If you are looking for the best saving accounts in Singapore, this article is for you. In 2022, due to the spiralling inflation, the US Fed has raised interest rates by over 4+%. Even though this is detrimental to the equities market, this has raised the interest rates for banks.

As a result, we have seen banks in Singapore raising their Fixed Deposits and Savings Accounts interest rates. When it comes to choosing a savings account, there are many factors to consider. The interest rate is important. However, you also need to consider the balance and the different products you may need to purchase to qualify. We’ve done the research and we’ve compiled a list of the best saving accounts in Singapore for 2022. So if you’re ready to start saving, read on to find the perfect account for you.

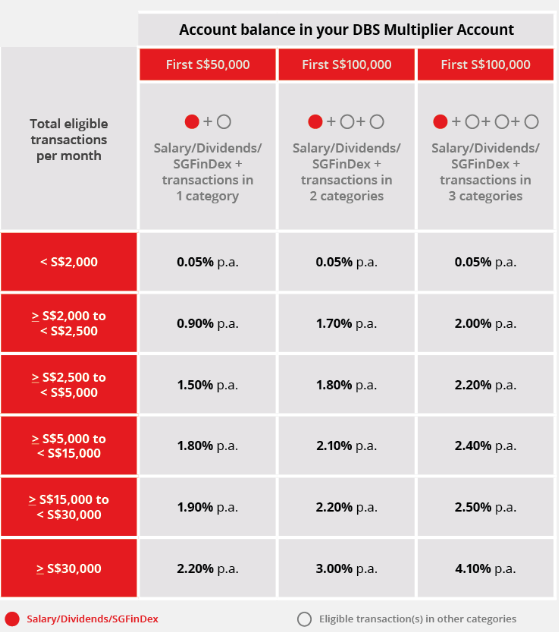

Best Saving Accounts #1: DBS Multiplier Account

One of the more well-known savings accounts is the DBS Multiplier Account. This is because most Singaporeans do have at least a DBS savings account. There have been multiple revisions to the interest rates and qualifying transactions announced. Below are the latest changes to the DBS Multiplier Account.

To be eligible, you must first receive a monthly income (such as salary credit or investment dividends or SGFinDex). Next, make a purchase from one or more of the following categories:

To achieve the highest interest rate, you must qualify in the following transaction categories:

- Credit Card (No min. spending)

- Selected Insurance policies (Life, CI, Endowment policies)

- Selected Investments (RSP, Unit Trusts, Equities, Bonds etc.)

