As we enter the new year, there’s one big question on everyone’s mind. Should we invest in US tech or Chinese tech for 2023?

Starting with US tech, there’s no doubt that this industry has been doing well over the past decade. By the end of 2021, the US tech industry was worth an estimated $1.6 trillion. The current US Tech market estimates to account for 35% of the total world market. American tech companies are responsible for some of the most innovative and cutting-edge products and services in the world. Some notable names include: Alphabet, Apple, Microsoft, Amazon and more.

Introduction

However, in the past few months, the US tech stock prices have also taken a beating. In 2022, the tech-focused NASDAQ has declined by over 30%. The following is mainly attributed to economic uncertainty, rising interest rates and disappointing earning results. As a result, the narrative for investing has also gradually shifted from forecasting future growth to profitability. Hence, many US tech stocks are now less appealing to investors as most of them are not yet profitable. However, for profitable US Tech companies, could this be an opportune time to invest in them?

Turning to Chinese tech, this is an industry that has seen many headwinds in the recent two years. The most noteworthy event would be China’s tech crackdown by the Chinese regulators on data usage and monopolism acts. As a result, many Chinese tech firms’ earnings were also affected over the past 2 years. This has triggered a selloff for many of these Chinese Tech firms. It was estimated that more than $1 trillion was wiped off from the market value of some of these prominent companies.

However, the easing of China’s covid policies has gotten many investors excited. Many are expecting the Chinese economy and consumption to recover which will eventually benefit the Chinese firms. It seems to be a matter of time before the Chinese economy recovers. Could now be a good time to start investing in them?

Both the US and Chinese Tech companies seem to have their fair share of pros and cons. Let’s take a closer look into the qualitative and quantitative factors to determine.

Qualitative Factors affecting US and Chinese Tech

When it comes to making investment decisions, there are many factors to consider. But when it comes to deciding whether to invest in US tech or China tech, there are two main factors that come into play: qualitative and quantitative. For Qualitative factors, we will be looking into factors like Interest Rates, State of Economy and Regulatory Pressure.

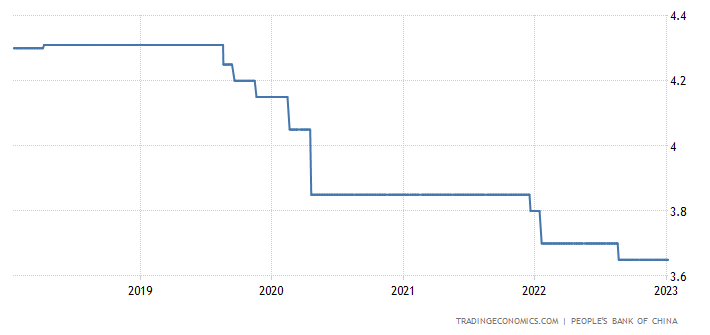

Qualitative Factor #1: Interest Rates

In general, tech stocks tend to be negatively impacted by rising interest rates. This is because high interest rates make the cost of borrowing more expensive. As many investors would say, the era of easy money comes to an end. This reduces the tech businesses’ cash flow and makes it harder for them to reinvest into innovation and growth prospects. Additionally, for unprofitable tech companies, higher interest rates means a reduction of expected cash flow which represents lower valuation.

The current interest rate environment in the US and China is 4.5% and 3.65%, respectively. It appears that the rising loan rates are currently having a greater impact on US tech companies. In addition, it is anticipated that the US terminal interest rate would rise to 5.1% in 2023. This would indicate that the financing environment for US tech enterprises in 2023 is anticipated to be more challenging.

Winner: Chinese Tech Firms

Qualitative Factor #2: State of Economy

With regards to COVID-19, the US and Chinese governments have taken quite different positions. US has been managing the COVID-19 policies at the state level. Many US states began to lift most or all of their restrictions in the spring and summer of 2021.

