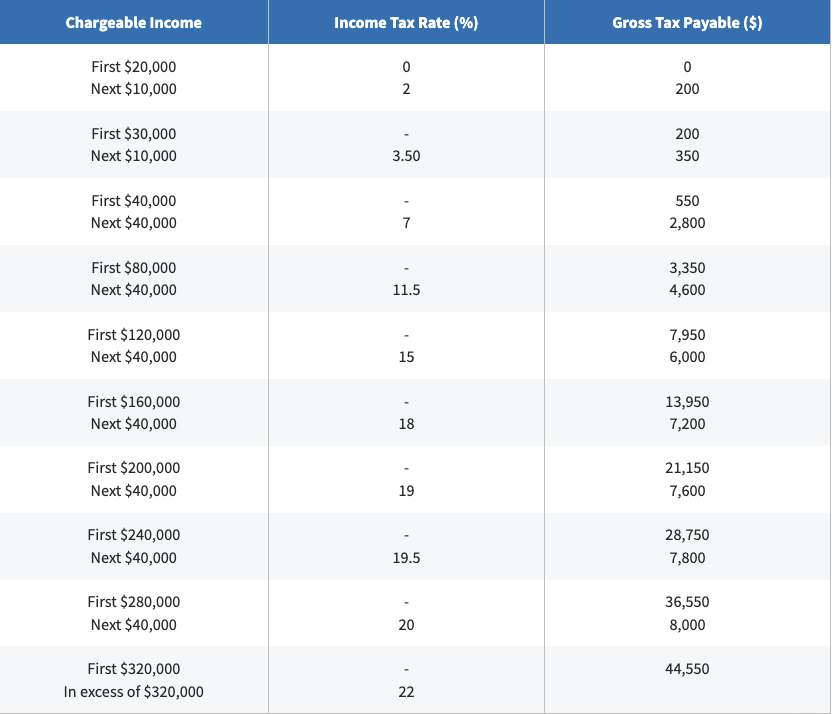

Next, add up all of your 2022 taxable income. By looking at Figure 1 below, you can get an idea of how much income tax will cost in YA2023.

However, this is not the final income tax as one may be eligible for several tax reliefs. This will be subtracted from your total taxable income. Your chargeable income, which is the resultant (lower) number, is used by IRAS to determine how much tax you must pay in the upcoming year.

As you can see, once your chargeable income exceeds $40,000, your income tax increases fairly significantly. In order to reduce your chargeable income, you might want to learn what tax reliefs are eligible for you.

Keep in mind that the $80,000 ceiling on income tax relief is the highest amount that can be received. Hence, do take note of this as we share with you some tips to reduce your income tax.