- Home Loan

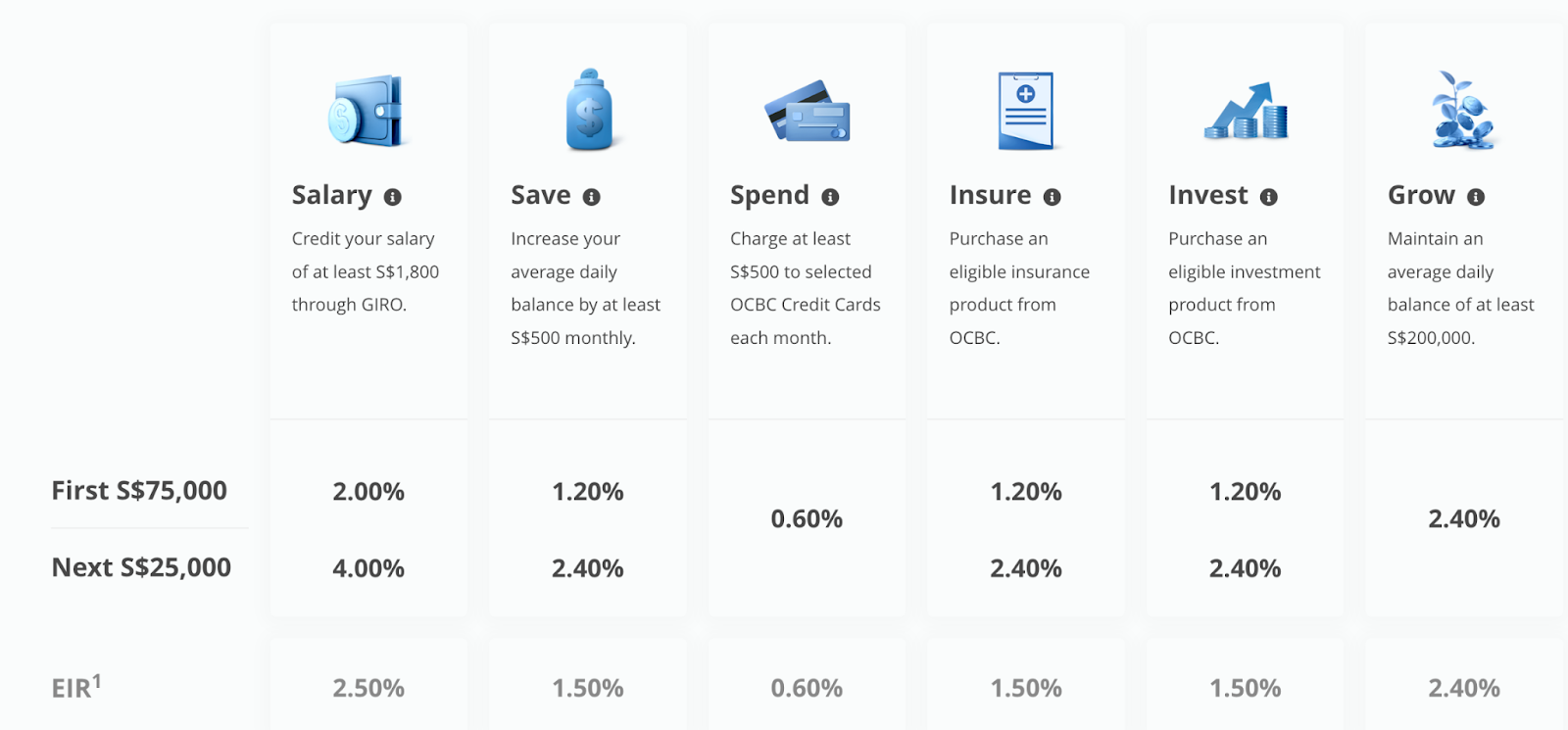

Best Saving Accounts #2: OCBC 360 Savings Account

There are many great savings accounts in Singapore, but the OCBC 360 account is one of the best. This account offers a high interest rate on your savings, which can help you reach your financial goals faster. Additionally, the account provides a number of perks and features that make it a great choice for savers.

Similar to DBS, the OCBC also has multiple categories of products to qualify for additional interest rates. You can earn up to 7.65% annually if you credited your salary, insured and made investments with OCBC.

To achieve the highest interest rate, you must qualify in the following transaction categories:

You will be eligible for at least 2.65% when you credit your salary and spend $500 on credit cards. Furthermore, if you save extra $500 per month, you get to earn additional 1.2% interest.