As for China, they have only recently announced easing measures for Covid in December 2022. Self-isolation will now be permitted if they are contracted with Covid. Additionally, they won’t need to perform any virus tests before their trip.

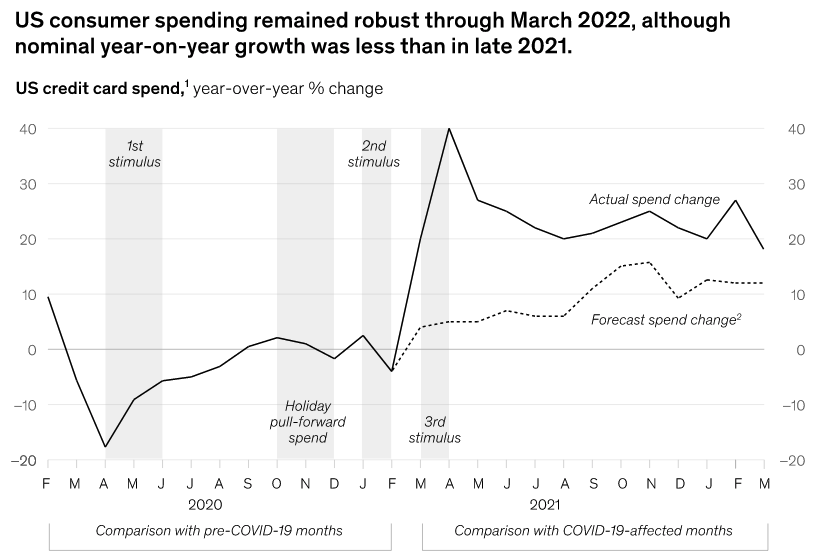

China’s current economic recovery is slower because China eases their COVID-19 policies a year later than US authorities. This is also evident in the consumer spending for both the US and China. A study by Mckinsey has shown that the US consumers spend 18% more in March 2022 than March 2020. This is 12% more than forecast based on pre-COVID trajectory.

According to CNBC, China’s current consumer spending is at about 50% of normal levels. However, many are only expecting business to return back to normalcy after 3 to 4 months. The Chinese Tech sector is anticipated to be more negatively impacted given the current state of both economies.

Winner: US Tech Firms

Qualitative Factor #3: Tech Regulations

Regulations related to technology have affected technology firms in both China and the United States in different ways.

In China, technology firms have generally had to comply with strict regulations and censorship rules. Some of the notable regulations include the “common prosperity” campaign and “anti-monopoly” rules. This is because as some of the Chinese Tech grew larger over the past decade, they have squeezed out small business instead of promoting healthy competition. This was a concern for the Chinese government and thus the authorities tightened enforcement of its antitrust laws in 2021. This was to align the Chinese companies back to the whole “common prosperity” campaign that was emphasized by the Chinese regulators. As a result, tech firms like Alibaba, Tencent, Didi, Bytedance and JD.com were all handed hefty fines for abusing their market power.

In addition to that, many of these tech firms were holding on to a lot of customer’s personal data. This became a concern as the government was afraid this could fall into the hands of foreign authorities or entities. Hence, many Chinese Tech firms had to do significant business reform to align with the authorities’ regulations.

In the United States, technology firms have generally had more freedom to operate. However, they also do have their fair share of scrutiny. The US government has been focused on issues related to data privacy, national security, and competition in the technology sector. Some key examples include the Cambridge Analytica data scandal.

Overall, both Chinese and US technology firms have been affected by regulations in their respective countries. However, the nature of these regulations and their impact on the firms is different. Chinese firms face more restrictive regulations and censorship, while US firms are facing increased scrutiny and potential penalties for noncompliance.

Winner: US Tech Firms

Quantitative Factors affecting US and Chinese Tech

Before we deep dive into the quantitative factors, do note that we are only taking the top few companies as a reference. Hence, it may not paint a complete picture of the entire tech industry for the respective countries.