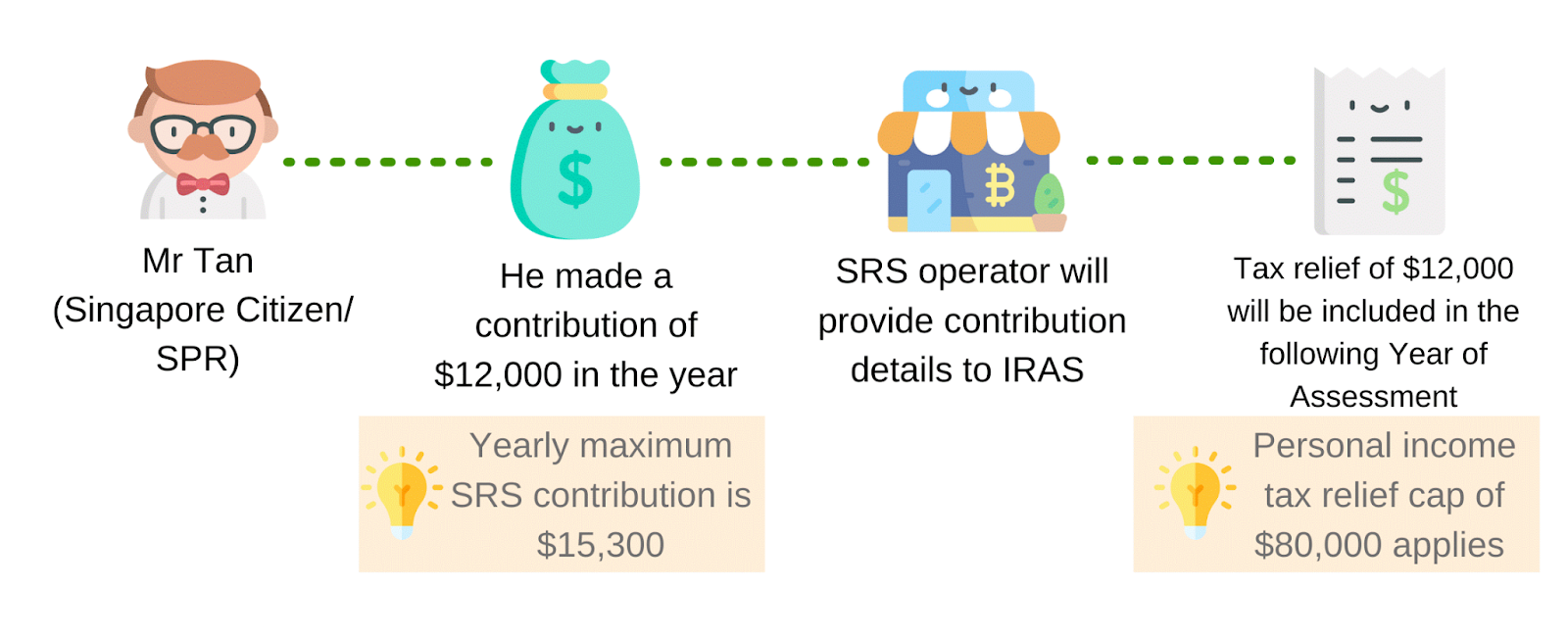

Income Tax Tip #1: CPF top-ups and the Supplementary Retirement Scheme

Topping up to all of your retirement accounts is the simplest and most well-known technique to lower your taxes. You receive a $1 deduction from your chargeable income for every $1 you deposit in these accounts. Any top-ups have to be completed by December 31 and there are limits to the different accounts.

For SRS, you can voluntarily open a retirement savings bank account at DBS/POSB, OCBC, or UOB. After topping up your CPF and SRS, do ensure that the contributions are accurately reflected in your tax statements.

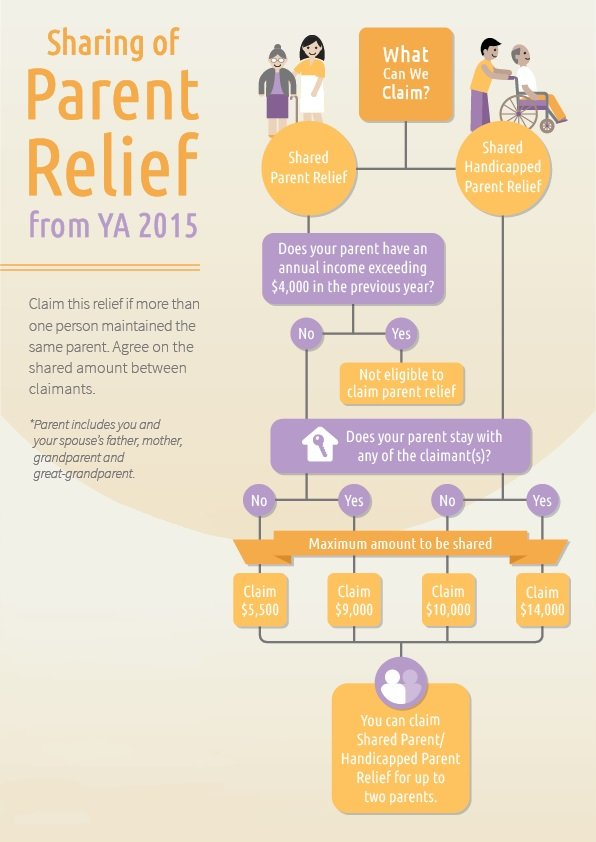

Income Tax Tip #2: Staying with parents / grandparents

The problem of an aging population is one that has been plaguing developed countries for some time now. Singapore is no stranger to this issue too. The most obvious way to try and solve this problem is to invoke filial piety and get the elderly’s own children to care for them. There are tax breaks that can be applied for in order to lessen the children’s financial burden.