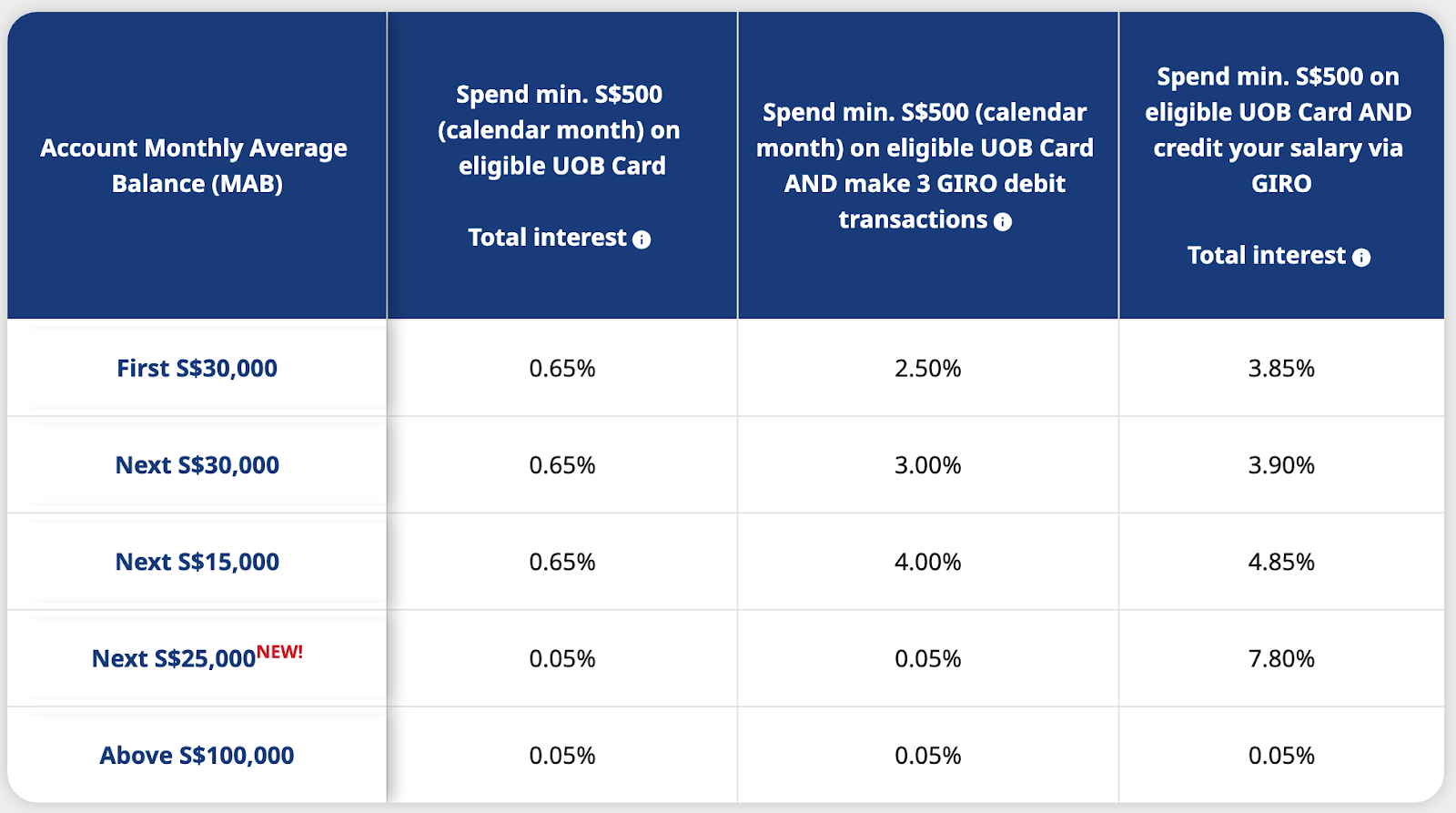

Best Saving Accounts #3: UOB One Savings Account

The UOB One Account is a great choice for those looking for a high interest savings account in Singapore. Recently, UOB has also changed their interest rate to one of the highest interest rates ever.

To achieve the highest interest rate, you must do the following:

- Spend a min S$500 on the eligible UOB cards

- Credit Cards: UOB One card, UOB Lady Card, UOB EVOL Card

- Debit Cards: UOB One Debit Card, UOB Lady’s Debit Card, UOB Mighty FX Debit Card

- Make 3 GIRO debit transactions

- Click here to find out more on the GIRO payments

Do note that the 7.8% is only for the next $25,000 after $75,000 balance. Hence, the effective would be ~5% if you have $100,000 in your savings account.