For US Tech firms, we have selected the following: Apple, Alphabet, Amazon, Microsoft and Meta. While for Chinese Tech firms, they are as follows: Alibaba, Tencent, Meituan, JD.com and Xiaomi.

Quantitative Factor #1: Revenue Growth

The US Tech companies’ average revenue growth rates are 8.46% (1Y), 18.33% (3Y) and 18.86% (5Y) respectively.

On the other hand, Chinese Tech companies’ average revenue growth rates are 3.70% (1Y), 19.41% (3Y) and 27.04% (5Y) respectively.

The Chinese tech sector displays slightly higher revenue than its US counterparts, despite regulatory pressure and delayed Covid easing measures.

Winner: Chinese Tech Firms

Quantitative Factor #2: Operating Profit Margin Growth

Next, we compare the operating profit margin across the tech firms. As these companies grow, “Operating Margin” will give us a glimpse of how well managed the company is. This is because it illustrates how efficient the company is at generating profits from its revenue.

The US Tech companies’ average operating margin growth are -17.82% (1Y), -0.82% (3Y) and 1.00% (5Y) respectively. The operating margins of US tech companies appear to have maintained over the last three to five years.

On the other hand, Chinese Tech firms’ margins have fluctuated quite drastically over the past few years. This could be partly attributed to the hefty fines which affected their operating margin.

The management of the US Tech firms appears to have been more successful with managing the margins better. The ability to maintain consistently at about ~20% is not an easy feat.

Winner: US Tech Firms

Quantitative Factor #3: Price/Equity Ratio

Thirdly, we shall look into their Price-to-Equity ratio. This is a good indicator for profitable companies. It gives an indication of what investors are willing to pay for current and prospective growth of the company. If a company is trading at a high P/E ratio, this means that investors have high hopes for its future earnings.

The US Tech companies’ average P/E ratios are 35.15 (3Y) and 35.68 (5Y) respectively. The current average P/E for US Tech companies is at 32.52.

However, the Chinese Tech companies’ average P/E ratios are at 17.92 (3Y) and 34.59 (5Y) respectively. The current average P/E for Chinese Tech companies is at 3.5.

In conclusion, the current P/E valuation for 3 year and 5 year averages points to Chinese Tech being more undervalued. It is trading generally 80% lower than its 3 year average.

Winner: Chinese Tech Firms

Quantitative Factor #4: Price/Sales Ratio

Lastly, we shall look into their Price-to-Sales ratio. This is a good indicator for growth and non-profitable companies. It gives an indication of what investors are willing to pay for prospective growth of the company. If a company is trading at a high P/S ratio, this means that investors have high hopes for its future revenue sales.

The US Tech companies’ average P/S ratios are 6.94 (3Y) and 6.40 (5Y) respectively. The current average P/E for US Tech companies is at 4.80.

The China Tech companies’ average P/S ratios are 3.86 (3Y) and 4.19 (5Y) respectively. The current average P/E for China Tech companies is at 2.60.

In totality, current P/S valuation for 3 year and 5 year averages points to US and China Tech being evenly undervalued. It is trading generally 40% lower than its 3 year average.

Winner: Breakeven

Conclusion

In conclusion, which country tech firms should you focus in 2023 depends on your investing horizon. For a short-term reversal play, investing now into the Chinese Tech Firms could be a good opportunity. However, there will always be regulatory pressure which Chinese investors should be well aware of. Considering the current economic climate, investing in US tech may be a wise decision for those looking for long-term growth. Finally, before you invest into either, please do sufficient research into their individual products and services before making any decisions.

In addition, if you do like the finance matters we share, check out our other latest articles. Trust Bank Referral, HSBC Account and Credit Card Deals and The Battle of the Digital Banks.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalized investment advice. Readers should always do their own due diligence and consider their financial goals before the usage of these products. We do not offer any warranty or assurance regarding the quality of these services or goods.