The Parent Relief scheme is a great way to reduce your taxable income. Although it’s technically called “Parent Relief”, this also applies to in-laws, grandparents, and grandparents-in-law. However they must not be earning more than $4000 per year and one can only claim up to 2 dependants. Furthermore, the parent relief cannot be double-claimed on the same person.

Nonetheless, it’s a great way to reduce your taxable income if you have eligible dependents!

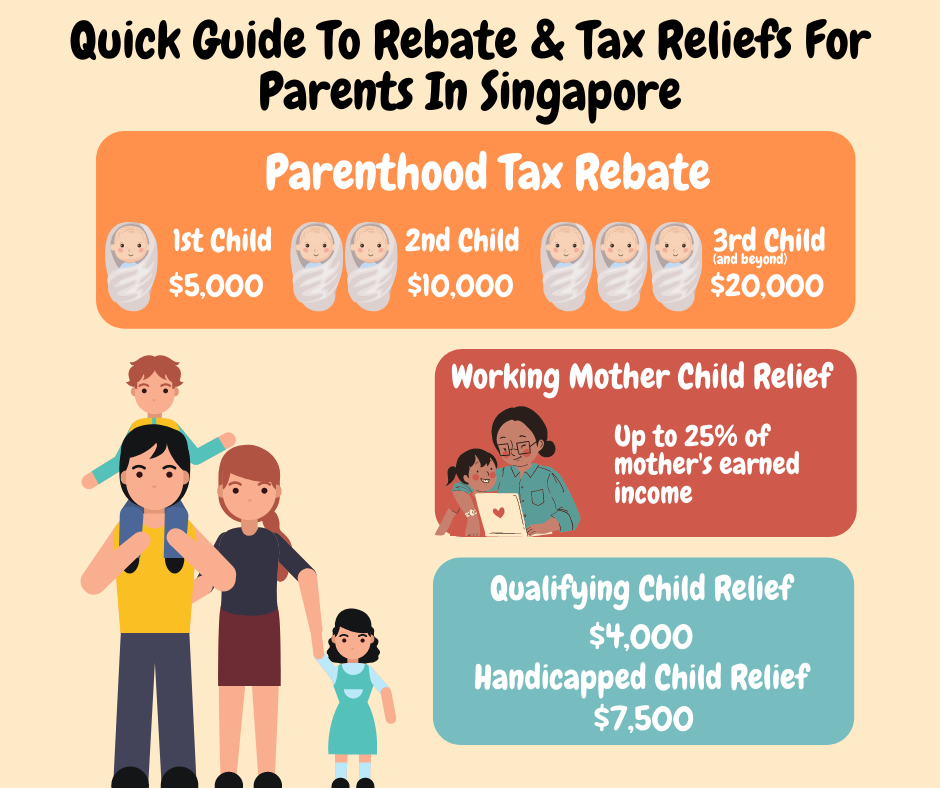

Income Tax Tip #3: For Parents and Working Mums

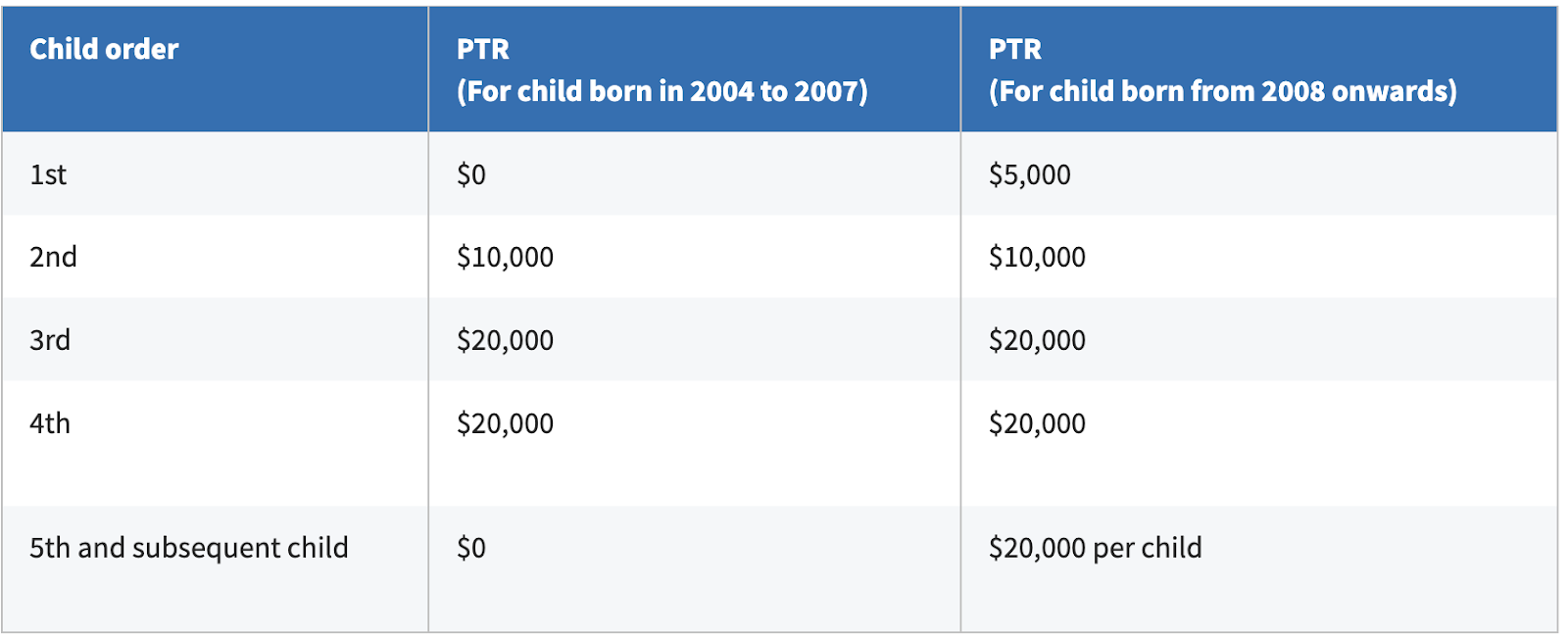

Apart from the aging population issue, the birth rate for most developed countries is also decreasing drastically. In addition to the baby bonus, the government also provides many income tax reliefs for working parents. Below are some Child Reliefs that parents can apply for:

Do note that working mum can qualify for both Qualifying Child and Working Mother’s Child reliefs. It is capped at $50,000 per child.

For parenthood tax rebates, it is a fixed one-off tax relief. This is slightly different from the other child reliefs. Any unused funds will be automatically carried forward to lower your upcoming income tax obligations. Any balance that is left over is not refundable.

Clearly, it’s a great way to reduce your taxable income if you have eligible children!

Tip #4: Donations

When you make a donation to an IPC (Institution of a Public Character), you’re entitled to a 250% tax deduction. That means for every dollar you donate, you can deduct $2.50 from your income taxes.

This is a significant savings, and it’s one of the reasons why many people choose to support charities through donations. When you donate to an IPC, you’re not only helping a worthy cause, but you’re also saving money on your taxes. It’s a win-win!