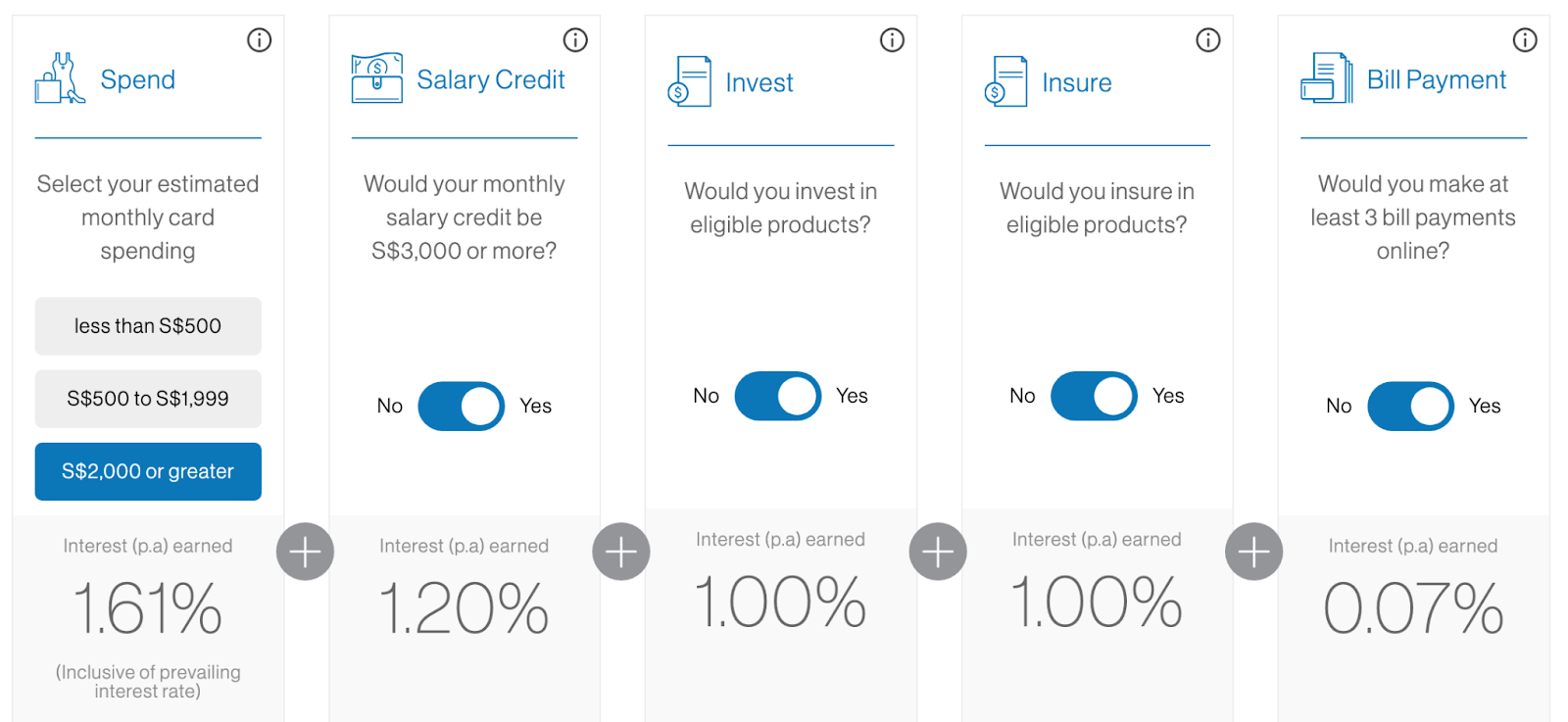

Best Saving Accounts #4: Standard Chartered Bonus$aver Account

Although the Standard Chartered Bonus Saver savings account isn’t the best for average people, it does fill a niche. It is targeting those who spend a min. of $2000 or more monthly with their credit cards. By crediting your salary at least $3000 and spending more than $2000, you will qualify for more than 2.8%.