Do note that working mum can qualify for both Qualifying Child and Working Mother’s Child reliefs. It is capped at $50,000 per child.

Lastly, the 250% tax deduction for qualifying donations will be extended for an additional two years until 31 December 2023. This is to support the charitable sector and encourage Singaporeans to continue supporting their community.

Tip #5: Upgrading Skills

If you’re planning to upskill in 2022, good for you! You would qualify for tax reliefs of up to $5,500. That’s a significant amount of money that can go towards covering the cost of your course fees.The government is encouraging people to upskill and improve their employability, so this is a great opportunity to take advantage of.

Hence, if you’re looking to learn something new, consider taking a course next year and claim the tax reliefs available.

For more information on course fees relief, you can refer to here for more information.

Other Additional Tips to reduce income tax

Apart from the above stated relief methods, there are some tax reliefs that are automatically applied. This includes Earned Income Relief, CPF contribution and NSman relief. Click here to find out more. Be sure to check that these reliefs are applied before you pay for your income tax.

There’s no one-size-fits-all answer to the question of how much you should pay in taxes each month. However, following these tips can help you reduce your income tax bill. The key is to find a balance. What you’re comfortable with paying tax and maintaining your financial stability. In addition, be sure to stay up-to-date on the latest regulations for tax reliefs to take advantage of the benefits. Lastly, if this is your first time, you can talk to a colleague or someone more senior for advice on tax relief too.

If you are keen, check out our other latest articles. Trust Bank Referral, Best Standard Chartered Cashback deals and 5 Singapore REITs you can buy and hold forever.