To achieve the highest interest rate, you must qualify in the following transaction categories:

- Investment products

- Insurance products

- Bill payments

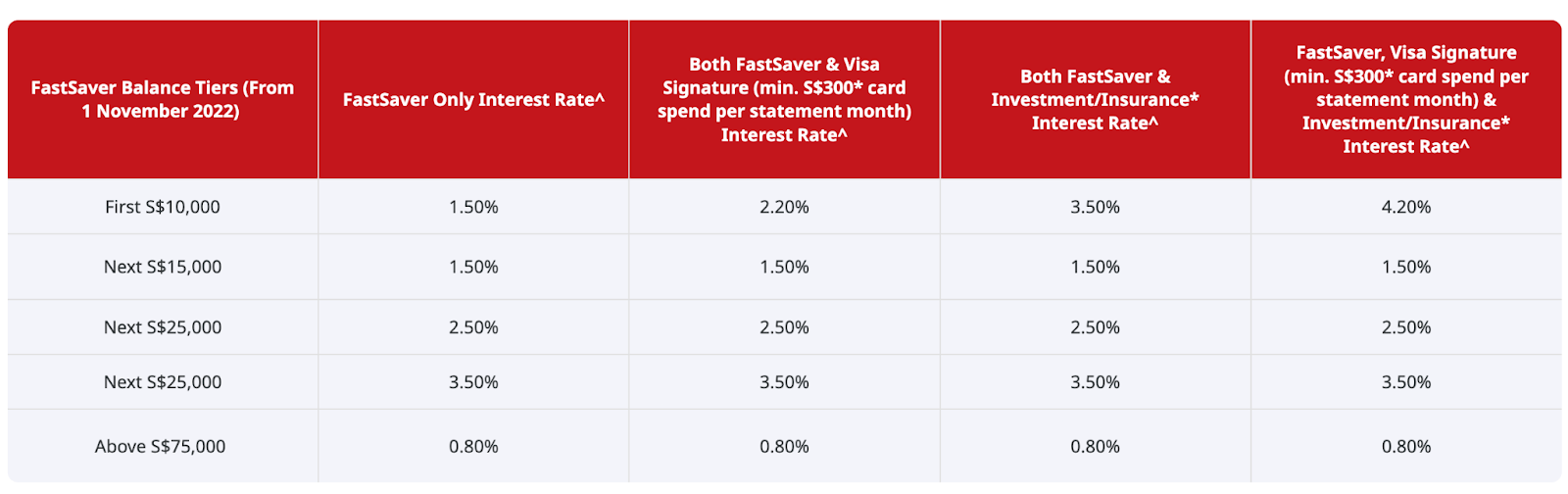

Best Saving Accounts #5: CIMB FastSaver Account

Once again, CIMB has also changed their interest rate to compete with the other banks. Currently, it is offering up to 4.20% per annum for their FastSaver users.

To achieve the highest interest rate, you must qualify in the following transaction categories:

- Spend min $300. on their Visa Signature Card

- Invest in either their Investment / Insurance products

Currently, there is no fall below fee and a very modest “minimum” balance of $1,000. This account will be ideal for the majority of young adults that started their careers or are still doing part-time jobs.

How to choose the best Savings Account for yourself?

There will be a couple of assumptions that we are making when comparing across the different bank accounts.

- This comparison will be assuming that they do not purchase any invest or insurance products.

- For students, they earn less than $2000 per month but spend approx. $300 per month.

- For working adults, we will assume that their salary is about $5000 per month. This is consistent with 2022 median working adult salary in Singapore.

However, there are definitely more considerations than what we shared above. Some people may prefer to purchase investment or insurance products with their banks too. By doing your research and understanding what each account offers, you can make a more informed decision. This will definitely help you to save more money in the long run. We hope our guide has helped you understand the different options available in 2022. Do note that these interest rates may change based on the market conditions. Nonetheless, we hope this article has given you information you need to make the best choice for your savings goals.

Keep an eye on this space next year as we share the latest interest rates for the different banks!

If you are keen, check out our other latest articles. Trust Bank Referral, UOB Credit Card Deals and Why should ALL 18 to 26 years old create this account.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.